Result, Properties, Proof, Solved Example Problems - Mathematical expectation | 11th Statistics : Chapter 9 : Random Variables and Mathematical Expectation

Chapter: 11th Statistics : Chapter 9 : Random Variables and Mathematical Expectation

Mathematical expectation

Mathematical

expectation

Probability

distribution gives us an idea about the likely value of a random variable and

the probability of the various events related to random variable. Even though

it is necessary for us to explain probabilities using central tendencies,

dispersion, symmetry and kurtosis. These are called descriptive measures and

summary measures. Like frequency distribution we have to see the properties of

probability distribution. This section focuses on how to calculate these

summary measures. These measures can be calculated using

i. Mathematical Expectation and variance.

ii. Moment Generating Function .

iii. Characteristic Function.

Expectation of Discrete random variable

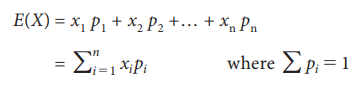

Let X be a discrete

random variable which takes the values x1,

x2 ….. xn with respective probabilities p1, p2 ….. pn

then mathematical expectation of X

denoted by E(X)is defined by

Sometimes E(X) is known as the mean of the random

vairable X.

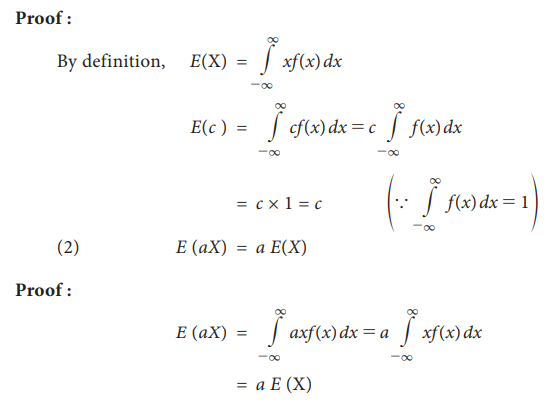

Result:

If g(X) is

a function of the random variable X, then E g(X) = Σg(x)p(X = x)

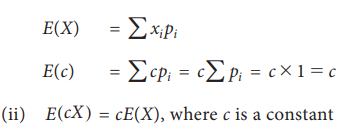

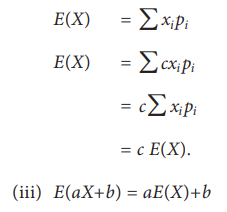

Properties:

E(c) = c where c is a constant

Proof:

Proof:

Variance of Discrete random variable

Definition: In a probability distribution Variance is the

average of sum of squares of deviations from the mean. The variance of the

random variable X can be defined as.

Var ( X ) = E (X

– E(X))2

= E (X2 ) – ( E(X))2

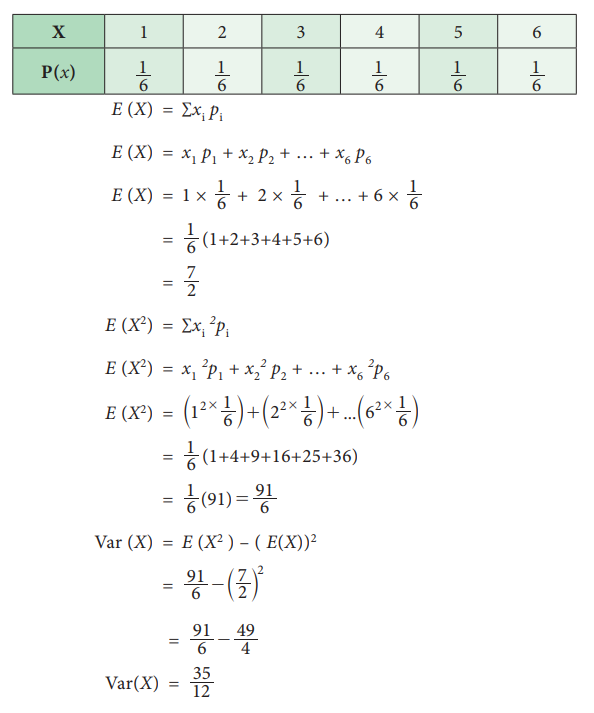

Example 9.18

When a die is thrown X

denotes the number turns up. Find E(X), E(X2) and Var(X).

Solution:

Let X denoted that

number turns up in a die.

X takes the values 1, 2, 3, 4, 5, 6 with probabilities 1/6 for

each.

