Applications of differentiation in business and economics - Demand, supply, cost, revenue and profit functions | 11th Business Mathematics and Statistics(EMS) : Chapter 6 : Applications of Differentiation

Chapter: 11th Business Mathematics and Statistics(EMS) : Chapter 6 : Applications of Differentiation

Demand, supply, cost, revenue and profit functions

Demand, supply, cost, revenue and

profit functions

Demand function

In a market, the quantity of a

commodity demanded by the consumer depends on its price. If the price of the

commodity increases, then the demand decreases and if the price of the

commodity decreases, then the demand increases.

The relationship between the

quantity and the unit price of a commodity demanded by consumer is called as demand function

and is defined as x = f ( p) or p = f (x)

, where x>0 and p>0 .

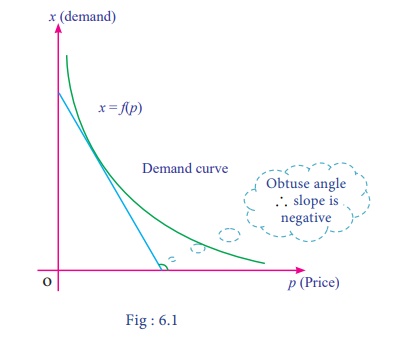

Graph of the demand function, x

= f(p)

Observations

(i) Price

and quantity of the demand function are in inverse variation.

(ii) The

graph of the demand function lies only in first quadrant.

(iii) Angle

made by any tangent to the demand curve with respect to the positive direction

of x ŌĆō axis is always an obtuse

angle.

(iv) Slope of the demand curve is

negative( ŌĆōve).

Supply function

In a market, the quantity of a

commodity supplied by producer depends on its price. If the price of the

commodity increases, then quantity of supply increases and if the price of the

commodity decreases, then quantity of supply decreases.

The relationship between the

quantity and the unit price of a commodity supplied by producer is called as supply function

and is defined as x = g(p)

or p=g(x) where x > 0 and p > 0

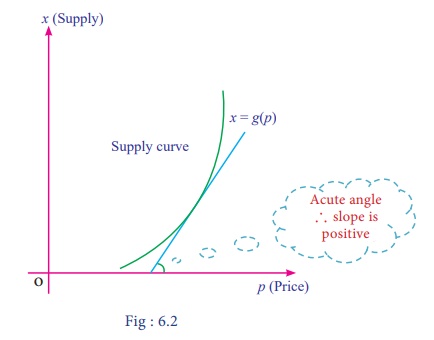

The graph of the supply function, x= g(p)

Observations

(i) Price

and quantity of the supply function are in direct variation.

(ii) The

graph of supply function lies only in first quadrant.

(iii) Angle

made by any tangent to the supply curve with respect to positive direction of x ŌĆō axis is always an acute angle.

(iv) Slope of the supply curve is

positive (+ve).

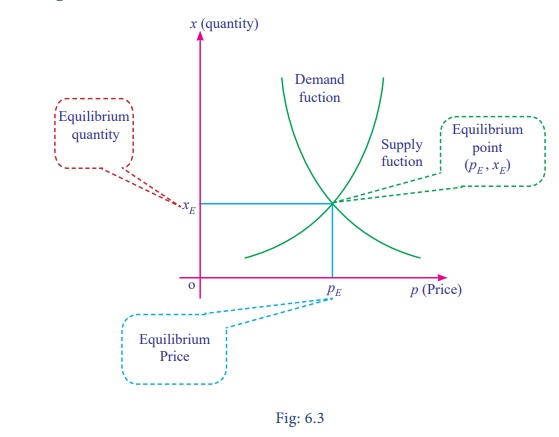

Equilibrium Price

The price at which the demand for

a commodity is equal to its supply is called as Equilibrium Price and is

denoted by pE.

Equilibrium Quantity

The quantity at which the demand

for a commodity is equal to its supply is called as Equilibrium Quantity and is

denoted by xE.

NOTE

Usually the demand

and supply functions are expressed as x

in terms of p, so the equilibrium

quantity is obtained either from the demand function (or) from the supply

function by substituting the equilibrium price.

Equilibrium Point

The point of intersection of the

demand and supply function (pE,

xE) is called as

equilibrium point.

Diagrammatical explanation of equilibrium price, equilibrium quantity and equilibrium point

Average and Marginal concepts

Usually, the variation in the

dependent quantity ŌĆśyŌĆÖ with respect

to the independent quantity ŌĆśxŌĆÖ can

be described in terms of two concepts namely

(i) Average concept and

(ii) Marginal concept.

(i) Average concept

The average concept expressed as

the variation of y over a whole range

of x and is denoted by y/x .

(ii) Marginal concept

The marginal concept expressed as

the instantaneous rate of change of y

with respect to x and is denoted by dy/dx .

