Vouching of Cash Transactions | Auditing - Internal Check as Regards Stores | 11th Auditing : Chapter 8 : Vouching of Trading Transactions

Chapter: 11th Auditing : Chapter 8 : Vouching of Trading Transactions

Internal Check as Regards Stores

Internal Check as Regards

Stores

Stores is a place were different kinds of

materials, consumables, spare parts are kept under the control of a person

known as a storekeeper. The storekeeper maintains and has control over the

materials kept in stores. He maintains a ledger known as Stores Ledger where he

accounts quantity and value of materials received, issued to production

department and maintains balance of materials left in the stores. Every

organization has to maintain the stores of different kinds of materials like,

finished goods, semi- finished goods and raw materials in a proper way. Stock

of goods kept in the Stores Department should be properly protected against

pilferage, theft or misappropriations. Hence a proper system of internal check

in relation to stores must be given careful attention.

The system of internal check to be introduced in

respect to materials is as follows:

1. Location

of Stores: Stores should be located at a convenient place and should have proper facilities so

that goods may not be misplaced, misused or wasted.

2. Receipt

of Stores: The Stores Department on receiving the goods in stores should prepare a Goods Received

Note in triplicate. One copy of the note should be sent to the Purchase Department,

second copy to the Accounts Department and the third copy will be retained by

the Stores Department. The particulars of the goods received should be entered

in the note.

3. Preservation

of Stores: Stores should

be properly preserved; the following are the points to be noted in this

regard.

·

A separate place should be earmarked for each type

of stores.

·

All items in stores should be serially numbered and

the place where they are to be kept also should be numbered.

·

Entries relating to stores, such as, receipts,

issues and balance of stores should be recorded in the bin cards. Such bin

cards should be kept hanging on the places where stores are reserved.

·

A responsible officier at frequent intervals should

check the stores and should also compare the bin cards with the stores ledger.

·

At regular intervals stocktaking should be

conducted. Differences if any noticed between the actual stock and the balance

of stock as shown by the books should be properly adjusted after obtaining

sanction from the higher officials.

4. Issue of

Stores: The following system should

be adopted for issuing stores:

· Stores

should be issued only against proper requisition slip received from the

department. The requisition slip should be signed by the responsible person of

the department.

·

Issue of stores should be made only by an

authorized person. The Stores officer should be seated near the gate so that

all the issues should be made under his supervision.

·

When materials or stores are returned from the job

or department, it should be properly accounted in the Materials Return Note.

·

When materials or stores are transferred from one

department or job to another entry should be made through the Materials

Transfer Note.

·

Proper instructions should be given to the

gate-keeper not to allow any materials out of the factory without obtaining

permission from the storekeeper.

5. Recording:

When

materials are issued under the

material requisition slip from the department, the requisition slip should be

sent to the stores accounts section for recording. At frequent intervals the

bin cards should be checked and compared with the entries in the stores

records.

Books and Documents to be Vouched: (1) Bin Card, (2) Stores Ledger,

(3) Goods Received Note, (4) Material Requisition Slip, (5) Material Transfer

Note, (6) Material Return Note.

Records to be verified by the Auditor

Auditor should check entries relating

to stores with the following records:

1. Bin Card: Maintained by the

Storeskeeper in Stores Department.

2. Stores Ledger Account: Maintained

by Accountant in Accounts Department.

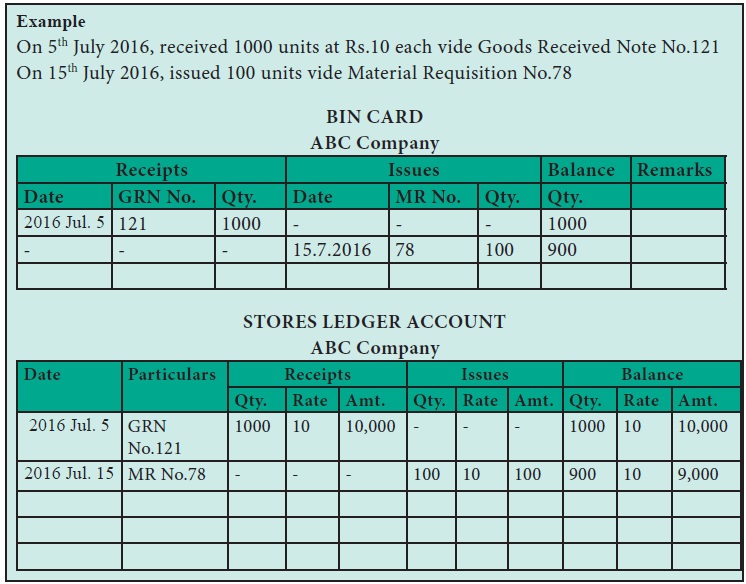

Example

On 5th July 2016, received 1000 units

at Rs.10 each vide Goods Received Note No.121 On 15th July 2016, issued 100

units vide Material Requisition No.78

Related Topics