Therefore the probability distribution is

Example 9.19

The

mean and standard deviation of a random variable X are 5 and 4 respectively Find E

(X2)

Solution:

Given

E (X) = 5 and σ = 4

`

Var (X) = 16

But,

Var (X) = E(X2) – [E(X)]2

16

= E (X2) – (5)2

E(X2)

= 25 + 16 = 41

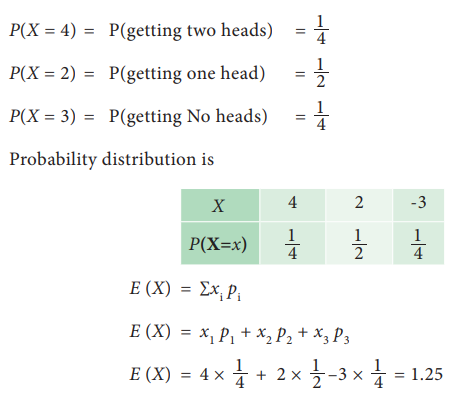

Example 9.20

A

player tosses two coins, if two head appears he wins ` 4, if one head appears

he wins ` 2, but if two tails appears he loses ` 3. Find the expected sum of

money he wins?

Solution:

Let

X be the random variable denoted the amount he wins.

The

possible values of X are 4, 2 and –3

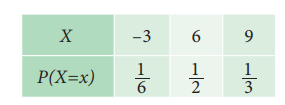

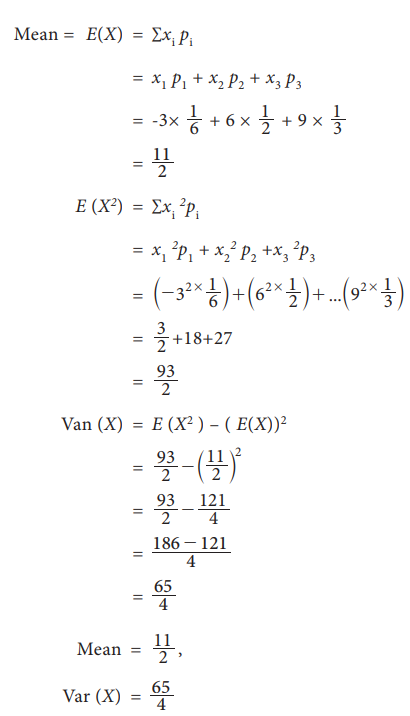

Example 9.21

Let X be a discrete

random variable with the following probability distribution

Find mean and variance

Solution:

Mean = E(X) = ∑xi pi

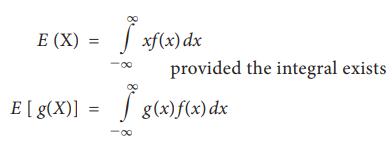

Expectation of a continuous random variable

Let X be a continuous

random variable with probability density function f (x) then the mathematical expectation of X is defined as

Results:

E(c) = c where c is constant

Example 9.22

The

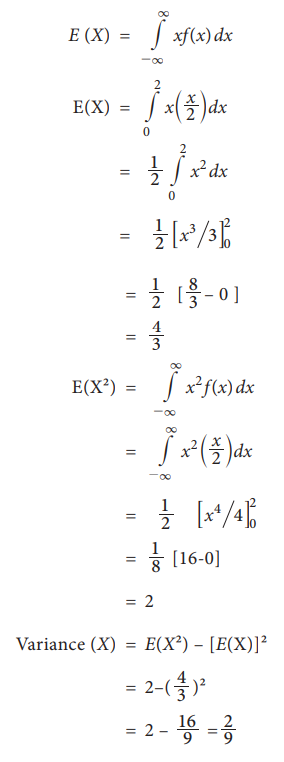

p.d.f. of a continuous random variable X is given by

find its mean and variance

Solution:

So

far we have studied how to find mean and variance in the case of single random

variables taken at a time but in some cases we need to calculate the

expectation for a linear combination of random variables like aX

+ bY or the product of the random variables cX × dY or

involving more number of random variables. So here we see theorems useful in

such situations.

Independent random variables

Random

variables X and Y are said to be independent if the

joint probability density function of X and Y can be written as the product of

marginal densities of X and Y.

That

is f (x,y)= g(x) h(y)

Here g(x) marginal p.d.f. of X

h(y) marginal p.d.f. of Y

Related Topics