Different methods, Example, Merits, Limitations, Example Illustration, Solution | Accountancy - Methods of providing depreciation | 11th Accountancy : Chapter 10 : Depreciation Accounting

Chapter: 11th Accountancy : Chapter 10 : Depreciation Accounting

Methods of providing depreciation

Methods of providing depreciation

There are various methods used for providing depreciation on fixed

assets. The management of a business enterprise has to select the most

appropriate method based on the consideration of various factors such as nature

of the asset, use of the asset and circumstances that prevail in the business.

The following are the different methods of providing depreciation:

1.

Straight

line method or Fixed instalment method or Original cost method

2.

Written

down value method or Diminishing balance method

3.

Sum of

years of digits method

4.

Machine

hour rate method

5.

Depletion

method

6.

Annuity

method

7.

Revaluation

method

8.

Sinking

fund method

9.

Insurance

policy method

1. Straight line method/ Fixed instalment method / Original cost method

Under this method, a fixed percentage on the original cost of the asset

is charged every year by way of depreciation. Hence it is called original cost

method. As the amount of depreciation remains equal in all years over the

useful life of an asset it is also called as fixed instalment method. When the

amount of depreciation charged over its life is plotted on a graph and the

points are joined together, the graph will show a horizontal straight line.

Hence, it is called straight line method.

This method is suitable for those assets the useful life of which can be

estimated accurately and which do not require much expense on repairs and

renewals.

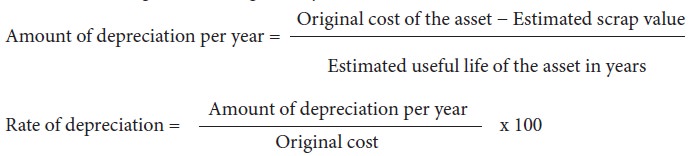

Under this method, the following

formulae are used for calculating the amount of depreciation and the rate of

depreciation respectively:

Tutorial note

·

In the year of purchase, if the period of use is

less than a year, the amount of depreciation will be charged proportionately

for the period for which the asset has been used in the business.

·

If depreciation is deducted from the cost of the

asset at the end of useful life of the asset the amount left in the asset

account will be equal to the scrap value if there is any scrap value or it will

be zero if there is no scrap value.

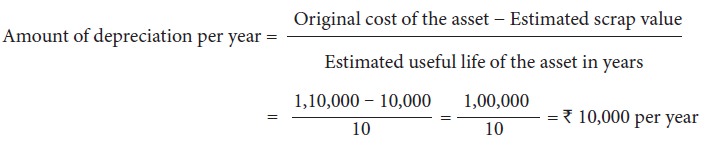

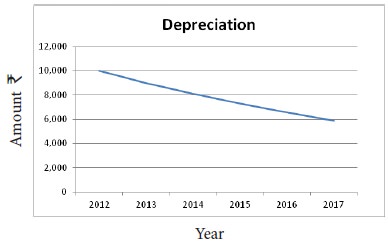

Example

On 1.1.2012, a firm purchased a

machine at a cost of Rs. 1,10,000. Its life was estimated to be 10

years with a scrap value of Rs. 10,000. The amount of depreciation to be

charged at the end of each year is:

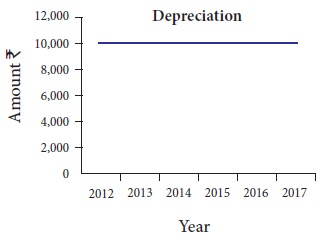

When it is plotted on a graph for

5 years, it appears as follows:

Merits

Following are the merits of

straight line method of depreciation:

(a)

Simple and easy to understand

Computation of depreciation under

this method is very simple and is easy to understand.

(b)

Equality of depreciation burden

Under this method, equal amount of depreciation is debited to the profit and loss account each year. Hence, the burden of depreciation on the profit of each year is equal.

(c) Assets can be completely written off

Under this method, the book value of an asset can be reduced to zero if

there is no scrap value or to the scrap value at the end of its useful life.

Thus the asset account can be completely written off.

