Commerce - Partnership Deed and its Contents | 11th Commerce : Chapter 5 : Hindu Undivided Family and Partnership

Chapter: 11th Commerce : Chapter 5 : Hindu Undivided Family and Partnership

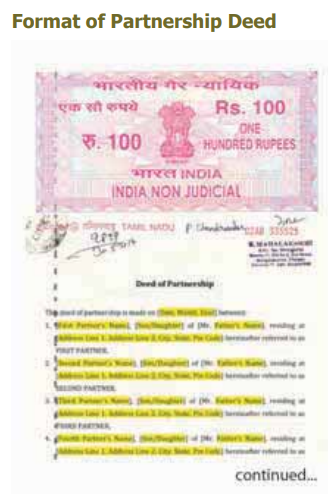

Partnership Deed and its Contents

Partnership Deed and its Contents

Though a partnership agreement need not

necessarily be in writing, it is

important to have a written agreement in order to avoid misunderstandings;

it is

desirable to have a written

agreement. A carefully drafted partnership deed helps in ironing out

differences which may develop among partners and in ensuring smooth running of

the partnership business. It should be properly stamped and registered.

Contents of Partnership Deed

i.

Name of the Firm

ii.

Nature of the proposed business

iii.

Duration of partnership

Duration of the partnership business

whether it is to be run for a fixed period of time or whether

it is to be

dissolved after completing a particular venture.

Iv.

Capital contribution

The capital is to be contributed by the

partners. It must be remembered that capital contribution is not

necessary to become a partner for one who contributes his organising power,

business acumen, managerial skill etc., instead of capital.

v.

Withdrawal from the firm

The amount that can be withdrawn from

the firm by each partner.

vi.

Profit/loss sharing

The ratio in which the profits or losses

are to be shared. If the profit sharing ratio is not specified in the deed, all

the partners must share the profits and bear the losses equally.

vii.

Interest on capital

Whether any interest is to be allowed on

capital and if so, the rate of interest. If the deed is silent on interest on

capital, the rules for interest on capital in partnership act will take effect.

viii.

Rate of interest on drawing

Whether any interest is to be allowed on

drawing, the rate of interest is to be specifird

ix.

Loan from partners

Whether loans can be accepted from the partners and if so the rate of interest

payable thereon.

x.

Account keeping

Maintenance of accounts and audit.

xi.

Salary and Commission to Partners

Amount of salary or commission payable

to partners for their services. (Unless this is specifically provided, no

partner is entitled to any salary).

xii.

Retirement

Matters relating to retirement of a

partner. The arrangement to be made for paying out the amount due to a retired

or deceased partner must also be stated.

xiii.

Goodwill valuation

Method of valuing goodwill on the

admission, death or retirement of a partner.

xiv.

Distribution of responsibility

The work that is entrusted to each

partner is better stated in the deed itself.

xv.

Dissolution procedure

Procedure for dissolution of the firm

and the mode of settlement of accounts thereafter.

xvi.

Arbitration of dispute

Arbitration in case of disputes among

partners. The deed should provide the method for settling disputes or

difference of opinion. This clause will avoid costly litigations.

Related Topics