Chapter: 12th Commerce : Chapter 28 : Company Law and Secretarial Practice : Company Secretary

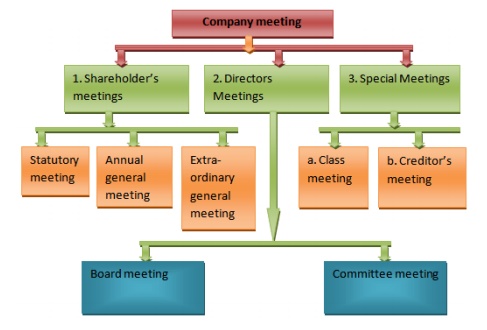

Kinds of Company Meetings

Kinds of Company Meetings

Under the Companies Act, 2013,

Company meetings can be classified as under:

1. Meetings of Shareholders:

(a) Statutory Meeting

(b) Annual General Meetings (AGM)

(c) Extraordinary General Meetings (EGM)

2. Meetings of the Directors

(a) Board meetings

(b) Committees meetings

3. Special Meetings

(a) Class Meetings.

(b) Creditors and of Debenture/bond holders

meetings

The following picture shows the different types of

company meetings

01. Shareholders Meetings

The meeting held with the shareholders of the

company is called shareholders meeting. The shareholders meeting can be

classified as statutory meeting, annual general meeting and extra ordinary

general meeting

a) Statutory Meeting

According to Companies Act, every public company,

should hold a meeting of the shareholders within 6 months but not earlier than

one month from the date of commencement of business of the company. This is the

first general meeting of the public company is called the Statutory Meeting.

This meeting is conducted only once in the lifetime

of the company. A private company or a public company having no share capital

need not conduct a statutory meeting. The company gives the circular to

shareholders before 21 days of the meeting.

b) Annual General Meeting [AGM]

Every year a meeting is held to transact the

ordinary business of the company. Such meeting is called Annual General Meeting

of the company (AGM). Company is bound to invite the first general meeting

within eighteen months from the date of its registration. Then the general

meeting will be held once in every year. The differences between two general

meetings should not be more than fifteen months. Every Annual General meeting shall

be held during business hours, on a day which is not a public holiday, at the Registered Office of the

company or at some other place within the town or village where the Registered

Office is situated. AGM should be conducted by both private and public Ltd

companies.

c) Extra-Ordinary General Meeting

Both Statutory meeting and annual general meetings

are called as ordinary meetings of a company. All other general meetings other

than statutory and annual general meetings are called extraordinary general

meetings. If any meeting conducted in between two annual general meeting to

deal with some urgent or special or extraordinary nature of business is called

as extra-ordinary general meetings.

02. Meeting of the Directors

Since the administration of the company lies in the

hands of the board of directors, they should meet frequently for the proper

conduct of the business and to decide policy matters of the company.

a) Board Meetings

Meetings of directors are called Board Meetings.

Meetings of the directors provide a platform to discuss the business and take

formal decisions. First meeting of directors should be convened within 30

(Thirty) days from the date of incorporation of the company.

b) Committee Meetings

Every listed company and every other public company

having paid up share capital of ₹10 crore is required to have audit committee.

This committee should meet at least four times in a year. In case of other

companies, the board of directors shall nominate a director to play the role of

audit committee which is functioning as a vigil mechanism.

03. Special Meeting

a) Class Meeting (Meetings of Particular Share or Debenture Holders)

Meetings, which are held by a particular class of

share or debenture holders e.g. preference shareholders or debenture holders is

known as class meeting. The debenture holders of a particular class conduct

these meetings. These meetings are held according to the rules and regulations

laid by the Trust Deed or Debenture Bond, from time to time, where the

interests of the debenture holders play vital role at the time of

re-organisation, reconstruction, amalgamation or winding-up of the company.

b) Meetings of the Creditors

Strictly speaking, these are not meetings of a

company. Unlike the meetings of a company, there arise situation in which a

company may wish to arrive at a consensuses with the creditors to avoid any

crisis or to evolve compromise or to introduce any new proposals.

Related Topics