Admission of a Partner | Accountancy - New profit sharing ratio and sacrificing ratio | 12th Accountancy : Chapter 5 : Admission of a Partner

Chapter: 12th Accountancy : Chapter 5 : Admission of a Partner

New profit sharing ratio and sacrificing ratio

New

profit sharing ratio and sacrificing ratio

1. New profit sharing ratio

It is necessary to

determine the new profit sharing ratio at the time of admission of a partner

because the new partner is entitled to share the future profits of the firm.

New profit sharing ratio is the agreed proportion in which future profit will

be distributed to all the partners including the new partner. If the new profit

sharing ratio is not agreed, the partners will share the profits and losses

equally.

2. Sacrificing ratio

The old partners may

sacrifice a portion of the share of profit to the new partner. The sacrifice

may be made by all the partners or some of the partners. Sacrificing ratio is

the proportion of the profit which is sacrificed or foregone by the old

partners in favour of the new partner. The purpose of finding the sacrificing

ratio is to share the goodwill brought in by the new partner. The share

sacrificed is calculated by deducting the new share from the old share.

Share sacrificed = Old

share - New share

Sacrificing ratio =

Ratio of share sacrificed by the old partners

Share of the new partner

is the sum of shares sacrificed by the old partners.

Tutorial note: When the new profit

sharing ratio is not given in the problem, it is to be calculated based on the

information given in the problem.

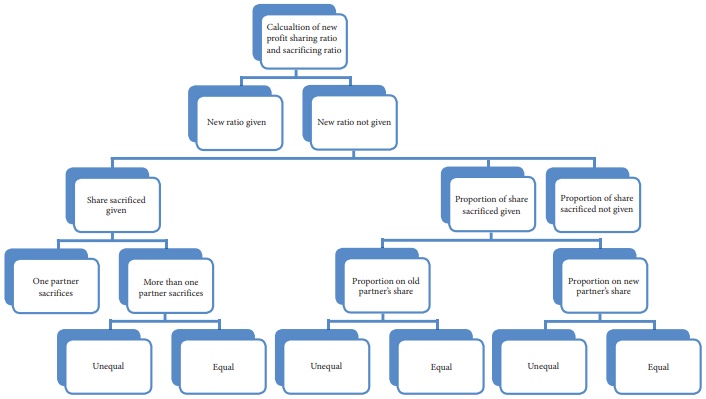

Calculation of sacrificing ratio and new profit sharing ratio under different situations

1. When new profit sharing ratio is given

When new profit sharing ratio is given, sacrificing

ratio has to be calculated as follows:

Sacrificing ratio = Ratio of share sacrificed by

the old partners

Share

sacrificed = Old share - New share

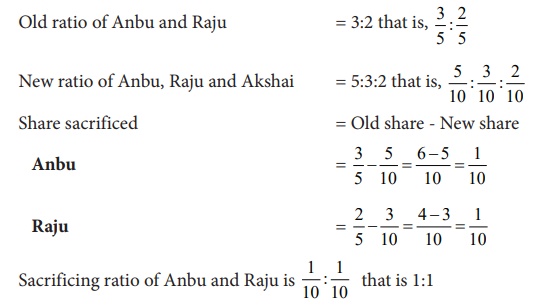

Illustration 8

Anbu and Raju are

partners, sharing profits in the ratio of 3:2. Akshai is admitted as a partner.

The new profit sharing ratio among Anbu, Raju and Akshai is 5:3:2. Find out the

sacrificing ratio.

Solution

2. When new profit sharing ratio is not given

(a) When share sacrificed is given

When new profit sharing

ratio is not given, but the share sacrificed by the old partner(s) is given,

new profit sharing ratio is calculated as follows:

Illustration 9

Hari and Saleem are

partners sharing profits and losses in the ratio of 5:3. They admit Joel for

1/8 share, which he acquires entirely from Hari. Find out the new profit

sharing ratio and sacrificing ratio.

