Banking - Central Bank | 12th Economics : Chapter 6 : Banking

Chapter: 12th Economics : Chapter 6 : Banking

Central Bank

Central Bank

A central bank, reserve bank, or monetary authority is an

institution that manages a state’s currency, money supply, and interest rates.

Central banks also usually oversee the commercial banking system of their

respective countries.

1. Functions of Central Bank (Reserve Bank of India)

The Reserve Bank of India (RBI) is India’s central banking

institution, which controls the monetary policy of the Indian rupee. It

commenced its operations on 1 April 1935 in accordance with the Reserve Bank of

India Act, 1934. The original share capital was divided into shares of ₹100

each fully paid, which were initially owned entirely by private shareholders.

Following India’s independence on 15 August 1947, the RBI was nationalised on 1

January 1949.

1. Monetary Authority: It controls the supply of money in the

economy to stabilize exchange rate, maintain healthy balance of payment, attain

financial stability, control inflation, strengthen banking system.

2. The issuer of currency: The objective is to maintain the currency

and credit system of the country. It is the sole authority to issue currency.

It also takes action to control the circulation of fake currency.

3. The issuer of Banking License: As per Sec 22 of Banking Regulation Act, every bank has to obtain a banking license from RBI to conduct banking business in India.

4. Banker to the Government: It acts as banker both to the central and

the state governments. It provides short-term credit. It manages all new issues

of government loans, servicing the government debt outstanding and nurturing

the market for government securities. It advises the government on banking and

financial subjects.

5. Banker’s Bank: RBI is the bank of all banks in India as

it provides loan to banks, accept the deposit of banks, and rediscount the

bills of banks.

6. Lender of last resort: The banks can borrow from the RBI by

keeping eligible securities as collateral at the time of need or crisis, when

there is no other source.

7. Act as clearing house: For settlement of banking transactions,

RBI manages 14 clearing houses. It facilitates the exchange of instruments and

processing of payment instructions.

8. Custodian of foreign exchange reserves: It acts as a custodian

of FOREX. It administers and enforces the provision of Foreign Exchange

Management Act (FEMA), 1999. RBI buys and sells foreign currency to maintain

the exchange rate of Indian rupee v/s foreign currencies.

9. Regulator of Economy: It controls the money supply in the

system, monitors different key indicators like GDP, Inflation, etc.

10. Managing Government securities: RBI administers

investments in institutions when they invest specified minimum proportions of

their total assets/liabilities in government securities.

11. Regulator and Supervisor of Payment and Settlement Systems: The Payment and

Settlement Systems Act of 2007 (PSS Act) gives RBI oversight authority for the

payment and settlement systems in the country. RBI focuses on the development

and functioning of safe, secure and efficient payment and settlement

mechanisms.

12. Developmental Role:

This

role includes the development of the quality banking system

in India and ensuring that credit is available to the productive sectors of the

economy. It provides a wide range of promotional functions to support national

objectives. It also includes establishing institutions designed to build the

country’s financial infrastructure. It also helps in expanding access to

affordable financial services and promoting financial education and literacy.

13. Publisher of monetary data and other data: RBI maintains and provides

all essential banking and other economic data, formulating and critically

evaluating the economic policies in India. RBI collects, collates and publishes

data regularly.

14. Exchange manager and controller: RBI represents India as

a member of the International Monetary Fund [IMF]. Most of the commercial banks

are authorized dealers of RBI.

15. Banking Ombudsman Scheme: RBI introduced the Banking Ombudsman

Scheme in 1995. Under this scheme, the complainants can file their complaints

in any form, including online and can also appeal to the Ombudsman against the

awards and the other decisions of the Banks.

16. Banking Codes and Standards Board of India: To measure the

performance of banks against Codes and standards based on established

global practices, the RBI has set up the Banking Codes and Standards Board of

India (BCSBI).

2. Credit Control Measures

Credit control is the primary mechanism available to the Central

banks to realize the objectives of monetary management. The RBI is much better

placed than many of credit control. The statutory basis for the control of the

credit system by the Reserve Bank is embodied in the Reserve Bank of India Act,

1934 and the Banking Regulation Act, 1949.

