Chapter: 11th Economics : Chapter 1 : Introduction To Micro-Economics

Basic Concepts in Economics

Basic Concepts in Economics

Like other sciences, Economics also has concepts to explain its theories. A complete and clear grasp of their meaning is necessary when the theories associated with them are studied. Only a preliminary acquaintance is now attempted here.

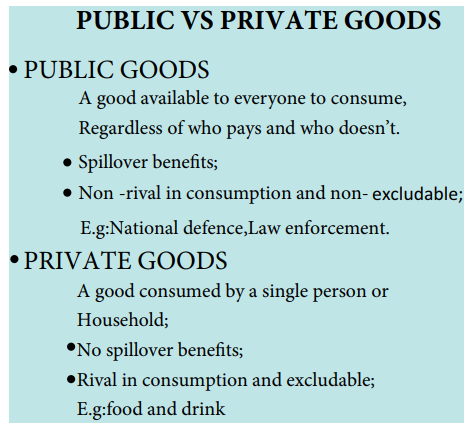

1. Goods and Services

Both goods and services satisfy human wants. In Economics, the term ‘goods’ implies the term ‘services’ also, unless specified otherwise.

Goods (also called ‘products’, ‘commodities’, ‘things’ etc)

a. as material things, they are tangible;

b. have physical dimensions, i.e., their physical attributes can be preserved over time;

c. exist independently of their owner;

d. are owned by some persons;

e. are transferable;

f. have value-in exchange;

Kinds of Goods (and Services)

a. Free and Economic goods

Free goods are available in nature and in abundance. Man does not need to incur any expenditure to own or use them. For example air, and sun shine. Water was also an example in the past, but at present it has exchange value. So it is not a free good.

Milton Friedman, a Nobel laureate, popularises a saying: “There is no such thing as a free lunch”. He means that it is impossible to get something for nothing. Even those offered ‘free’ always costs a person or the society as a whole. Its cost, however, is hidden. It is an externality. Someone can benefit from an externality or from a public good, but someone-else has to pay the cost of producing these benefits. In Economics, it refers to ‘opportunity cost’.

On the other hand, economic goods are not available in plenty. They are scarce in supply. Man has to spend money to own or use them.

b. Consumer goods and Capital goods:

Consumer goods directly satisfy human wants, TV, Furniture, Automobile etc.

Capital-goods (also called producer’s goods) don’t directly satisfy the consumer wants. They help to produce consumer goods. For example, machines do not directly satisfy the consumers, but in factories, the manufacturers need them.

c. Perishable goods and Durable goods:

Perishable goods are short-lived. Their life-span is limited. For example fish, fruits, flower etc do not have a long life.

Durable goods and semi-durable goods have a little longer life-time than the Perishable goods. For example, a table, a chair etc.

Services

Along with goods, services are produced and consumed. They are generally, possess the following:

· Intangible: Intangible things are not physical objects but exist in connection to other things, for example, brand image, goodwill etc. But today, the intangible things are converted and stored into tangible items such as recording a music piece into a pen-drive. They are marketed as a good.

· Heterogeneous: Services vary across regions or cultural backgrounds. They can be grouped on the basis of quality standards. A single type service yields multiple experiences. For example, music, consulting physicians etc.

· Inseparable from their makers: Services are inextricably connected to their makers. For example, labour and labourer are inseparable; and,

· Perishable: Services cannot be stored as inventories like assets. For example, it is useless to possess a ticket for a cricket-match once the match is over. It cannot be stored and it has no value-in-exchange.