Solution

Computation of

sacrificing ratio and new profit sharing ratio

Share sacrificed by old

partners

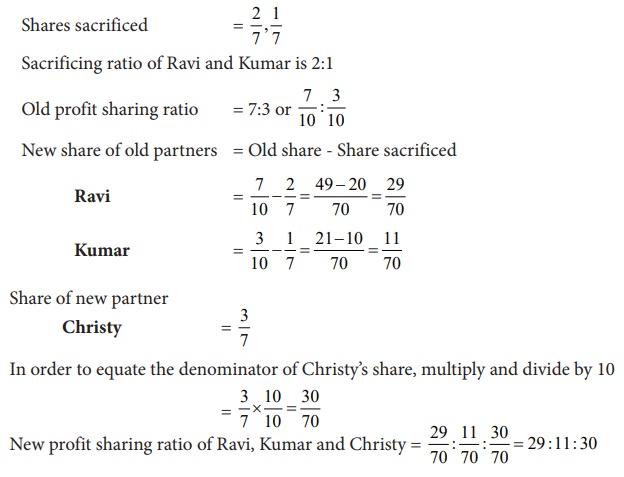

Illustration 10

Ravi and Kumar share

profits and losses in the ratio of 7:3. Christy is admitted as a new partner

with 3/7 share which he acquires 2/7 from Ravi and 1/7 from Kumar. Calculate

the new profit sharing ratio and sacrificing ratio.

Solution

Computation of sacrificing ratio and

new profit sharing ratio

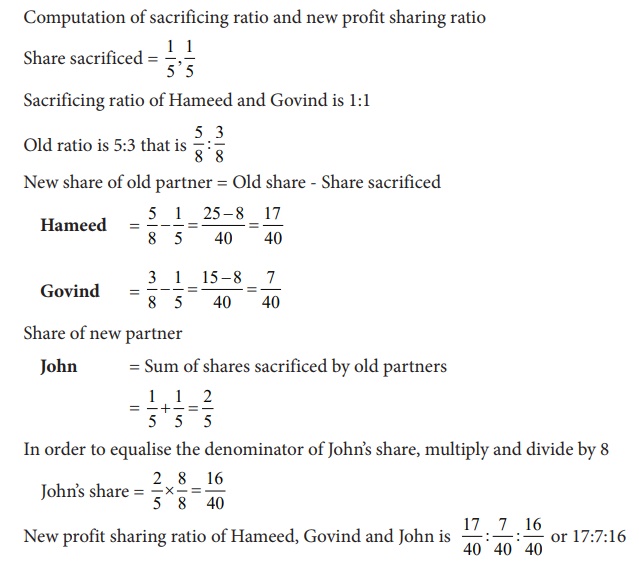

Illustration 11

Hameed and Govind are

partners sharing profits and losses in the ratio of 5:3. They admit John as a

partner. John acquires his share 1/5 from Hameed and 1/5 from Govind. Find out

the new profit sharing ratio and sacrificing ratio.

Solution

Computation of

sacrificing ratio and new profit sharing ratio

(b) When proportion of share sacrificed is given

(i) When share sacrificed is given as a proportion on old partners’ share

When new profit sharing

ratio is not given, but the share sacrificed is given as a proportion on old

partners’ share, new profit sharing ratio is calculated as follows:

Share sacrificed by old partner = Old share x Proportion of share

sacrificed

New share of old partner = Old share - Share sacrificed

Share of new partner = Sum of shares sacrificed by old partners

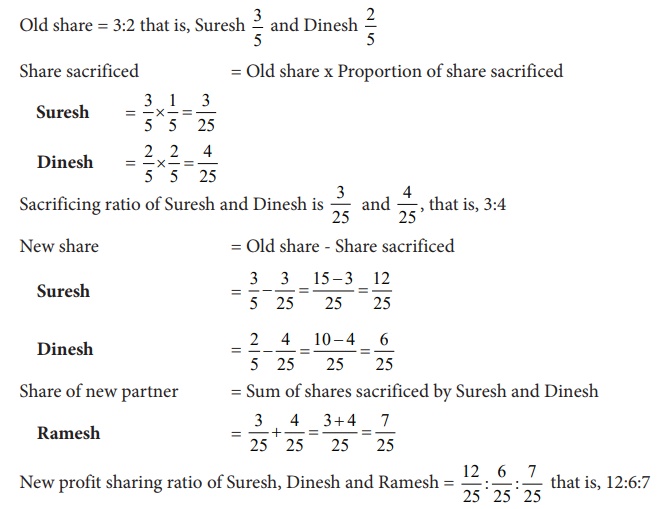

Illustration 12

Suresh and Dinesh are

partners sharing profits in the ratio of 3:2. They admit Ramesh as a new

partner. Suresh surrenders 1/5 of his share in favour of Ramesh. Dinesh

surrenders 2/5 of his share in favour of Ramesh. Calculate the new profit

sharing ratio and sacrificing ratio.