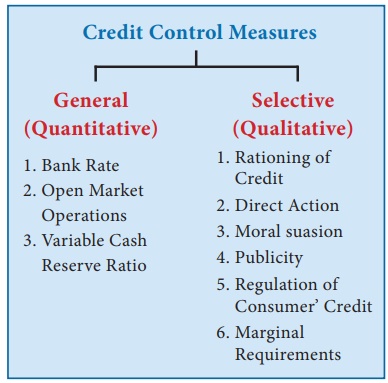

3. Methods of Credit Control

I. Quantitative or General Methods:

1. Bank Rate Policy:

The bank rate is the rate at which the Central Bank of a country

is prepared to re-discount the first class securities. It means the bank is

prepared to advance loans on approved securities to its member banks. As the

Central Bank is only the lender of the last resort the bank rate is normally

higher than the market rate. For example: If the Central Bank wants to control

credit, it will raise the bank rate. As a result, the deposit rate and other

lending rates in the money-market will go up. Borrowing will be discouraged,

and will lead to contraction of credit and vice versa.

2. Open Market Operations:

In narrow sense, the Central Bank starts the purchase and

sale of Government securities in the money market.

In Broad Sense, the Central Bank purchases and sells not

only Government securities but also other proper eligible securities like bills

and securities of private concerns. When the banks and the private individuals

purchase these securities they have to make payments for these securities to

the Central Bank.

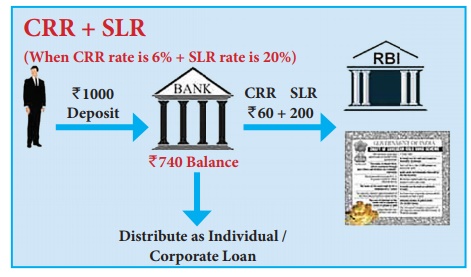

3. Variable Reserve Ratio:

a) Cash Reserves Ratio:

Under this system the Central Bank controls credit by changing the

Cash Reserves Ratio. For example, if the Commercial Banks have excessive cash

reserves on the basis of which they are creating too much of credit,this will

be harmful for the larger interest of the economy. So it will raise the cash

reserve ratio which the Commercial Banks are required to maintain with the

Central Bank.

Similarly, when the Central Bank desires that the Commercial Banks

should increase the volume of credit in order to bring about an economic

revival in the economy. The central Bank will lower down the Cash Reserve Ratio

with a view to expand the lending capacity of the Commercial Banks.

Variable Cash Reserve Ratio as an objective of monetary policy was

first suggested by J.M. Keynes. It was first followed by Federal Reserve System

in United States of America. The commercial banks as per the statute has to

maintain reserves based on their demand deposit and fixed deposit with central

bank is called as Cash Reserve Ratio.

If the CRR is high, the commercial bank’s capacity to create

credit will be less and if the CRR is low, the commercial bank’s capacity to

create credit will be high.

b) Statutory Liquidity Ratio:

Statutory Liquidity Ratio (SLR) is the amount which a bank has to

maintain in the form of cash, gold or approved securities. The quantum is specified

as some percentage of the total demand and time liabilities (i.e., the

liabilities of the bank which are payable on demand anytime, and those

liabilities which are accruing in one month’s time due to maturity) of a bank.

II. Qualitative or Selective Method of Credit Control:

The qualitative or the selective methods are directed towards the

diversion of credit into particular uses or channels in the economy. Their

objective is mainly to control and regulate the flow of credit into particular

industries or businesses. The following are the frequent methods of credit

control under selective method:

1.

Rationing of Credit

2.

Direct Action

3.

Moral Persuasion

4.

Method of Publicity

5.

Regulation of Consumer’s Credit

6.

Regulating the Marginal Requirements on Security Loans

1. Rationing of Credit

This is the oldest method of credit control. Rationing of credit

as an instrument of credit control was first used by the Bank of England by the

end of the 18th Century. It aims to control and regulate the purposes for which

credit is granted by commercial banks. It is generally of two types.

a) The variable portfolio ceiling: It refers to the

system by which the central bank fixes ceiling or maximum amount of loans and

advances for every commercial bank.

b) The variable capital asset ratio: It refers to the

system by which the central bank fixes the ratio which the capital of the

commercial bank should have to the total assets of the bank.

