Retirement and Death of a Partner | Accountancy - Adjustment for current yearŌĆÖs profit or loss upto the date of retirement | 12th Accountancy : Chapter 6 : Retirement and Death of a Partner

Chapter: 12th Accountancy : Chapter 6 : Retirement and Death of a Partner

Adjustment for current yearŌĆÖs profit or loss upto the date of retirement

Adjustment

for current yearŌĆÖs profit or loss upto the date of retirement

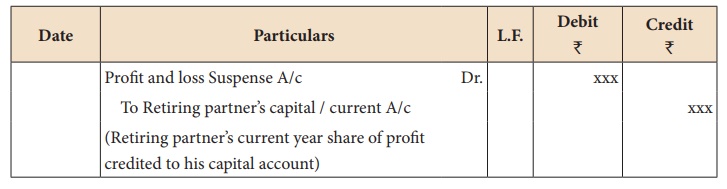

When a partner retires

in between in an accounting year, his share of the current yearŌĆÖs profit or

loss upto the date of retirement has to be distributed to him. It may be

estimated based on the current yearŌĆÖs turnover. Previous yearŌĆÖs profit or the

average of the past yearsŌĆÖ profit may also be taken as the base to estimate the

current yearŌĆÖs profit. The following journal entry is passed.

Note: If there is loss the reverse entry is passed.

Profit and loss suspense account is

closed by transferring to the profit and loss account at the end the accounting

period.

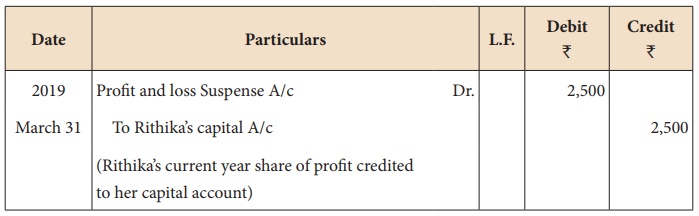

Illustration 14

Justina, Navi and

Rithika are partners sharing profits and losses equally. On 31.3.2019, Rithika

retired from the partnership firm. Profits of the preceding years is as

follows:

2016: Ōé╣ 5,000; 2017: Ōé╣ 10,000 and 2018: Ōé╣ 30,000

Find out the share of

profit of Ritika for the year 2019 till the date of retirement if

a)

Profit is to be distributed on the basis of the previous yearŌĆÖs

profit

b)

Profit is to be distributed on the basis of the average profit of

the past 3 years

Also pass necessary

journal entries by assuming that partnersŌĆÖ capitals are fluctuating.

Solution

(a) If profit is to be distributed on the basis of the previous yearŌĆÖs profit:

RitikaŌĆÖs share of profit for 3 months = 30,000 ├Ś 3/12 ├Ś 1/3 = Ōé╣ 2,500

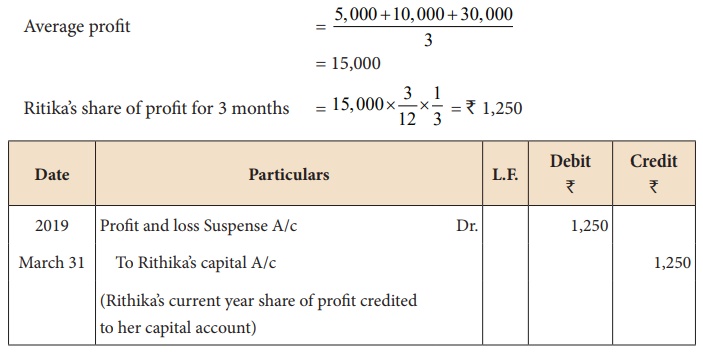

(b) If profit is to be distributed on the basis of the average profit of the past 3 years:

Related Topics