(d)

Suitable for the assets having fixed working life

This method is appropriate for the fixed assets having certain fixed

period of working life. In such cases, the estimation of useful life is easy and

in turn it helps in easy determination of rate of depreciation.

Limitations

Following are the limitations of

straight line method of depreciation:

(a)

Ignores the actual use of the asset

Under this method, a fixed amount of depreciation is provided on each

asset by applying the predetermined rate of depreciation on its original cost.

But, the actual use of the asset is not considered in computation of

depreciation.

(b)

Ignores the interest factor

This method does not take into account the loss of interest on the

amount invested in the asset. That is, the amount would have earned interest,

had it been invested outside the business is not considered.

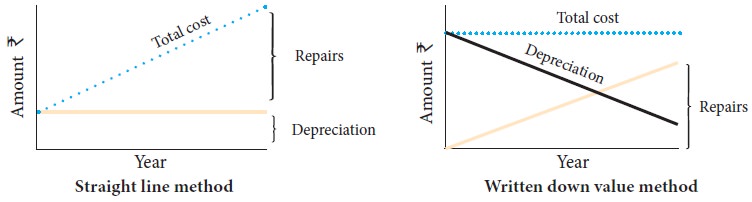

(c)

Total charge on the assets will be more when the asset becomes older

With the passage of time, the cost of maintenance of an asset goes up.

Hence, the amount of depreciation and cost of maintenance put together is less

in the initial period and goes up year after year. But, this method does not

consider this.

(d)

Difficulty in the determination of scrap value

It may be quite difficult to assess the true scrap value of the asset

after a long period say 10 or 15 years after the date of its installation.

Suitability

Straight line method of depreciation is suitable in case of fixed assets

in respect of which useful life can be determined and maintenance and repair

cost is the same throughout the life of the asset.

Illustration 1

On 1.1.2017 a firm purchased a machine at a cost of Rs. 1,00,000. Its life was estimated to be 10

years with a scrap value of Rs. 10,000.

Compute the amount of depreciation to be charged at the end of each year.

Solution

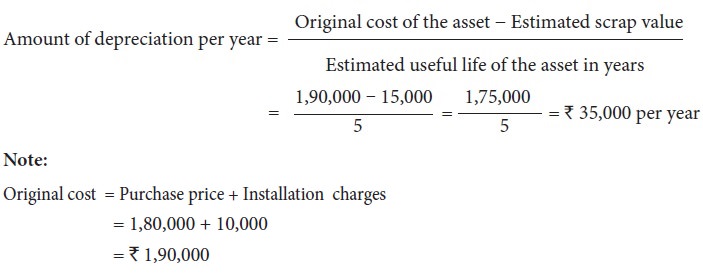

Illustration 2

A company has purchased a

machinery for Rs. 1,80,000 and

spent Rs. 10,000 for

its installation. The estimated life of the machinery is 5 years with a

residual value of Rs. 15,000. Find

out the amount of depreciation to be provided every year.

Solution

Note:

Original cost = Purchase price +

Installation charges

= 1,80,000

+ 10,000

= 1,90,000

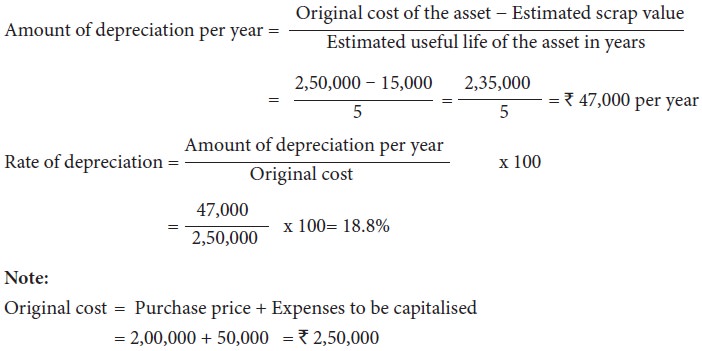

Illustration 3

From the following information, calculate the amount of depreciation and

rate of depreciation under straight line method.

Purchase price of machine Rs.

2,00,000

Expenses to be capitalised Rs.

