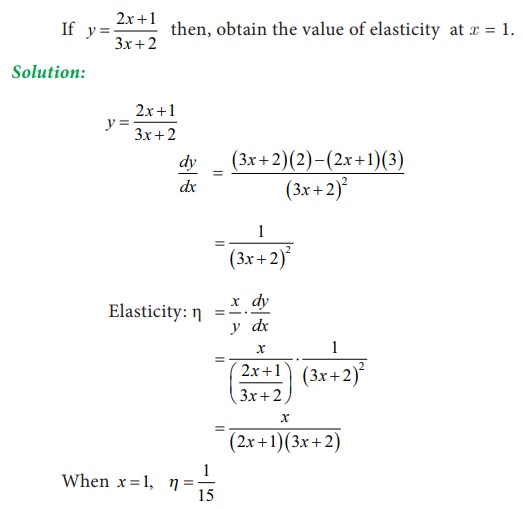

Applications of differentiation in business and economics - Elasticity | 11th Business Mathematics and Statistics(EMS) : Chapter 6 : Applications of Differentiation

Chapter: 11th Business Mathematics and Statistics(EMS) : Chapter 6 : Applications of Differentiation

Elasticity

Elasticity

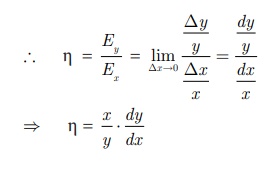

Elasticity ŌĆś╬ĘŌĆÖ of the function y = f (x ) at a

point x is defined as the limiting

case of ratio of the relative change in y

to the relative change in x.

(i) Price elasticity of demand

Price elasticity of demand is the

degree of responsiveness of quantity demanded to a change in price.

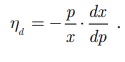

If x is demand and p is unit

price of the demand function x = f(p),

then the elasticity of demand with respect to the price is defined as hd =

(ii) Price elasticity of supply :

Price elasticity of supply is the

degree of responsiveness of quantity supplied to a change in price.

If x is supply and p is unit price of the supply function x = g(p), then the elasticity of supply with respect to the price is defined as hs

Some important results on price elasticity

(i) If |

╬Ę |>1, then the quantity demand or supply is said to be elastic.

(ii) If |

╬Ę |=1, then the quantity demand or supply is said to be unit elastic.

(iii) If | ╬Ę |<1, then the

quantity demand or supply is said to be inelastic.

Remarks:

(i) Elastic : A quantity demand

or supply is elastic when its quantity responds greatly to changes in its

price.

Example: Consumption of onion and

its price.

(ii) Inelastic : A quantity

demand or supply is inelastic when its quantity responds very little to changes

in its price.

Example: Consumption of rice and its price.

(iii) Unit elastic : A quantity

demand or supply is unit elastic when its quantity responds as the same ratio

as changes in its price.

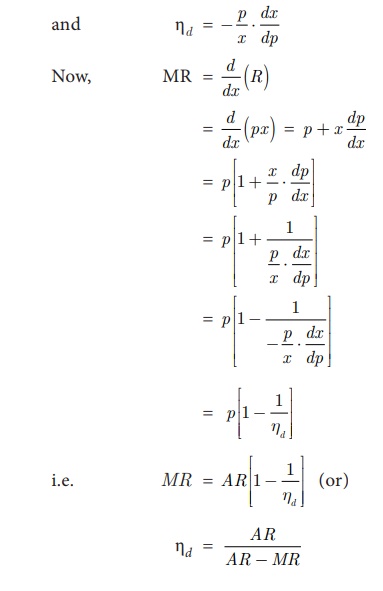

Relationship among Marginal revenue [MR], Average revenue [AR] and Elasticity of demand[╬Ęd].

