Chapter: Communication Theory : Random Process

Stationary Process

STATIONARY PROCESS:

In

mathematics and statistics, a stationary process is a stochastic process whose

joint probability distribution does not change when shifted in time.

Consequently, parameters such as the mean and variance, if they are present,

also do not change over time and do not follow any trends.

Stationary

is used as a tool in time series analysis, where the raw data is often

transformed to become stationary; for example, economic data are often seasonal

and/or dependent on a non-stationary price level. An important type of

non-stationary process that does not include a trend-like behaviour is the

cyclostationary process.

Note that

a "stationary process" is not the same thing as a "process with

a stationary distribution". Indeed there are further possibilities for

confusion with the use of "stationary" in the context of stochastic

processes; for example a "time-homogeneous" Markov chain is sometimes

said to have "stationary transition probabilities". Besides, all

stationary Markov random processes are time-homogeneous.

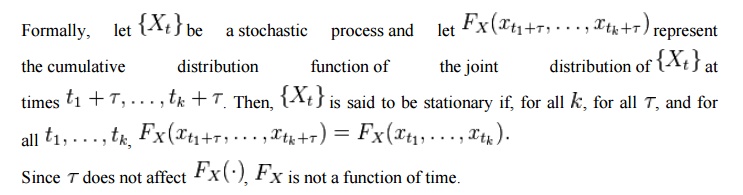

ü Definition:

ü Wide Sense Stationary:

Weaker

form of stationary commonly employed in signal processing is known as

weak-sense stationary, wide-sense stationary (WSS), covariance stationary, or

second-order stationary. WSS random processes only require that 1st moment and

covariance do not vary with respect to time. Any strictly stationary process

which has a mean and a covariance is also WSS.

So, a

continuous-time random process x(t) which is WSS has the following restrictions

on its mean function.

and auto

covariance function.

Related Topics