Chapter: 11th Economics : Chapter 1 : Introduction To Micro-Economics

Economics: Its Methods, Facts, Theories and Laws

Economics:

Its Methods, Facts, Theories and Laws

1. Methods of Economics: Deduction and Induction

Like any

other science, Economics also has its laws or generalisations. These laws

govern the activities in the various divisions of Economics such as

Consumption, Production, Exchange and Distribution. The logical process of

arriving at a law or generalization in a science is called its method.

Economics

uses two methods: deduction and induction.

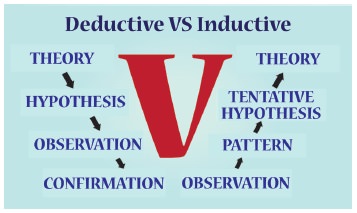

a. Deductive Method of Economic

Analysis

It is

also named as analytical or abstract

method. It consists in deriving conclusions from general truths; it takes few

general principles and applies them to draw conclusions. The classical and

neo-classical school of economists notably, Ricardo, Senior, J S Mill, Malthus,

Marshall, Pigou, applied the deductive method in their economic investigations.

Steps of Deductive Method

Step 1: The analyst must have a clear and

precise idea of the problem to be inquired

into.

Step 2: The analyst clearly defines the

technical terms used in the analysis. Further, assumptions of the theory are to be precise.

Step 3: Deduce hypothesis from the

assumptions taken.

Step 4: Hypotheses should be verified

through direct observation of events in the real world and through statistical methods. (eg) There exists an

inverse relationship between price and quantity demanded of a good.

b. Inductive Method of Economic Analysis

Inductive method, also called empirical method, is adopted by the “Historical School of Economists”. It involves the process of reasoning from

particular facts to general principle.

Economic

generalizations are derived in this method, on the basis of

1.

Experimentations;

2.

Observations; and,

3.

Statistical methods.

Step 1: Data are collected about a

certain economic phenomenon. These are systematically

arranged and the general conclusions are drawn from them.

Step 2: By observing the data,

conclusions are easily drawn.

Step 3: Generalization of the data and

then Hypothesis Formulation

Step 4: Verification of the hypothesis (eg.Engel’s law)

According to Engel’s Law “The proportion

of total expenditure incurred on food items declines as total expenditure

[which is proxy for income] goes on increasing.”

Economists

today are of the view that both these methods are complementary. Alfred Marshall

has rightly remarked: “Inductive and Deductive methods are both needed for scientific thought, as the right and left

foot are both needed for walking”.

2. Economics:

Facts, Theories

Using the

methods, the economist observes facts, such as, changes in the price of a

commodity. Similarly, the quantity demanded of that commodity also varies. And

he observes these movements and comes up with a theory that these two movements

are inversely related, i.e., when the price increases, the quantity demanded of

that commodity decreases and vice versa. Thus, he formulates his theory of

demand.

He tests

his theory by collecting further facts and when his theory stands the test of

time and obtains universal acceptance, the theory is raised to the status of a

law.

3. Nature of Economic Laws

A Law

expresses a causal relation between two or more than two phenomena. Marshall

states that the Economic laws are statement

of tendencies, and those social laws, which relate to those branches of

conduct in which the strength of the motives chiefly concerned can be measured

by money price.

In

natural sciences, a definite result is expected to follow from a particular

cause. In Economic science, the laws function with cause and effect. The

consequences predicted by the data, necessarily and invariably follow.

However,

Economic laws are not as precise and certain as the laws in the physical

sciences. Marshall holds the opinion that there are no laws of economics which

can be compared for precision with the law of gravitation.

Importance of Micro Economics

·

To understand the operation of an

economy

·

To provide tools for economic

policies

·

To examine the condition of economic

welfare

·

Efficient utilization of resources

·

Useful in international trade

·

Useful in decision making:

·

Optimal resource allocation

·

Basis for prediction

·

Price determination

A

physical scientist carrying out controlled experiments in his laboratory can

test the scientific laws very easily by changing the conditions obtaining

there. Changes in Economics science cannot be brought about easily. As a

result, prediction regarding human behaviour is likely to go wrong. There are

exceptions to the Law of Demand. Thus, economic laws are not inviolable.

As

unpredictability is invariably associated with the economic laws. Marshall

compares them to the laws of tides. Just as it cannot be predicted and said

with certainty that a high tide would follow a low tide, unpredictability

prevails in Economics. Human behaviour is volatile. Economic laws are not

assertive but they are indicative. The Law of Demand, for example, states that

other things remaining the same, the quantity demanded of a commodity

increases, as its price decreases and vice versa.

The use

of the assumption ‘other things remaining the same’ (ceteris paribus) in

Economics makes the Economic laws hypothetical. It might be argued that the

laws in other sciences can also be called hypothetical. It should be admitted

however that in the case of Economics, the hypothetical elements in its laws

are a little less pronounced than in the laws of physical sciences.

But since

money is used as the measuring rod, laws in economics are more exact, precise

and accurate than the other social sciences. As the value of the measuring- rod

money is not constant, there is always an hypothetical element surrounding the

laws of Economics.

Some

economic laws are simply truisms. For example, saving is a function of income.

Another

example of truism is: human wants are unlimited.

Related Topics