2. Direct Action

Direct action against the erring banks can take the following

forms.

a) The central bank may refuse to altogether grant discounting

facilities to such banks.

b) The central bank may refuse to sanction further financial

accommodation to a bank whose existing borrowing are found to be in excess of

its capital and reserves.

c) The central bank may start charging penal rate of interest on

money borrowed by a bank beyond the prescribed limit.

3. Moral Suasion

This method is frequently adopted by the Central Bank to exercise

control over the Commercial Banks. Under this method Central Bank gives advice,

then requests. and persuades the Commercial Banks to co-operate with the

Central Bank in implementing its credit policies.

4. Publicity

Central Bank in order to make their policies successful, take the

course of the medium of publicity. A policy can be effectively successful only

when an effective public opinion is created in its favour.

5. Regulation of Consumer’s Credit:

The down payment is raised and the number of installments reduced

for the credit sale.

6. Changes in the Marginal Requirements on Security Loans:

This system is mostly followed in U.S.A. Under this system, the

Board of Governors of the Federal Reserve System has been given the power to

prescribe margin requirements for the purpose of preventing an excessive use of

credit for stock exchange speculation.

This system is specially intended to help the Central Bank in

controlling the volume of credit used for speculation in securities under the

Securities Exchange Act, 1934.

The Repo Rate and the Reverse Repo Rate are the frequently used

tools with which the RBI can control the availability and the supply of money

in the economy. RR is always greater than RRR in India

Repo Rate: (RR)

The rate at which the RBI is willing to lend to commercial banks

is called Repo Rate. Whenever banks have any shortage of funds they can borrow

from the RBI, against securities. If the RBI increases the Repo Rate, it makes

borrowing expensive for banks and vice versa. As a tool to control inflation,

RBI increases the Repo Rate, making it more expensive for the banks to borrow

from the RBI. Similarly, the RBI will do the exact opposite in a deflationary

environment.

Reverse Repo Rate: (RRR)

The rate at which the RBI is willing to borrow from the commercial banks is called reverse repo rate. If the RBI increases the reverse repo rate, it means that the RBI is willing to offer lucrative interest rate to banks to park their money with the RBI. This results in a decrease in the amount of money available for banks customers as banks prefer to park their money with the RBI as it involves higher safety. This naturally leads to a higher rate of interest which the banks will demand from their customers for lending money to them.

4. Reserve Bank of India and Rural Credit

In a developing economy like India, the Central bank of the

country cannot confine itself to the monetary regulation only, and it is

expected that it should take part in development function in all sectors

especially in the agriculture and industry.

5. Role of RBI in agricultural credit

RBI has been playing a very vital role in the provision of

agricultural finance in the country. The Bank’s responsibility in this field

had been increased due to the predominance of agriculture in the Indian economy

and the inadequacy of the formal agencies to cater to the huge requirements of

the sector. In order to fulfill this important role effectively, the RBI set up

a separate Agriculture Credit Department. However, the volume of

informal loans has not declined sufficiently.

6. Functions of Agriculture Credit Department:

a) To maintain an expert staff to study all questions on

agricultural credit;

b) To provide expert advice to Central and State Government, State

Co-operative Banks and other banking activities.

c) To finance the rural sector through eligible institutions

engaged in the business of agricultural credit and to co-ordinate their

activities.

The duties of the RBI in agricultural credit were much restricted

as it had to function only in an ex -officio capacity being the Central Bank of

the country. It could not lend directly to the farmers, but the supply of rural

credit was done through the mechanism of refinance with institutions

specializing in rural credit. Primary societies may borrow from Central

Co-operative Bank, and the latter may borrow from the apex or the State

Co-operative Bank, which in its turn might get accommodation facilities from

the RBI.

The RBI was providing medium-term loans also for a period

exceeding 15 months to 5 years for reclamation of land, construction of irrigation

works, purchase of machinery, etc.

The Reserve Bank of India was also providing long-term loans to

fiancé permanent changes in land and also for the redemption of old debts.

With the establishment of National Bank for Agriculture and

Rural Development (NABARD), all the functions of the RBIrelating to

agricultural credit had been taken over and looked after by NABARD since 1982.

Since then, all activities relating to rural credit are entirely looked after

by NABARD.

Related Topics