Retirement and Death of a Partner | Accountancy - Revaluation of assets and liabilities | 12th Accountancy : Chapter 6 : Retirement and Death of a Partner

Chapter: 12th Accountancy : Chapter 6 : Retirement and Death of a Partner

Revaluation of assets and liabilities

Revaluation

of assets and liabilities

When a partner retires

from the partnership firm, the assets and liabilities are revalued as the

current value may differ from the book value. There are two ways in which the

revaluation of assets and liabilities may be dealt with in the accounts.

a) Revised value of assets

and liabilities are shown in the books

b) Revised value of assets

and liabilities are not shown in the books

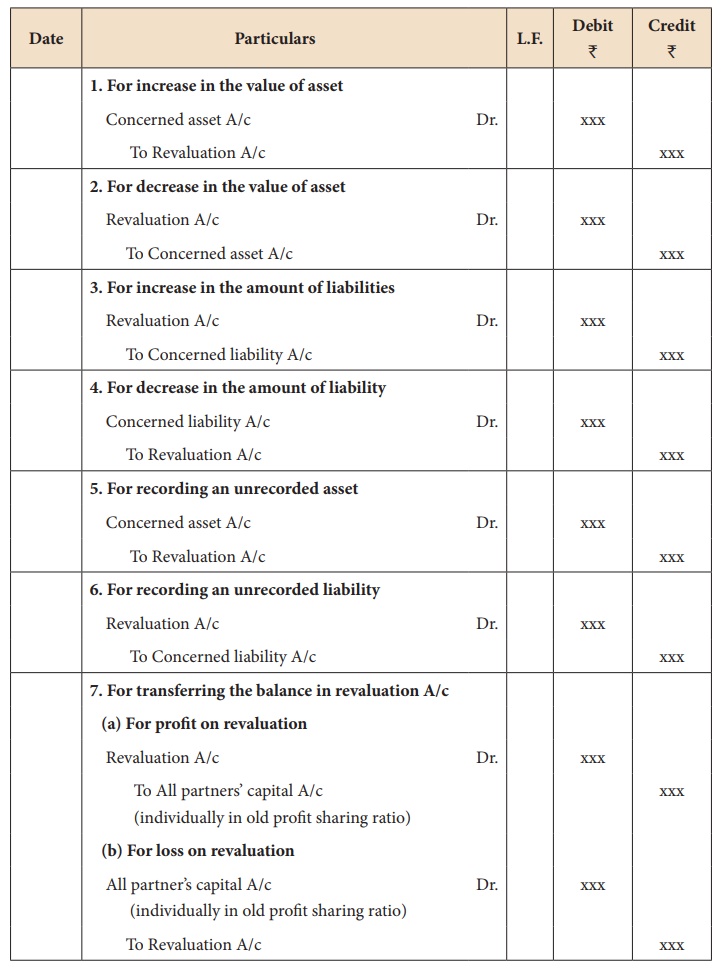

(a) When revised value of assets and liabilities are shown in the books:

Under this method, the

assets and liabilities are shown at their revised values in the books and in

the balance sheet which is prepared immediately after the retirement of a

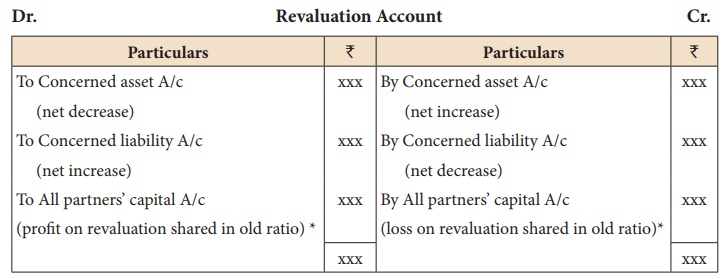

partner. A revaluation account is opened to record the increase or decrease in

the value of assets and liabilities. Revaluation account which is otherwise

called profit and loss adjustment account is a nominal account. Revaluation

account is credited with increase in value of assets and decrease in the value

of liabilities. It is debited with decrease in value of assets and increase in

the value of liabilities. Unrecorded assets if any are credited and unrecorded

liabilities if any are debited to the revaluation account. The profit or loss

arising therefrom is transferred to the capital accounts of all the partners in

the old profit sharing ratio.