50,000

Estimated residual value Rs.

15,000

Expected useful life 5

years

Solution

Illustration 4

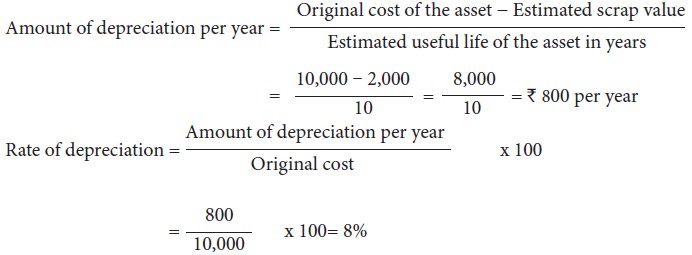

Find out the rate of depreciation under straight line method from the

following details:

Original cost of the asset = Rs. 10,000

Estimated life of the asset = 10 years

Estimated scrap value at the end = Rs. 2,000

Solution

2. Written down value / Diminishing balance method

Under this method, depreciation

is charged at a fixed percentage on the written down value of the asset every

year. Hence, it is called written down value method. Written down value is the

book value of the asset, i.e., original cost of the asset minus depreciation

upto the previous accounting period. As the amount of depreciation goes on

decreasing year after year, it is called diminishing balance method or reducing

installment method.

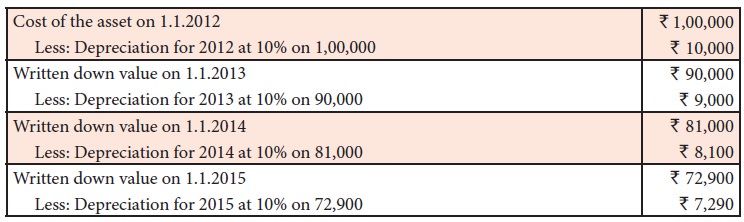

Example

On 1.1.2012, a firm purchased a

machine at a cost of Rs. 1,00,000. Depreciation charged at 10% p.a. on

written down value method for the five years is as follows:

Merits

Following are the merits of

written down value method.

(a) Equal

charge against income

In the initial years depreciation is high and repair charges are low. When the asset becomes older, the amount of depreciation charged is less but repair charges are high. Hence, the total burden on profit in respect of depreciation and repairs put together remains almost similar year after year.

(b) Logical method

In the earlier years, when the asset is more productive, high

depreciation is charged. In the later years when the asset becomes less

productive, the depreciation charge is less.

Limitations

Following are the limitations of written down value method.

(a) Assets

cannot be completely written off

Under this method, the value of an asset even if it becomes obsolete and

useless, cannot be reduced to zero and some balance would continue in the asset

account.

(b) Ignores

the interest factor

This method does not take into account the loss of interest on the

amount invested in the asset. The amount would have earned interest, had it

been invested outside the business is not considered.

(c)

Difficulty in determining the rate of depreciation

Under this method, the rate of providing depreciation cannot be easily

determined. The rate is generally kept higher because it takes very long time

to write off an asset down to its scrap value.

(d) Ignores

the actual use of the asset

Under this method, a fixed rate of depreciation is provided on the

written down value of the asset by applying the predetermined rate of

depreciation on its original cost. But, the actual use of the asset is not

considered in the computation of depreciation.

Suitability

This method is suitable in case of assets having a comparatively long

life and which require considerable repairs in the later years when they become

older. Examples are building and plant and machinery.

Illustration 5

A firm purchased a plant on

1.1.2018 for Rs. 9,000 and

spent Rs. 1,000 as

erection charges. Calculate the amount of depreciation for the year 2018 @ 15%

per annum under the written down value method. Accounts are closed on 31st

March every year.

