Vouching of Cash Transactions | Auditing - Goods Sent on Sale or Return Basis | 11th Auditing : Chapter 8 : Vouching of Trading Transactions

Chapter: 11th Auditing : Chapter 8 : Vouching of Trading Transactions

Goods Sent on Sale or Return Basis

Goods Sent on Sale or Return Basis

When goods are delivered to a customer on condition

that if goods are not approved within a particular period the customer can

return the goods. Such a type of sale is called as Goods on sale or return

basis.

Auditors Duty

The auditor should vouch sale on return basis by

considering the following points:

1.

Auditor should verify that a separate sale or

return journal with necessary columns for sale price of goods, value of goods

returned and retained should be maintained.

2. Auditor should

vouch the goods on sale-or-return journal with invoices, correspondences with

the client or other documentary evidences available with the client.

3. The

auditor should ensure that goods sold on approval should not be treated as

complete sale unless the customer approves the sale.

4. He should

check that until the goods are approved it should be shown as goods with

customers in closing stock in Balance Sheet. If this is not done, the profit of

the concern will be inflated and will not show the correct financial position.

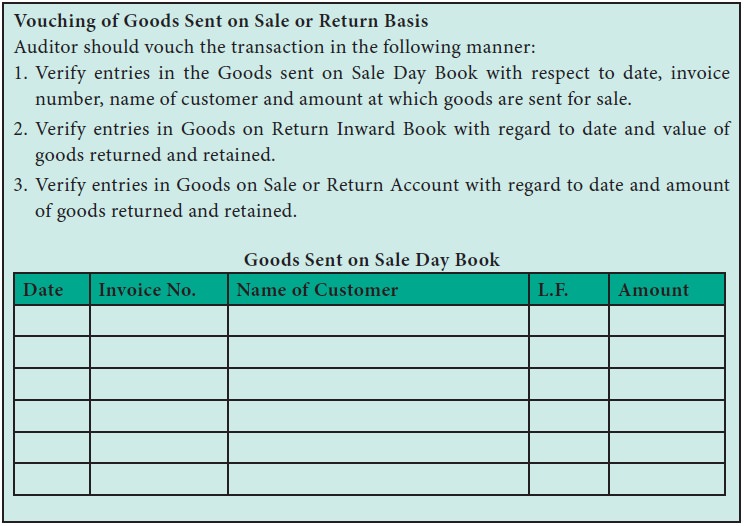

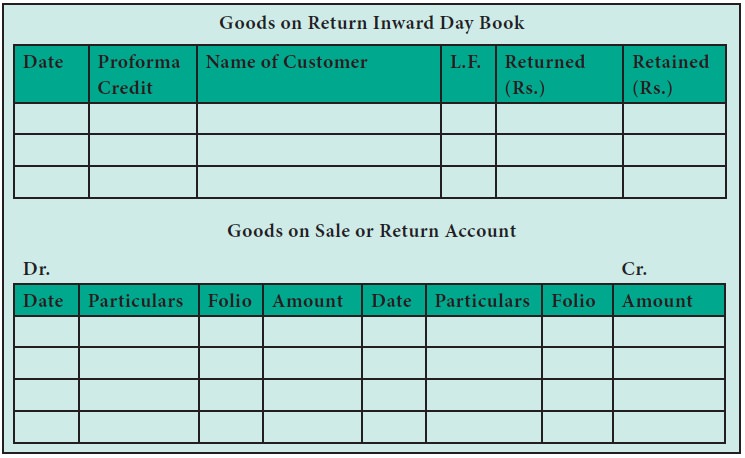

Vouching of Goods Sent on Sale or Return Basis

Auditor should vouch the transaction

in the following manner:

1. Verify entries in the Goods sent

on Sale Day Book with respect to date, invoice number, name of customer and

amount at which goods are sent for sale.

2. Verify entries in Goods on Return

Inward Book with regard to date and value of goods returned and retained.

3. Verify entries in Goods on Sale or

Return Account with regard to date and amount of goods returned and retained.

Related Topics