Following are the

journal entries to be passed to record the revaluation of assets and

liabilities:

*There will be either profit or loss on revaluation.

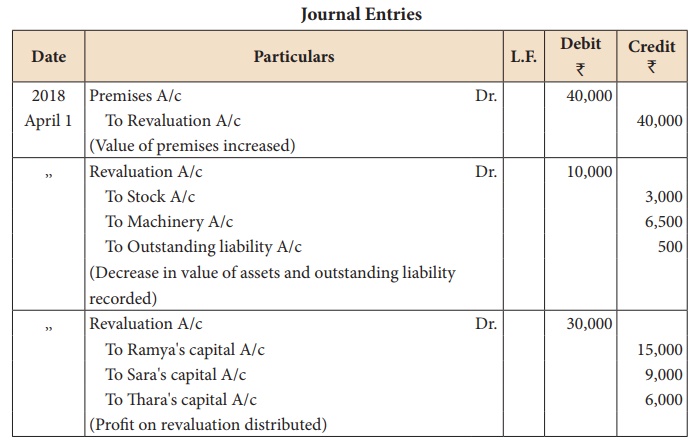

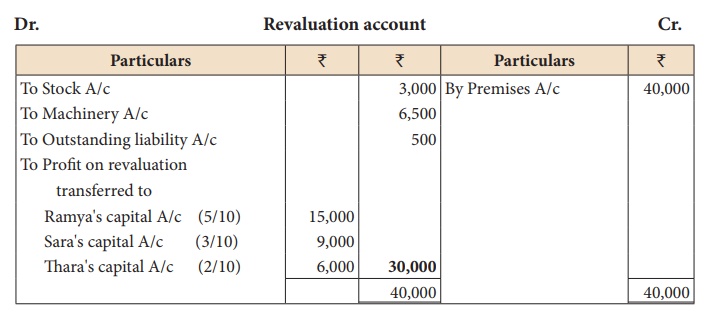

Illustration 4

Ramya, Sara and Thara

are partners sharing profits and losses in the ratio of 5:3:2.

On 1st April 2018, Thara

retires and on retirement, the following adjustments are agreed upon:

(i) Increase the value

of premises by â‚ą

40,000.

(ii) Depreciate stock by

â‚ą 3,000 and machinery by â‚ą 6,500.

(iii) Provide an

outstanding liability of â‚ą

500

Pass journal entries and

prepare revaluation account.

Solution

Illustration 5

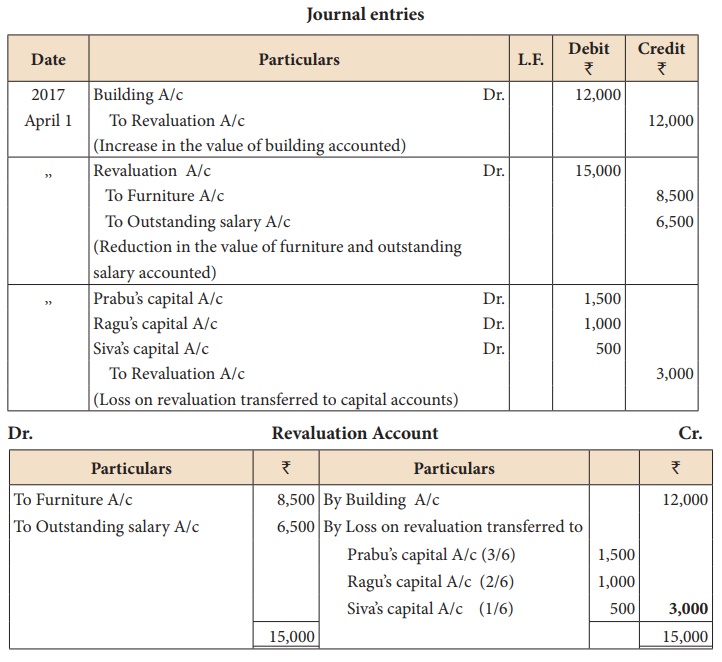

Prabu, Ragu and Siva are

partners sharing profits and losses in the ratio of 3:2:1. Prabu retires from

partnership on 1st April 2017. The following adjustments are to be made:

(i) Increase the value

of building by â‚ą

12,000

(ii) Reduce the value of

furniture by â‚ą 8,500

(iii) A provision would

also be made for outstanding salary for â‚ą

6,500. Give journal entries and prepare revaluation account.

