Gross Domestic Product and its Growth: an Introduction | Economics | Social Science - Write in detail answer | 10th Social Science : Economics : Chapter 1 : Gross Domestic Product and its Growth: an Introduction

Chapter: 10th Social Science : Economics : Chapter 1 : Gross Domestic Product and its Growth: an Introduction

Write in detail answer

V. Write in detail answer

1. Briefly

explain various terms associated with measuring of national income.

Gross National

Product (GNP): Gross National Product is the total

value of goods and services produced and income received in a year by domestic

residents of a country. It includes profits earned from capital invested

abroad.

Gross Domestic

Product (GDP): Gross Domestic Product (GDP) is the

total value of output of goods and services produced by the factors of

production within the geographical boundaries of the country.

Net National Product

(NNP): Net-National Product (NNP) is arrived by making

some adjustment with regard to depreciation. We arrive at the Net National

Product (NNP) by deducting the value of depreciation from Gross National

Product.

(NNP = GNP – Depreciation)

Net Domestic Product

(NDP): Net Domestic Product (NDP) is a part of Gross

Domestic Product. Net Domestic Product is obtained from the Gross Domestic

Product by deducting the quantum of tear and wear expenses (depreciation)

(NDP = GDP – Depreciation)

Per Capita Income

(PCI):

• Per capita Income is an indicator to show the living standard

of people in a country. It is obtained by dividing the National Income by the

population of a country.

• Per capita Income = National Income / Population

Personal Income

(PI): Personal income is the total money income

received by individuals and households of a country from all possible sources

before direct taxes.

Disposable Income

(DI): Disposable income means actual income which can

be spent on consumption by individuals and families. DPI = PI - Direct Taxes

2. What

are the methods of calculating Gross Domestic Product? and explain its.

Expenditure

Approach: In this method, the GDP is measured by adding

the expenditure on all the final goods and services produced in the country

during a specified period.

Y = C + I + G + (X-M)

The Income

Approach: This method looks at GDP from the perspective

of the earnings of the men and women who are involved in producing the goods

and services. The income approach to measure GDP (Y) is Y = Wages + rent + interest

+ profit

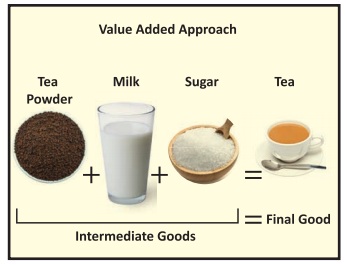

Value Added

Approach: Take a cup of tea. It is the final goods. The

goods used to produce it, tea powder, milk and sugar are intermediate goods. To

measure the market value of the cup of tea is to add the value of each

intermediate goods used in the production of it. The sum of the value added by

all the intermediate goods used in the production gives us the total value of

the final goods produced in the economy.

Example:

Value Added method: Tea powder + Milk + Sugar = Tea

Value of inter mediate goods =

Value of final goods

3. Write

about the composition of GDP in India.

Indian economy is broadly divided into three sectors.

Primary Sector:

(Agricultural Sector)

• Agricultural sector is known as primary sector, in which

agricultural operations are undertaken.

• Agriculture based allied activities, production of raw

materials such as cattle farm, fishing, mining, forestry, corn, coal etc. are

also undertaken.

Secondary Sector:

(Industrial Sector)

• Industrial sector is the secondary sector in which the goods

and commodities are produced by transforming the raw materials.

• Important industries

are Iron and Steel industry, cotton textile, jute, sugar, cement, paper,

petrochemical, automobile and other small scale industries.

Tertiary Sector:

(Service Sector)

• Tertiary sector is known as service sector.

• It includes scientific research, transport, communication,

trade, postal and telegraph, banking, education, entertainment, healthcare and

information technology etc.

• In the 20th century, economists began to suggest that,

traditional tertiary services could be further distinguished from 'quaternary'

and 'quinary' service sectors.