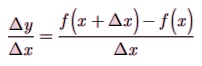

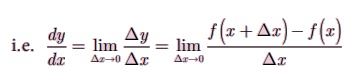

Remark:

If Ōłåx be the small change in x

and Ōłåy be the corresponding change in

y of the function y=f(x), then

Instantaneous rate of change of y with respect to x is defined as the limiting case of ratio of the change in y to the change in x.

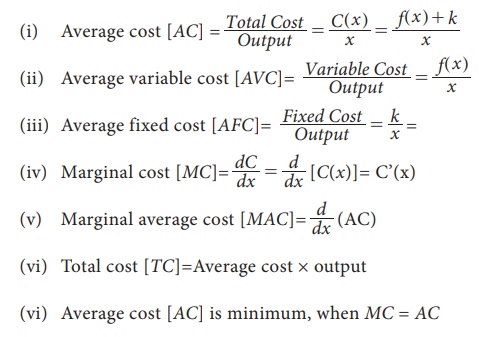

Cost function

The amount spent for the

production of a commodity is called its cost function.

Normally, total cost function [TC] consists of two parts.

(i) Variable cost

(ii) Fixed cost

Variable cost

Variable cost is the cost which

varies almost in direct proportion to the volume of production.

Fixed cost

Fixed cost is the cost which does

not vary directly with the volume of production.

If f(x) be the variable cost

and k be the fixed cost for

production of x units, then total

cost is C(x) = f(x) + k,

x>0.

NOTE

(i) Variable cost f(x) is a single valued function.

(ii) Fixed cost k is

independent of the level of output.

(iii) f(x) does not contain constant term.

Some standard results

If C(x) = f(x)

+ k be the total cost function, then

(vi) Total cost [TC]=Average cost ├Ś output

(vii) Average cost [AC] is minimum, when MC =

AC

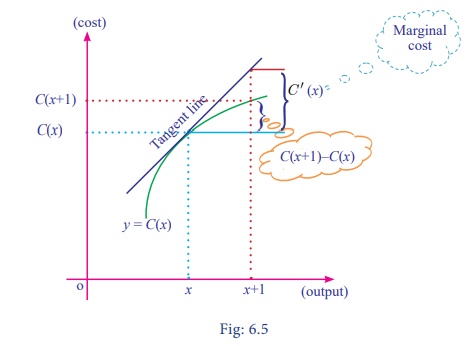

Remark:

The marginal cost [MC] is approximately equal to the

additional production cost of (x+1)th

unit, when the production level is x

units.

Diagrammatical explanation of marginal cost [MC]

Marginal cost is the change in

aggregate cost when the volume of production is increased or decreased by one

unit.

Revenue function

Revenue is the amount realised on

a commodity when it is produced and sold. If x is the number of units produced and sold and p is its unit price, then the total revenue function R(x)

is defined as R(x) =px, where x and p are positive.

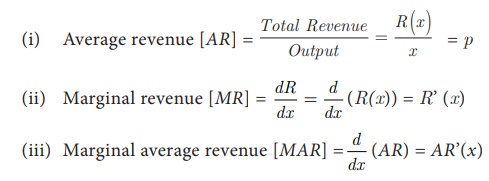

Some standard results

If R(x) =px be the revenue function, then

Remarks:

(i) Average revenue

[AR] and price [p] are the same. [i.e. AR=p]

(ii) The marginal

revenue [MR] is approximately equal

to the additional revenue made on selling of (x+1)th unit, whenx

the sales level is x units.

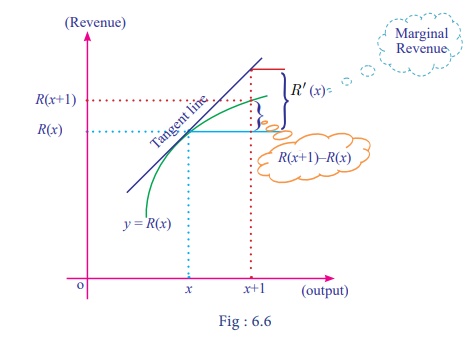

Diagrammatical explanation of Marginal Revenue [MR]

Marginal revenue is the change in

aggregate revenue when the volume of selling unit is increased by one unit.

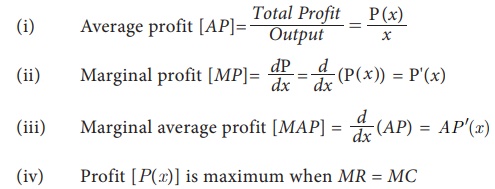

Profit function

The excess of total revenue over

the total cost of production is called the profit. If R(x) is the total revenue

and C(x) is the total cost, then profit function P(x) is defined as P(x) = R(x) ŌĆō C(x)

Some standard results

If P(x) = R(x) ŌĆō C(x) be the profit function, then

(iv) Profit [P(x)] is maximum when MR = MC

Related Topics