Chapter: Principles of Management : Controlling

Budgetary Control: Definition, Features and Classifiction

BUDGETARY CONTROL

Definition: Budgetary Control is defined as "the establishment of budgets,

relating the responsibilities of

executives to the requirements of a policy, and the continuous comparison of

actual with budgeted results either to secure by individual action the

objective of that policy or to provide a base for its revision.

Salient features:

Objectives: Determining the objectives to be achieved, over the budget period, and

the policy(ies) that might be adopted

for the achievement of these ends.

Activities: Determining the variety of activities that should be undertaken for

achievement of the objectives.

Plans: Drawing up a plan or a scheme of operation in respect of each class of

activity, in physical a well as

monetary terms for the full budget period and its parts.

Performance Evaluation: Laying out a system of comparison of actual

performance by each person section

or department with the relevant budget and determination of causes for the

discrepancies, if any.

Control Action: Ensuring that when the plans are not achieved,

corrective actions are taken; and

when corrective actions are not possible, ensuring that the plans are revised

and objective achieved

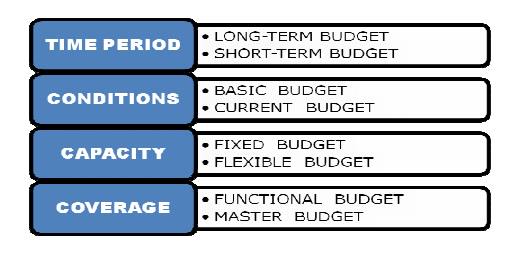

CLASSIFICATION OF BUDGETS

Budgets may be classified on the following bases –

BASED

ON TIME PERIOD:

Long Term Budget

Budgets which are prepared for periods longer

than a year are called LongTerm Budgets. Such Budgets are helpful in business

forecasting and forward planning. Eg: Capital Expenditure Budget and R&D

Budget.

Short Term Budget

Budgets which are prepared for periods less than

a year are known as ShortTerm Budgets. Such Budgets are prepared in cases where

a specific action has to be immediately taken to bring any variation under

control.

Eg: Cash Budget.

BASED

ON CONDITION:

Basic Budget

A Budget, which remains unaltered over a long

period of time, is called Basic Budget.

Current Budget

A Budget, which is established for use over a

short period of time and is related to the current conditions, is called

Current Budget.

BASED

ON CAPACITY:

Fixed Budget

It is a Budget designed to remain unchanged

irrespective of the level of activity actually attained. It operates on one

level of activity and less than one set of conditions. It assumes that there

will be no change in the prevailing conditions, which is unrealistic.

Flexible Budget

It is a Budget, which by recognizing the

difference between fixed, semi variable and variable costs is designed to

change in relation to level of activity attained. It consists of various

budgets for different levels of activity

BASED

ON COVERAGE:

Functional Budget

Budgets, which relate to the individual

functions in an organization, are known as Functional Budgets, e.g. purchase

Budget, Sales Budget, Production Budget, plant Utilization Budget and Cash

Budget.

Master Budget

It is a consolidated summary of the various

functional budgets. It serves as the basis upon which budgeted Profit &

Loss Account and forecasted Balance Sheet are built up.

Related Topics