We know that R(x)=px

Example 6.1

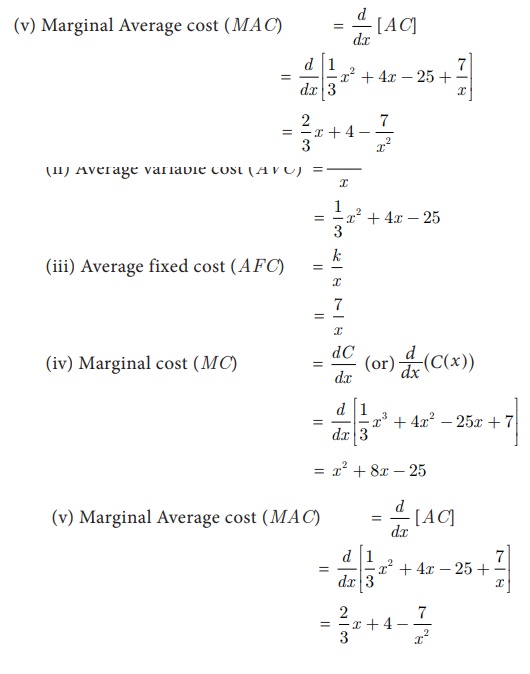

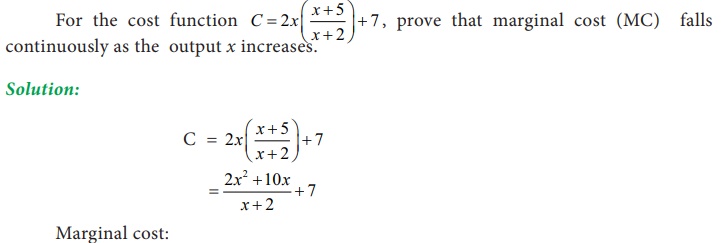

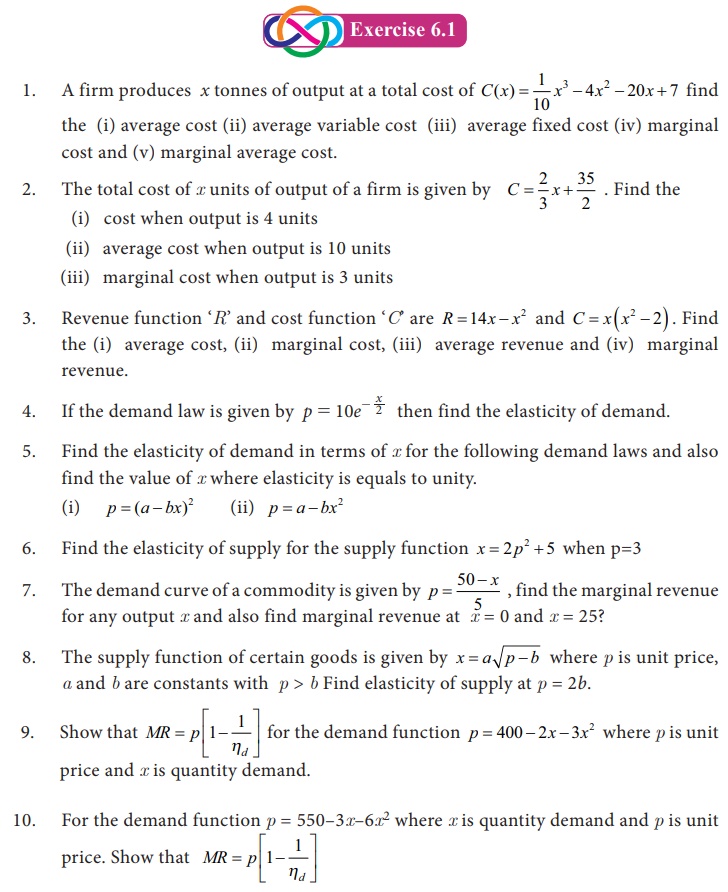

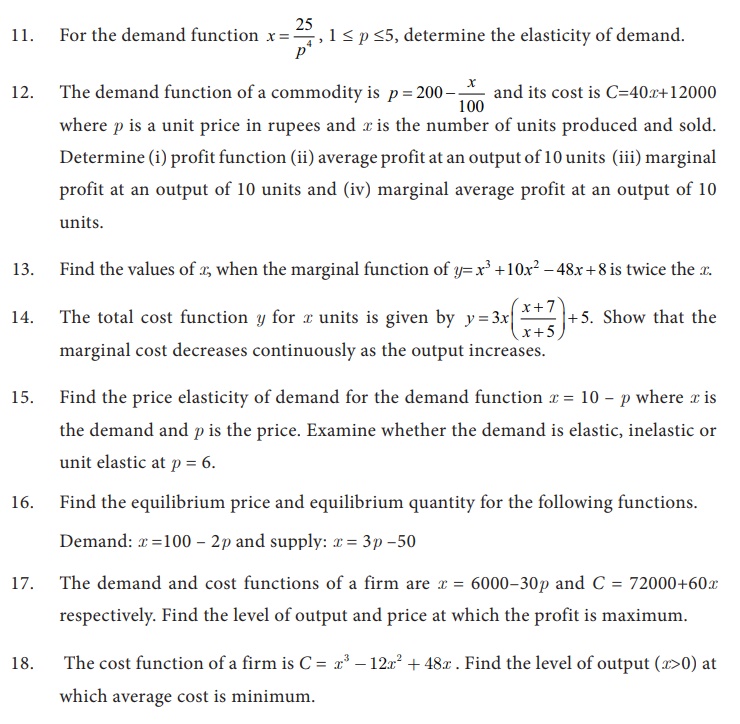

The total cost function for the

production of x units of an item is

given by

(i) Average cost

(ii) Average variable cost

(iii) Average fixed cost

(iv) Marginal cost and

(v) Marginal Average cost

Solution:

Example 6.2

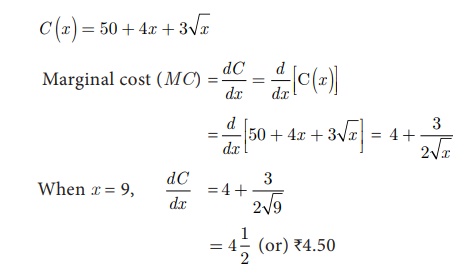

The total cost C in Rupees of making x units of product is C (x ) = 50 + 4x + 3ŌłÜx . Find

the marginal cost of the product at 9 units of output.