2. Utility

a. Meaning

‘Utility’ means ‘usefulness’. In Economics, utility is the want-satisfying power of a commodity or a service. It is in the goods and services for an individual consumer at a particular time and at a particular place.

b. Characteristics of Utility

1. Utility is psychological. It depends on the consumer’s mental attitude. For example, a vegetarian derives no utility from mutton;

2. Utility is not equivalent to usefulness. For example, a smoker derives utility from a cigarette; but, his health gets affected;

3. Utility is not the same as pleasure. A sick person derives utility from taking a medicine, but definitely, it is not providing pleasure;

4. Utility is personal and relative. An individual obtains varied utility from one and the same good in different situations and places;

5. Utility is the function of the intensity of human want. An individual consumer faces a tendency of diminishing utility;

6. Utility is a subjective concept it cannot be measured objectively and it cannot be measured numerically;

7. Utility has no ethical or moral significance. For example, a cook derives utility from a knife using which he cuts some vegetables; and, a killer wants to stab his enemy by that knife. In Economics, a commodity has utility, if it satisfies a human want;

Types of Utility

The following are the types of utility

1. Form Utility: An individual consumer obtains utility from a good or service only when it is available in a particular form. Raw materials in their original form may not possess utility for a consumer. But in their changed forms as they become finished products, they provide utility to him. For example, cotton as a raw material may not possess utility for a consumer; but as it gets a new form as a cloth, it yields the consumer utility.

2. Time Utility: A sick man derives time utility from blood not at the time of its donation, but only at the operation-time, i.e., when it is used.

3. Place Utility: A student derives place utility from a book not at the place of its publication (production centre) but only at the place of his education (consumption centre).

4. Service Utility: An individual consumer derives service utility from a service made available at the time when he most needs it. For example, clients obtain service utility from their lawyers, patients derive service utility from the doctors and so on.

5. Possession Utility: When a student buys a book or dictionary from a book seller, then only it gives utility.

6. Knowledge Utility: It is the utility derived by having knowledge of a particular thing. Advertisement serves as a source of information on an object.

Measurability of Utility

Wants of a person are satisfied by the act of consumption. The consumer derives utility, measured in terms of ‘Utils’. An ‘Util’ is a unit of measurement of utility. An individual pays a price for the unit of the good, equal to the utility derived. Marshall states that utility can be measured indirectly using the ‘measuring rod of money’.

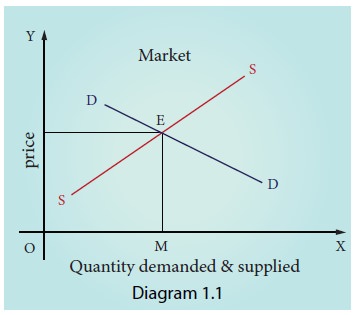

3. Price

Price is the value of the good expressed in terms of money. Price of a good is fixed by the forces of demand for and supply of the good. Price determines what goods are to be produced and in what quantities. It also decides how the goods are to be produced.

4. Market

Generally, market means a place where commodities are bought and sold.

But, in Economics, it represents where buyers and sellers enter into an exchange of goods and services over a price.

5. Cost

Cost refers to the expenses incurred to produce or acquire a given quantum of a good.

Together with revenue, it determines the profit gained or the loss incurred by a firm.

6. Revenue

Revenue is income obtained from the sale of goods and services. Total Revenue (TR) represents the money obtained from the sale of all the units of a good. Thus, TR = P × Q, where TR is Total Revenue; P is the price per unit of the good; and, Q is the Total Quantity of the goods sold.

7. Equilibrium Diagram 1.1.

a. Stable Equilibrium

Prof. Stigler states that “equilibrium is a position from which there is no net tendency to move”. Its absence is referred to as disequilibrium. Consumer’s equilibrium occurs when he gets maximum satisfaction. The equilibrium of the Producer occurs when he gets maximum profit. A resource is in equilibrium when it gets fully employed and gets its maximum payment. Thus, static equilibrium is based on given and constant prices, quantities, income, technology, population etc.

b. Particular Equilibrium and General Equilibrium

An equilibrium, when it pertains to a single variable, may be called particular equilibrium.

An equilibrium, on the other hand, when it relates to numerous variables or even the economy as a whole, may be called general equilibrium.

8. Income

Income represents the amount of monetary or other returns, either earned or unearned small or big, accruing over a period of time to an economic unit. Nominal income refers to income, expressed in terms of money. It is termed as the money income.

Real income is the amount of goods that can be purchased with money as income. It is the purchasing power of income which is based on the rate of inflation.

Related Topics