Solution

Original cost = 9,000 +

1,000 = 10,000

Rate of depreciation = 15%

Date of purchase = 1.1.2018

Number of months used = 1.1.2018 to 31.03.2018 = 3 months

Amount of depreciation = 15% on 10,000 for 3 months

= 10,000 ×15% × 3/12 = Rs. 375

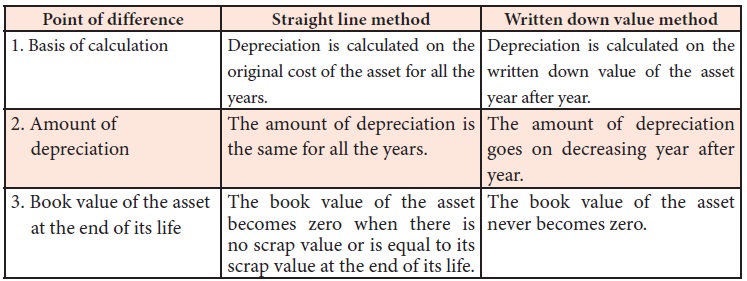

2.1 Differences between straight line method and written down value method

Following are the differences

between straight line method and written down value method

3. Sum of years of digits method

This method is similar to the diminishing balance method. The amount of

depreciation goes on decreasing year after year in proportion to the unexpired

life of the asset. This method is suitable for those assets having more

probability of obsolescence and increased repair charges as the assets grow

older. Under this method, amount of depreciation per year is calculated by

multiplying the cost of the asset and the number of remaining years of life and

dividing it by the sum of the digits of all years of life of the asset. The

following formula is used to compute the amount of depreciation under this

method:

4. Machine hour rate method

Under this method, depreciation per machine hour is calculated. The cost

of the machinery after deducting the residual value, if any, is divided by the

estimated working hours of the machine to find the depreciation per hour. The

actual depreciation for any given period depends upon the working hours during

that year. The special feature of this method is that depreciation is found

directly in proportion to the actual use of the asset. Under this method life

of the asset is estimated in hours and not in years. The following formula is

used to determine the rate of depreciation:

Amount of depreciation = Number

of machine hours used × Rate of depreciation per hour

5. Depletion method

Depletion means exhaustion of natural resources. That is, depletion

means quantitative reduction in the content of assets. This is applicable to

those assets that get exhausted due to extraction and exploitation. Examples:

mines, oil fields, etc. Under this method, depreciation rate is calculated on

the basis of the estimated quantities of the output during the whole life of

the asset.

Amount of depreciation = Units of

output during the year × Rate of depreciation per unit

Note: Even though

it is not depreciated, it is used to write off the cost of the asset as per matching principle.

6. Annuity method

Under this method, not only the original cost of the asset but also the

amount of interest on the investment is taken into account while computing

depreciation. The idea of considering interest is that if the investment is

made in any other asset instead of the relevant fixed asset, it would have

earned a certain rate of interest. To calculate the amount of depreciation,

annuity factor is used. Annuity factor can be found out from the annuity table

or by using formula.

Amount of depreciation is

computed as follows:

Amount of depreciation = Annuity

factor × Original cost of the asset

7. Revaluation method

Under this method, the amount of annual depreciation is calculated by

comparing the value of the assets at the end of the year and their value at the

beginning of the year. The value of the asset at the end of the year is

determined with the consultation of relevant experts. The excess of opening

value over the closing value of the asset is the amount of depreciation for

that year. This method is used for live stock, loose tools, etc.

8. Sinking fund method

This method is adopted especially when it is desired not merely to write

off an asset but also to provide enough funds to replace an asset at the end of

its working life. Under this method, the amount charged as depreciation is

transferred to depreciation fund and invested outside the business. The

investment is made in safe securities which offer a certain rate of interest.

Interest is received annually and reinvested every year along with the amount

of annual depreciation. On the expiry of the life of the asset, the investments

are sold and the sale proceeds are used for replacement of the asset. This

method of depreciation is suitable for assets of higher value. This method is

also known as depreciation fund method. Thus, this method not only takes into

account depreciation but also makes provision for the replacement of the asset.![]()

9. Insurance policy method

Under this method, an insurance policy is taken for an amount equal to

the cost of replacement of the asset. The amount of depreciation is paid by way

of insurance premium every year to the insurance company. On maturity of the

policy, the policy amount is received from the insurance company and it is used

for the purchase of new asset.

Related Topics