Solution:

MC is Ōé╣ 4.50 , when the level of output is 9 units.

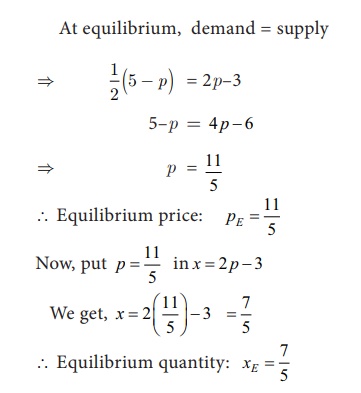

Example 6.3

Find the equilibrium price and

equilibrium quantity for the following demand and supply functions.

Demand : x = 1/2 (5 ŌłÆ p) and

Supply : x = 2pŌĆō3

Solution:

Example 6.4

For the demand function x=20/P+1, find the elasticity of demand

with respect to price at a point p =

3. Examine whether the demand is elastic at p

= 3.

Solution:

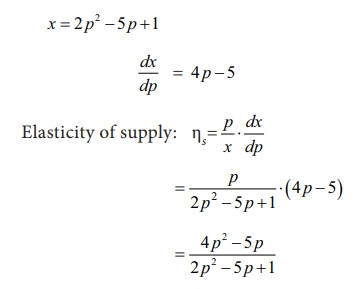

Example 6.5

Find the elasticity of supply for

the supply function x = 2p2 - 5 p + 1

Solution:

Example 6.6

Example 6.7

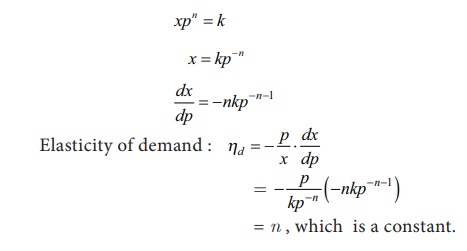

A demand function is given by xpn = k where n and k are constants. Prove that elasticity

of demand is always constant.

Solution:

Example 6.8

For the given demand function p = 40ŌĆōx, find the value of the output when ╬Ęd =1

Solution:

Example 6.9

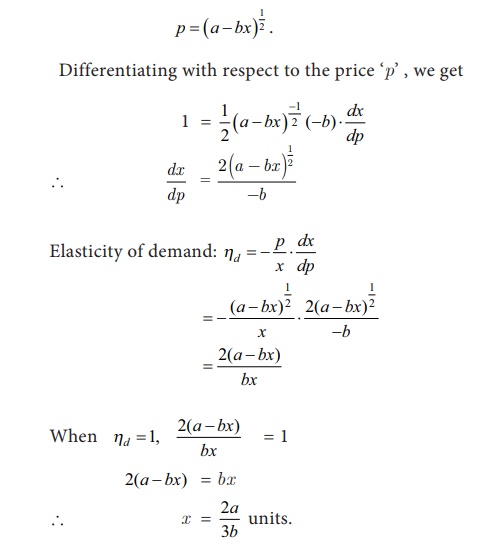

Find the elasticity of demand in

terms of x for the demand law p = (a-bx)1/2 . Also find the

values of x when elasticity of demand

is unity.

Solution:

Example 6.10

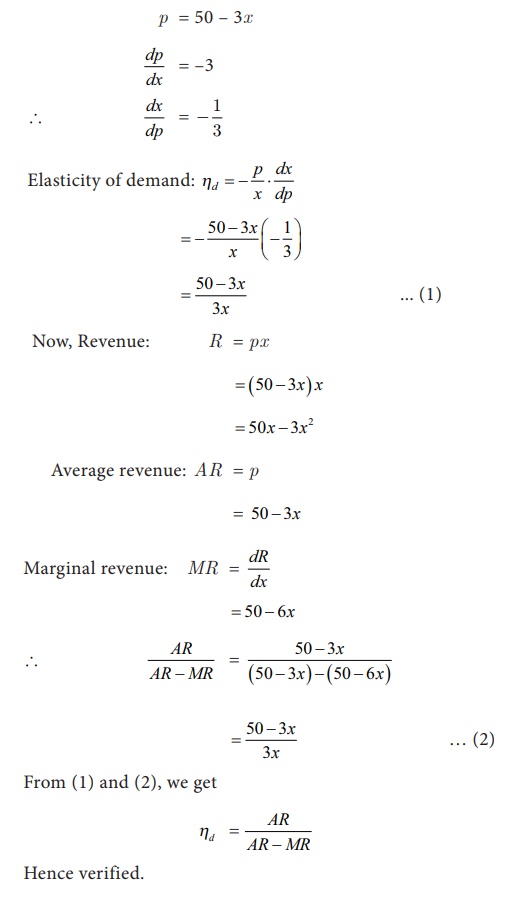

Verify the relationship of

elasticity of demand, average revenue and marginal revenue for the demand law p = 50 - 3x .