Illustration 6

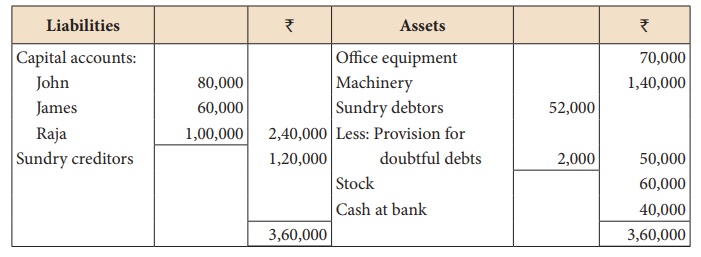

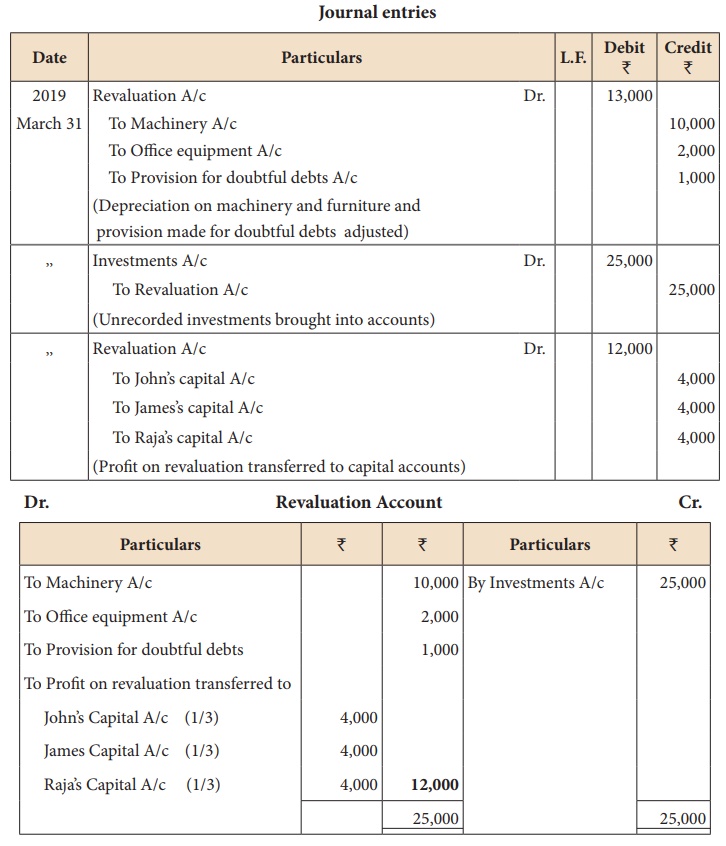

John, James and Raja are

partners in a firm sharing profits and losses equally. Their balance sheet as

on 31st March, 2019 is as follows:

Raja retired on 31st

March, 2019 subject to the following conditions:

(1) Machinery is valued

at â‚ą 1,30,000

(ii) Value of office

equipment is brought down by â‚ą

2,000

(iii) Provision for

doubtful debts should be increased to â‚ą

3,000

(iv) Investment of â‚ą 25,000 not recorded in

the books is to be recorded now

Pass necessary journal

entries and prepare revaluation account.

Solution

(b) When revised values of assets and liabilities are not shown in the books:

Under this method, the

assets and liabilities are shown at their original values and not at the

revised values in the books and in the balance sheet which is prepared

immediately after the retirement of a partner. The net result of revaluation is

adjusted through the capital accounts of the partners. A Memorandum revaluation

account which is a temporary account is opened when the revised values are not

to be shown in the books of accounts.

Related Topics