Meaning, Auditor's Duty - Auditing - Verification of Contingent Liabilities | 12th Auditing : Chapter 6 : Verification of Liabilities

Chapter: 12th Auditing : Chapter 6 : Verification of Liabilities

Verification of Contingent Liabilities

Verification of Contingent Liabilities

Meaning

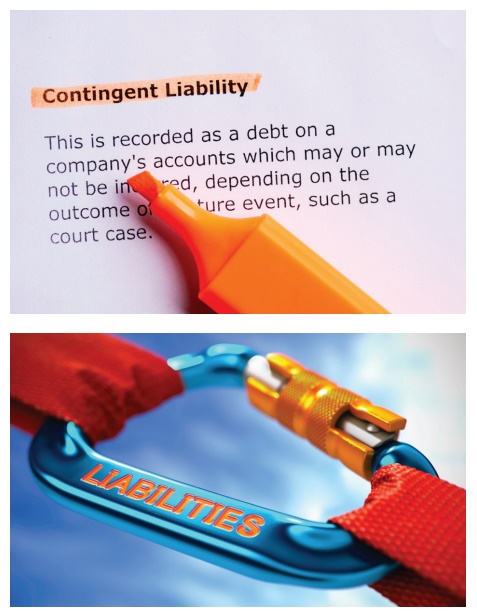

Contingent

liabilities are those liabilities, which may or may not arise in the future for

payment. The auditor should ensure that all known and unknown liabilities

The following

are the examples

of Contingent Liabilities:

·

Liabilities on Bills Receivable discounted and

not matured.

·

Liability on account of partly paid calls.

·

Liability on arrears of dividend on Cumulative

Preference Shares.

·

Liability under a guarantee.

·

Liability for penalties under forward contracts

·

Liability that arises on account of litigation

in respect of labour suits, trademarks, copyrights etc.

Auditor's Duty in Verifying Contingent Liabilities

1. Ensure Creation of Adequate Provision:

The

auditor should ensure that proper provision has been made for certain

liabilities, for example, liability which arise on account of litigation and if

he is not satisfied, the fact should be stated in the report.

2. Disclosure in Balance Sheet:

In

respect of certain liabilities for which no provision has been made in the

books, for example, Bills Receivable which has been discounted, arrears of

accumulated fixed dividend etc. The auditor should verify that such liabilities

are disclosed as foot note in the Balance Sheet.

Related Topics