Solution

Computation of

sacrificing ratio and new profit sharing ratio

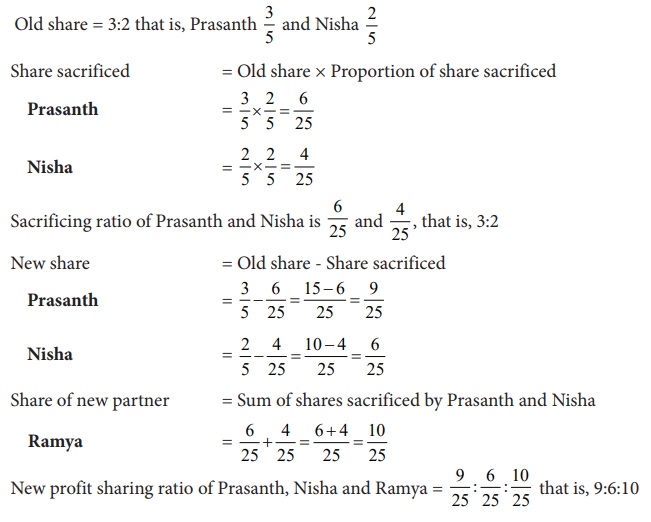

Illustration 13

Prasanth and Nisha are

partners sharing profits and losses in the ratio of 3:2. They admit Ramya as a

new partner. Prasanth surrenders 2/5 of his share and Nisha surrenders 2/5 of

her share in favour of Ramya. Calculate the new profit sharing ratio and

sacrificing ratio.

Solution

Computation of sacrificing ratio and new profit sharing ratio

(ii) When proportion of share sacrificed on new partner’s share is given

When new profit sharing

ratio is not given, but the proportion of share sacrificed on new partner’s

share is given, new profit sharing ratio is calculated as follows:

New share of old

partner = Old share - Share sacrificed

Share sacrificed = New partner’s share × Proportion of share sacrificed

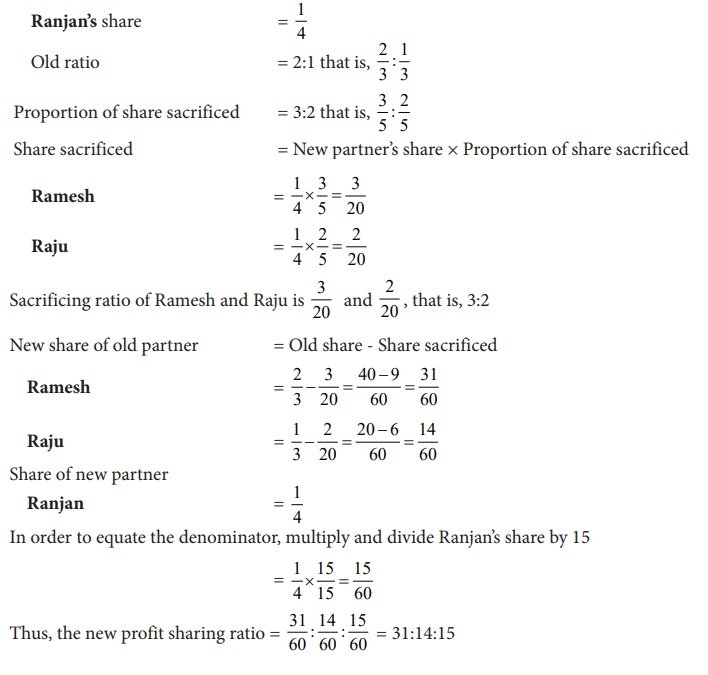

Illustration 14

Ramesh and Raju are

partners sharing profits in the ratio of 2:1. They admit Ranjan into

partnership with 1/4 share of profit. Ranjan acquired the share from old

partners in the ratio of 3:2. Calculate the new profit sharing ratio and

sacrificing ratio.

