Accountancy - Three column cash book (Cash book with cash, discount and bank column) | 11th Accountancy : Chapter 7 : Subsidiary Books - II Cash Book

Chapter: 11th Accountancy : Chapter 7 : Subsidiary Books - II Cash Book

Three column cash book (Cash book with cash, discount and bank column)

Three column cash book (Cash book with cash, discount and bank column)

A three column cash book includes three amount columns on both sides, i.e., cash, bank and discount. This cash book is prepared in the same way as simple and double column cash books are prepared. The transactions which increase the cash and bank balance are recorded on the debit side of the cash and bank columns respectively. Opening balance of cash and favourable bank balance appear as the first item on the debit side of the three column cash book in case of existing business. If the business is a new one, capital contributed in cash and/or bank deposit appear as the first item on the debit side.

All the transactions which decrease the cash and bank balance are recorded in the cash and bank columns on the credit side. The balancing figures will be the closing balances of cash and bank. Cash will always have debit balance. Bank balance may be debit or credit depending on whether the balance is favourable or unfavourable respectively. If there is any discount allowed it is entered in the discount column on the debit side against the particular account. Similarly, if there is any discount received, it is entered in the discount column on the credit side.

1. Format

Format of three column cash book is as follows:

Tutorial note

· If a business entity has more than one bank account, columns may be provided in the cash book for each bank account separately.

· Treatment of cheques: In addition to cash dealings every business may use cheques as a means of payment. For the purpose of accounting, cheques received are treated as cash received. When cheques received are banked on the same day the amount is to be directly debited to the bank account. When payments is made by cheque, the bank account is credited.

2. Contra entry

When the two accounts involved in a transaction are cash account and bank account, then both the aspects are entered in cash book itself. As both the debit and credit aspects of a transaction are recorded in the cash book, such entries are called contra entries.

Example

· When cash is paid into bank, it is recorded in the bank column on the debit side and in the cash column on the credit side of the cash book.

· When cash is drawn from bank for office use, it is entered in cash column on the debit side and in the bank column on the credit side of the cash book.

To denote that there are contra entries, the alphabet ‘C’ is written in L.F. column on both sides. Contra means that particular entry is posted on the other side (contra) of the same book, because Cash account and Bank account are there in the cash book only and there are no separate ledger accounts needed for this purpose. The alphabet ‘C’ indicates that no further posting is required and the relevant account is posted on the opposite side.

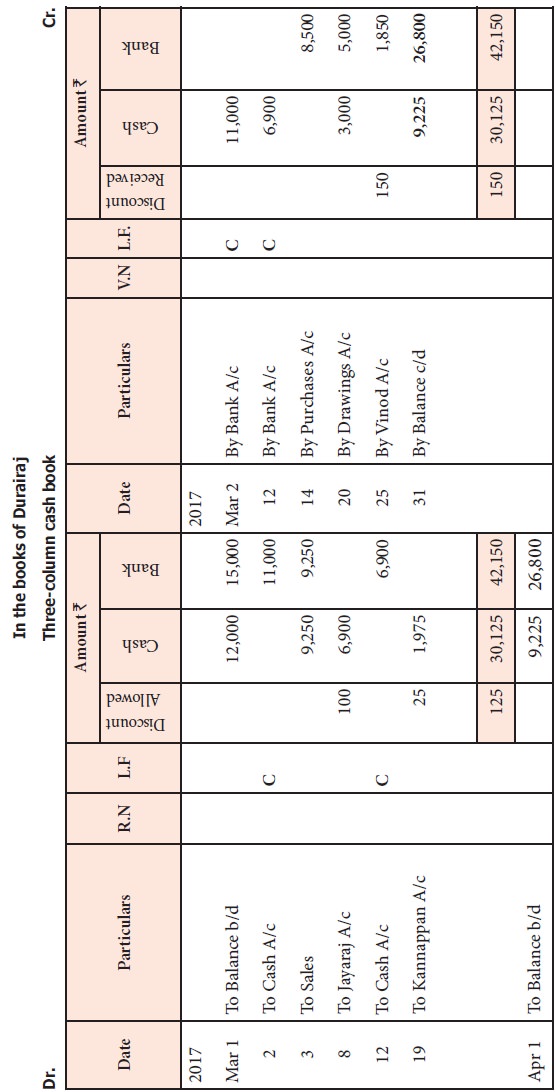

Illustration 4

Prepare three column cash book in the books of Thiru Durairaj.

