Chapter: Communication Theory : Random Process

Covariance Functions

COVARIANCE FUNCTIONS:

In

probability theory and statistics, covariance is a measure of how much two

variables change together, and the covariance function, or kernel, describes

the spatial covariance of a random variable process or field. For a random

field or stochastic process Z(x) on a domain D, a covariance function C(x, y)

gives the covariance of the values of the random field at the two locations x

and y:

The same

C(x, y) is called the auto covariance function in two instances: in time series

(to denote exactly the same concept except that x and y refer to locations in

time rather than in space), and in multivariate random fields (to refer to the

covariance of a variable with itself, as opposed to the cross covariance

between two different variables at different locations, Cov(Z(x1), Y(x2)))

ü Mean & Variance of covariance

functions:

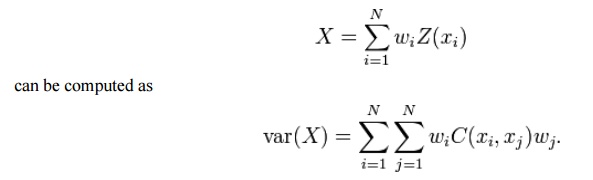

For locations x1, x2, …, xN ∈ D the variance of every linear combination

A

function is a valid covariance function if and only if this variance is

non-negative for all possible choices of N and weights w1, …, wN. A function

with this property is called positive definite.

Related Topics