Chapter: 11th Auditing : Chapter 1 : Introduction to Audit

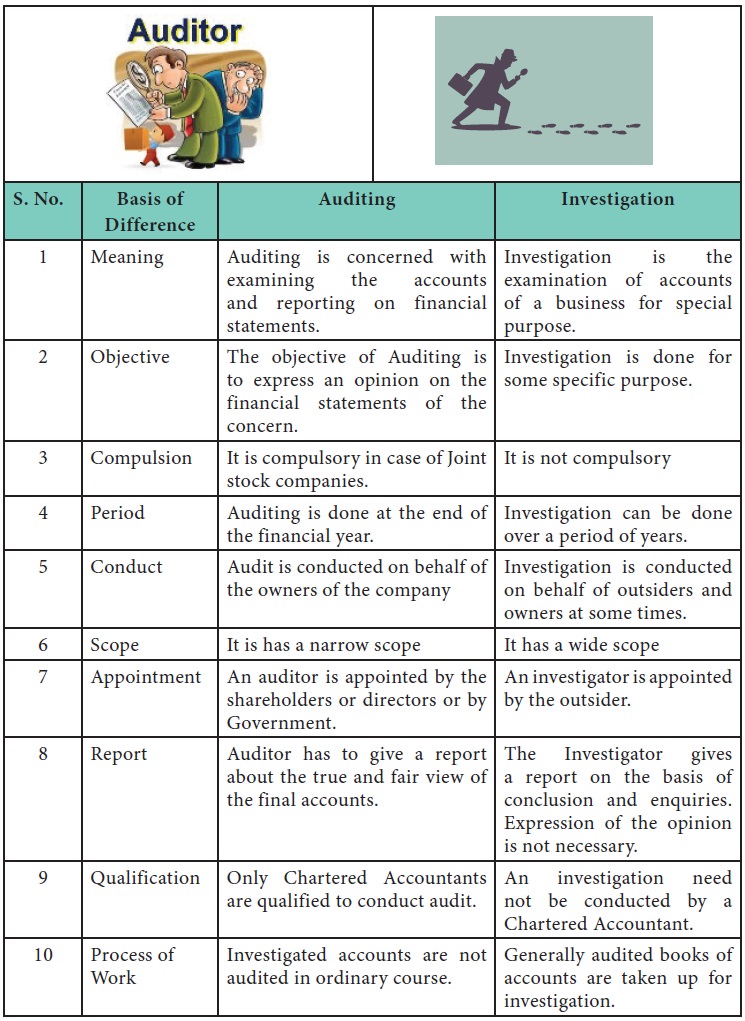

Differences between Auditing and Investigation

Differences between Auditing and

Investigation

Auditing Vs Investigation

1 Meaning

Auditing:

Auditing

is concerned with examining the accounts and reporting on financial statements.

Investigation:

Investigation is the examination of accounts of a business for special purpose.

2 Objective

Auditing:

The

objective of Auditing is to express an opinion on the financial statements of

the concern.

Investigation:

Investigation is done for some specific purpose.

3 Compulsion

Auditing:

It is

compulsory in case of Joint stock companies.

Investigation: It is

not compulsory

4 Period

Auditing:

Auditing

is done at the end of the financial year.

Investigation:

Investigation can be done over a period of years.

5 Conduct

Auditing:

Audit is

conducted on behalf of the owners of the company

Investigation:

Investigation is conducted on behalf of outsiders and owners at some times.

6 Scope

Auditing:

It is has

a narrow scope

Investigation: It has a

wide scope

7 Appointment

Auditing:

An

auditor is appointed by the shareholders or directors or by Government.

Investigation: An

investigator is appointed by the outsider.

8 Report

Auditing:

Auditor

has to give a report about the true and fair view of the final accounts.

Investigation: The

Investigator gives a report on the basis of conclusion and enquiries.

Expression of the opinion is not necessary.

9 Qualification

Auditing:

Only

Chartered Accountants are qualified to conduct audit.

Investigation: An

investigation need not be conducted by a Chartered Accountant.

10 Process of Work

Auditing:

Investigated

accounts are not audited in ordinary course.

Investigation:

Generally audited books of accounts are taken up for investigation.

Related Topics