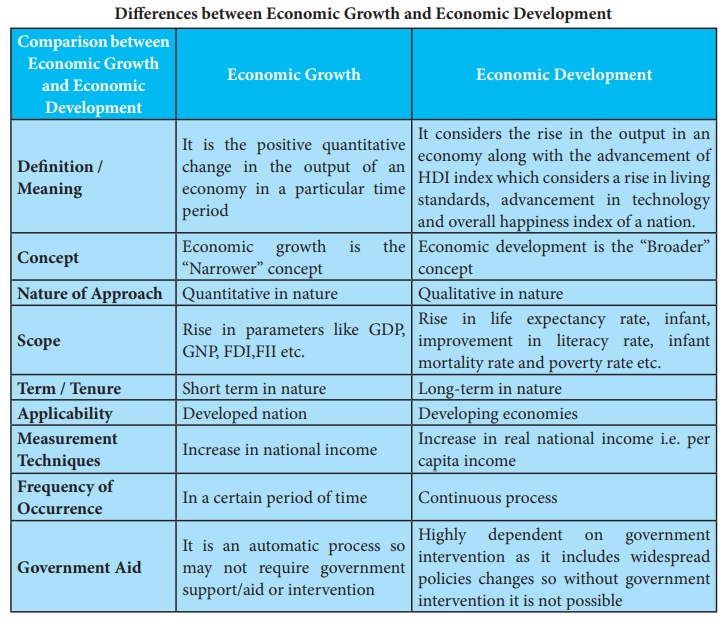

4. Write any five differences

between the growth and development.

Economic Growth

Definition / Meaning : It is the positive quantitative change in the output of an economy in a particular time period

Concept : Economic growth is the “Narrower” concept

Nature of Approach : Quantitative in nature

Scope : Rise in parameters like GDP, GNP, FDI,FII etc.

Term / Tenure : Short term in nature

Applicability : Developed nation

Measurement Techniques : Increase in national income

Frequency of Occurrence : In a certain period of time

Government Aid : It is an automatic process so may not require government support/aid or intervention

Economic Development

Definition / Meaning : It considers the rise in the output in an economy along with the advancement of HDI index which considers a rise in living standards, advancement in technology and overall happiness index of a nation.

Concept : Economic development is the “Broader” concept

Nature of Approach : Qualitative in nature

Scope : Rise in life expectancy rate, infant, improvement in literacy rate, infant mortality rate and poverty rate etc.

Term / Tenure : Long-term in nature

Applicability : Developing economies

Measurement Techniques : Increase in real national income i.e. per capita income

Frequency of Occurrence : Continuous process

Government Aid : Highly dependent on government intervention as it includes widespread policies changes so without government intervention it is not possible

5. Explain the following the

economic policies

i. Agricultural Policy

ii. Industrial policy

iii. New ecnomic policy

Agricultural

policy:

• Agricultural policy is the set of government decisions and

actions relating to domestic agriculture and imports of foreign agricultural

products.

• Some over arching themes include risk management and

adjustment, economic stability, natural resources and environmental

sustainability, research and development and market access for domestic

commodities.

• Price policy, land reform policy, irrigation policy and food

policy are examples of Agricultural policy.

Industrial policy:

• Industrial development creates employment, promotes research

and development, leads to modernization and makes the economy self sufficient.

• Industrial development also boosts agricultural sector, the

service sector and also trade.

• Textile industry policy, Sugar industry policy, Small scale

industrial policy and Industrial labour policy are some of the industrial

policies.

New economic

policy:

• The economy of India had undergone policy shifts in the

beginning of the 1990s.

• This new model economic reform is known as the LPG or

Liberalisation, Privatisation and Globalisation.

• These economic reforms had influenced the overall economic

growth of the country in a significant manner.

VI. Activity and Project

1. Students are collect the Gross Domestic Product datas of Tamilnadu and compare the other state of Karnataka and Kerala’s GDP.

2. Students

are collect the details of Employment growth of Tamilnadu.

Related Topics