2017 Rs.

March 1 Cash in hand 12,000

Cash at bank 15,000

2 Cash paid into bank 11,000

3. Goods sold Rs. 18,500. Half of it is received in cash and half of it is received by cheque which is immediately deposited in the bank

4 Sold on credit to Jayaraj for 7,000

8 Jayaraj sent a cheque in full settlement 6,900

12 Jayaraj’s cheque was sent to bank

14 Bought goods from Iqbal and issued a cheque

to him immediately 8,500

15 Bought goods from Murali on credit 4,000

19 Received a cheque from Kannappan in full

settlement of his account of Rs. 2,000 1,975

20 Drew cash Rs. 3,000 and by cheque Rs. 5,000 for personal use

25 Paid Vinod by cheque in full settlement of his account of Rs. 2,000 1,850

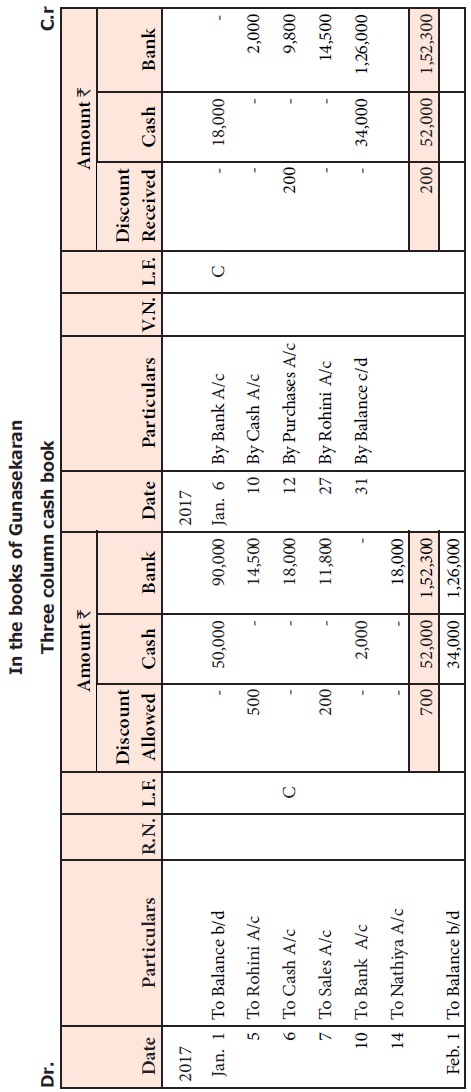

Illustration 5

Record the following transactions in three column cash book of Gunasekaran.

2017

Jan

1 Cash in hand 50,000

1 Cash at bank 90,000

2 Goods sold on credit to Rohini 15,000

5 Cheque received from Rohini in full settlement and deposited into bank 14,500

6 Cash deposited into bank through cash deposit machine 18,000

7 Goods sold to Sridhar for Rs. 12,000. He made the payment of Rs. 11,800 by debit card in full settlement by availing a cash discount of Rs. 200