Solution:

Example 6.11

Find the elasticity of supply for

the supply law x = p / p+5 when p = 20

and interpret your result.

Interpretation:

┬Ę

z If the price increases by 1% from p = Ōé╣ 20, then

the quantity of supply increases by 0.2% approximately.

┬Ę

z If the price decreases by 1% from p = Ōé╣ 20, then

the quantity of supply decreases by 0.2% approximately.

Example 6.12

Example 6.13

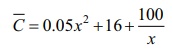

is the manufacturerŌĆÖs average cost function. What is the marginal cost when 50 units are produced and interpret your result.

is the manufacturerŌĆÖs average cost function. What is the marginal cost when 50 units are produced and interpret your result.

Solution:

Interpretation:

If the production level is

increased by one unit from x = 50,

then the cost of additional unit is approximately equal to Ōé╣ 391.

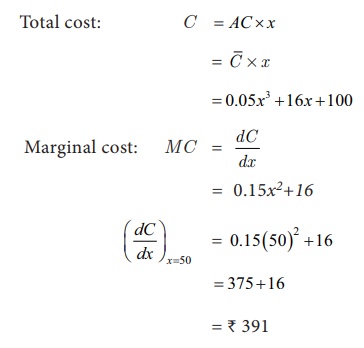

Example 6.14

For the function y x3+19,

find the values of x when its

marginal value is equal to 27.

Solution:

Example 6.15

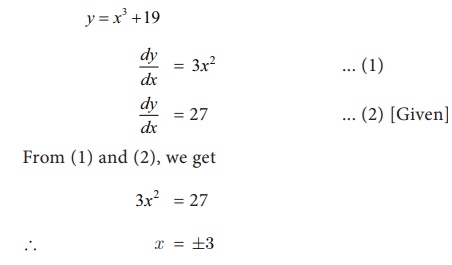

The demand function for a

commodity is p = 4/x,where

p is unit price. Find the

instantaneous rate of change of demand with respect to price at p=4. Also interpret your result.

Solution:

Rate of change of demand with

respect to the price at p

= Ōé╣ 4 is ŌłÆ 0.25

Interpretation:

When the price increases by 1%

from the level of p = Ōé╣ 4, the demand decreases (falls)

by 0.25%

Example 6.16

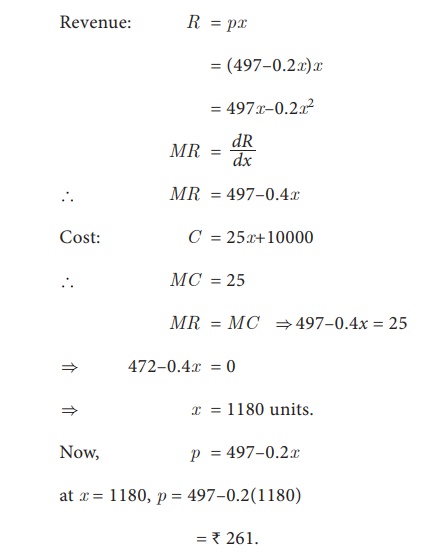

The demand and the cost function

of a firm are p = 497-0.2x and C = 25x+10000

respectively. Find the output level and price at which the profit is maximum.

Solution:

We know that profit is maximum

when marginal revenue [MR] = marginal cost [MC].

Revenue: R = px

Example 6.17

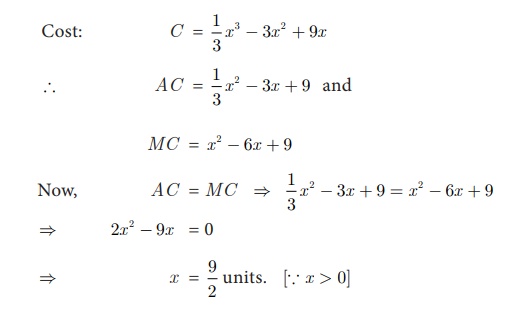

The cost function of a firm is C = 1/3 x3 ŌłÆ 3x2 + 9x . Find the level of output (x>0)

when average cost is minimum.

Solution:

We know that average cost [AC] is

minimum when average cost [AC] = marginal cost [MC].

Related Topics