Solution

Computation of sacrificing ratio and new profit sharing ratio

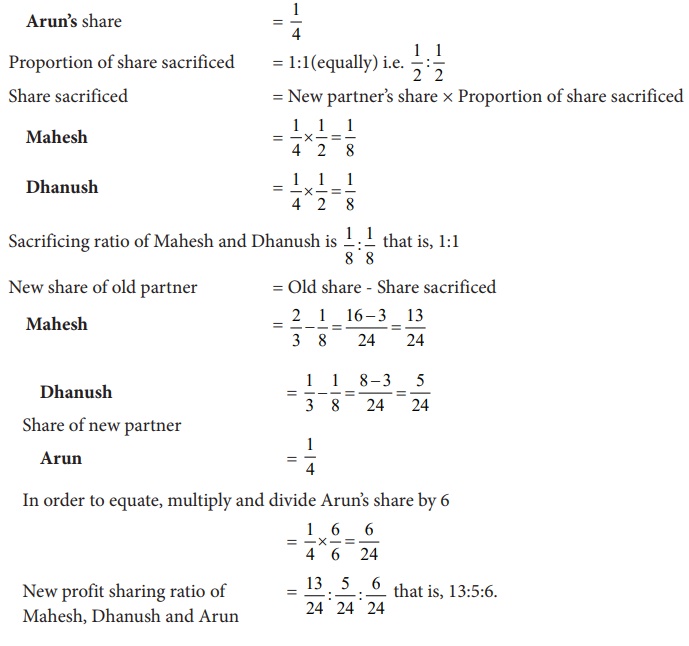

Illustration 15

Mahesh and Dhanush are

partners sharing profits and losses in the ratio of 2:1. Arun is admitted for

1/4 share which he acquired equally from both Mahesh and Dhanush. Calculate the

new profit sharing ratio and sacrificing ratio.

Solution

Computation of sacrificing ratio and new profit sharing ratio

(c) When share sacrificed and proportion of share sacrificed is not given

When new profit sharing

ratio, share sacrificed and the proportion of share sacrificed is not given,

but only the share of new partner is given, new profit sharing ratio is

calculated by assuming that the share sacrificed is the proportion of old

share. New profit sharing ratio is calculated as follows:

Share sacrificed = New

partner’s share x Old share

New share of old partner = Old share - Share sacrificed

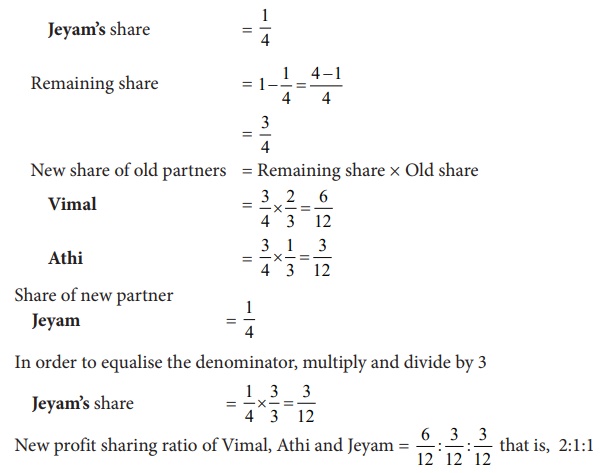

Illustration 16

Vimal and Athi are

partners sharing profits in the ratio of 2:1. Jeyam is admitted for 1/4 share

in the profits. Calculate the new profit sharing ratio and sacrificing ratio.

Solution

Computation of sacrificing

ratio and new profit sharing ratio

Since share sacrificed,

proportion of share sacrificed and new profit sharing ratio are not given, it

is assumed that the existing partners sacrifice in their old profit sharing

ratio, that is, 2:1.

Sacrificing ratio of

Vimal and Athi is 2:1

Let the total share be 1

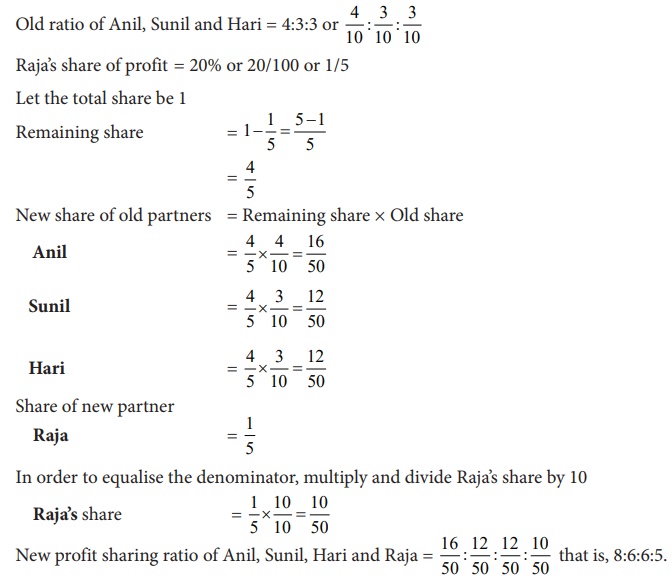

Illustration 17

Anil, Sunil and Hari are

partners in a firm sharing profits in the ratio of 4:3:3. They admit Raja for

20% profit. Calculate the new profit sharing ratio and sacrificing ratio.

Solution

Computation of sacrificing ratio and new profit sharing ratio

Related Topics