Definitions, Types, Budgetary Procedure, Budgetary Deficits - Economics - Budget | 12th Economics : Chapter 9 : Fiscal Economics

Chapter: 12th Economics : Chapter 9 : Fiscal Economics

Budget

Budget

The word ‘budget’ is said to have its origin from the French word

“Bougett” which refers to ‘a small leather bag’. The budget is an annual

financial statement which shows the estimated income and expenditure of the

Government for the forthcoming financial year.

1. Definitions

“It is a document containing a preliminary approved plan of public

revenue and expenditure”.-Reney Stourn.

“The budget has come to mean the financial arrangements of a given

period, with the usual implication that they have been submitted to the

legislature for approval”.- Bastabale

2. Union Budget and State Budget

India is a federal economy, hence public budget is divided into

two layers of the Government. According to the Indian Constitution, the Central

Government has to submit annual financial statement, i.e., Union Budget under

Article 112 to the Parliament and each State Government has to submit the same

for the State in the Legislative Assembly under Article 202.

3. Types of Budget

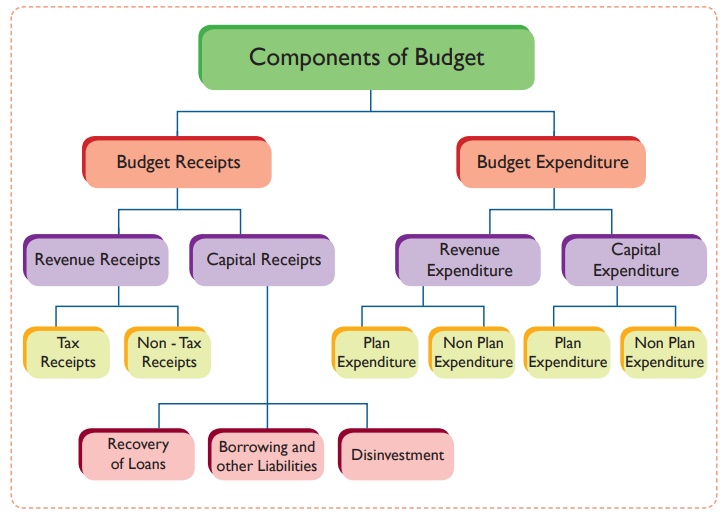

Revenue and Capital Budget

On the basis of expenditure on revenue account and other accounts,

a budget can be presented in two ways:

i) Revenue Budget: It consists of revenue receipts and

revenue expenditure. Moreover, the revenue receipts can be categorised into tax

revenue and non-tax revenue. Revenue expenditure can also be categorised into

plan revenue expenditure and non-plan revenue expenditure.

ii) Capital Budget: It consists of capital receipts and

capital expenditure. In this case, the main sources of capital receipts are

loans, advances etc. On the other side capital expenditure can be categorised

into plan capital expenditure and non-plan capital expenditure.

iii) Supplementary Budget: During the time of war emergencies and

natural calamities like tsunami, flood etc, the expenditures allotted in the

budget provisions are not always enough. Under these circumstances, a

supplementary budget can be presented by the Government to tackle these

unforeseen events.

iv) Vote - on - Account: Under Article 116 of the Indian

Constitution, the budget can be presented in the middle of the year. The reason

may be political in nature. The existing Government may or may not continue for

the year, on account of the fact that elections are due, then the Government places

a ‘lame duck budget’. This is also called ‘Vote-on-account Budget’.

The vote on account budget is a special provision by which the

Government gets permission from the parliament to incur expenditures on

necessary items till the budget is finally passed in the parliament. The legal

permission of both the Houses of the parliament for the withdrawal of money

from the Consolidated Fund of India to meet the requisite expenses till the

budget is finally approved is known as vote-on - account budget. This type of

budget is generally sanctioned for not more than two months.

v) Zero Base Budget: The Government of India presented

Zero-Base-Budgeting (ZBB first) in 1987-88. It involves fresh evaluation of

expenditure in the Government budget, assuming it as a new item. The review has

been made to provide whole in the light of the socio-economic objectives

which have been already set up for this project and as well as in view of the

priorities of the society.

vi) Performance Budget: When the outcome of any activity is taken

as the base of any budget, such budget is known as ‘Performance Budget’. For

the first time in the world, the performance budget was made in USA. The

Administrative Reforms Commission was set up in 1949 in America under Sir Hooper.

This commission recommended making of a ‘Performance Budget’ in USA. In

the Performance Budget, it is the compulsion of the government to tell ‘what is

done’, ‘how much done’ for the betterment of the people. In India, the

Performance Budget is also known as ‘Outcome Budget’.

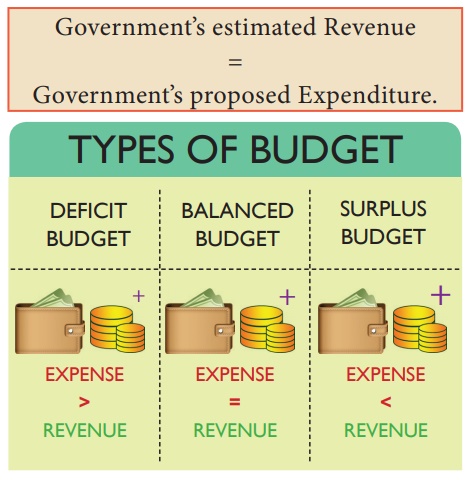

vii) Balanced Budget Vs Unbalanced Budget

A. Balanced Budget

Balanced budget is a situation, in which estimated revenue of the

government during the year is equal to its anticipated expenditure.

B. Unbalanced Budget

The budget in which Revenue & Expenditure are not equal to

each other is known as Unbalanced Budget.

Unbalanced budget is of two types:

1. Surplus Budget

2. Deficit Budget

1. Surplus Budget

The budget is a surplus budget when the estimated revenues of the

year are greater than anticipated expenditures.

Government Estimated revenue > Estimated Government

Expenditure.

2. Deficit Budget

Deficit budget is one where the estimated government expenditure

is more than expected revenue.

Government’s estimated Revenue < Government’s proposed

Expenditure.

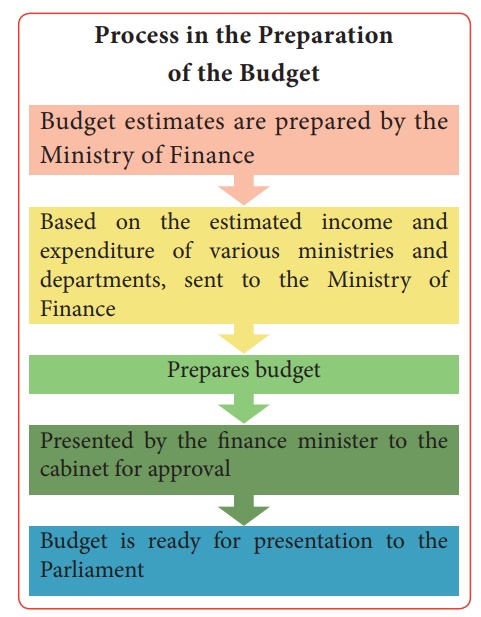

4. Budgetary Procedure

Budgetary procedure refers to the system through which the budget

is prepared, enacted and executed.

(A) Preparation of the Budget

The Ministry of Finance prepares the Central Budget every year. At

the state level the finance department is responsible for the Annual State

Budget. While preparing the budget, the following factors are taken into

account:

·

The macro economic targets to be achieved within a plan period;

·

The basic strategy of the budget;

·

The financial requirements of different projects;

·

Estimates of the revenue expenditures (includes defence

expenditure, subsidy, interest payment on debt etc.);

·

Estimates of the capital expenditures (includes development of

railways, roadways, irrigations etc.);

·

Estimates of revenue receipts from tax and non-tax revenues;

·

Estimates of capital receipts from the recovery of loans,

disinvestment of public sector units, market borrowings etc.

·

Estimates of the gap between revenue receipts and revenue

expenditure; and

·

Estimates of fiscal deficit, primary deficit, and revenue deficit.

(B) Presentation of the Budget

The hon’ble Minister of Finance, on behalf of the Central

Government, places the Union Budget before Parliament on the eve of a new

financial year. Similarly at state levels, the Hon’ble Finance Minister of the

respective State Government places the State Budget before the State

Legislature.

According to the Indian Constitution, all money bills must be

initiated in the Lower House. All the money bills are first placed before the

LokSabha at the Centre, and before the VidhanSabha at the State level. The

demands of various tax proposals are included in the budget. After the finance

bill is passed, an appropriation bill is presented to give legal effect to the

voted demands, and to authorise the expenditure as per the budget. In this way,

the budgets are enacted in India.

(c) Execution of the Budget

The budget is mainly executed by different departments of the

Government. Proper execution of the budgetary provisions are important for the

efficient utilisation of the allocated funds.

Parliamentary Control over the Budget

In India, the Government Accounts are maintained in three parts:

(i) Consolidated Fund

(ii) Contingency Fund

(iii) Public Accounts

There are also two committees of parliament, viz,

(i) The Public Accounts Committee, and

(ii)The Estimates Committee.

These committees keep a constant vigil on the expenditure so that

no Ministry or Department exceeds the amount sanctioned to it.

5. Budgetary Deficits

Budget deficit is a situation where budget receipts are less than

budget expenditures. This situation is also known as government deficit.

In reference to the Indian Government budget, budget deficit is of

four major types.

(a) Revenue Deficit

(b) Budget Deficit

(c) Fiscal Deficit, and

(d) Primary Deficit

(A) Revenue Deficit

It refers to the excess of the government revenue expenditure over

revenue receipts. It does not consider capital receipts and capital expenditure.

Revenue deficit implies that the government is living beyond its means to

conduct day-to-day operations.

Revenue Deficit (RD) = Total Revenue Expenditure (RE) - Total

Revenue Receipts (RR),

When RE - RR > 0

(B) Budget Deficit

Budget deficit is the difference between total receipts and total

expenditure (both revenue and capital)

Budget Deficit = Total Expenditure – Total Revenue

(C) Fiscal Deficit

Fiscal deficit (FD) = Budget deficit + Government’s market

borrowings and liabilities

(D ) Primary Deficit

Primary deficit is equal to fiscal deficit minus interest

payments. It shows the real burden of the government and it does not include

the interest burden on loans taken in the past. Thus, primary deficit reflects

borrowing requirement of the government exclusive of interest payments.

Primary Deficit (PD) = Fiscal deficit (PD) - Interest Payment

(IP)

Related Topics