10 Money withdrawn from bank for office use 2,000

12 Purchased goods from Raja for Rs. 10,000 and paid through credit

card in full settlement by availing a cash discount of Rs. 200 9,800

14 Nathiya who owed money made the payment through NEFT 18,000

Cheque of Rohini dishonoured

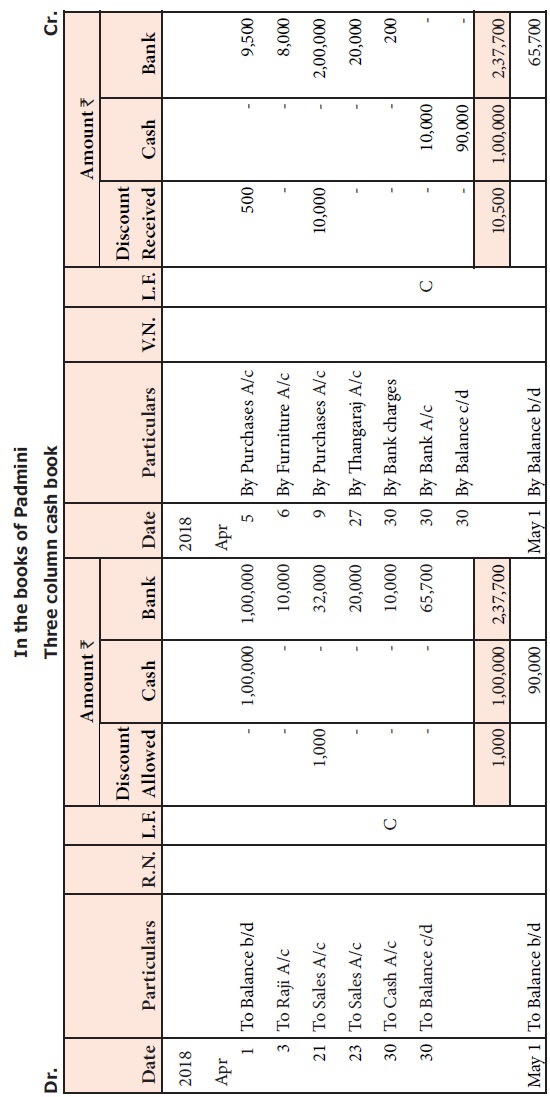

Illustration 6

Padmini is a dealer in stationery. She maintains three column cash book. Record the following transactions in her cash book for the month of April, 2018.

2018

April Rs.

1 Cash in hand: Rs. 1,00,000; Cash at bank: 1,00,000

3 Goods sold to Raji who made the payment through credit card 10,000

5 Goods purchased for Rs. 10,000 from Padma Traders. The payment is made after getting a cash discount of Rs. 500 through net banking 9,500

6 Purchased furniture from ABC Co. and the payment is made by cheque 8,000

9 Purchased goods from TNPL for Rs. 2,10,000 and the payment is made through RTGS after availing a cash discount of Rs. 10,000 2,00,000

21 Supplied stationery items to BHEL for Rs. 33,000 and received the payment through NEFT after allowing a cash discount of for Rs. 1,000 32,000

23 Supplied goods to Thangaraj who made the payment by cheque which is deposited in the bank 20,000

27 Thangaraju’s cheque is dishonoured

30 Bank charged for overdraft facility 200

30 Cash deposited into bank 10,000

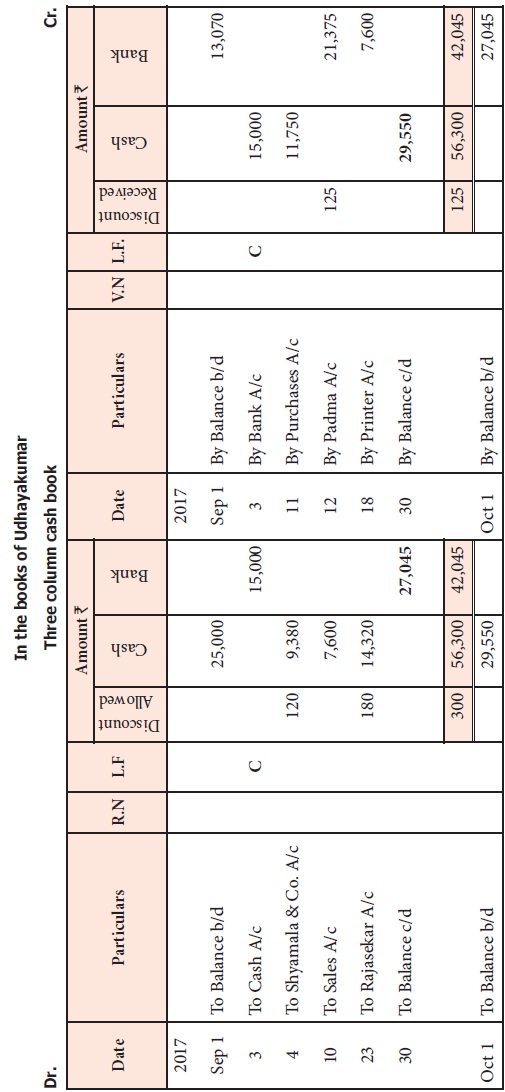

Illustration 7

From the following transactions prepare three column cash book of Udhayakumar

2017

Sep 1 Cash balance 25,000

1 Bank Balance (cr.) 13,070

3 Paid into bank 15,000

4 Received cash from Shyamala & Co., 9,380

Discount allowed to them Rs. 120

10 Goods sold for cash 7,600

11 Cash purchases 11,750

12 Gave Padma a Cheque for Rs. 21,375 and was allowed a discount of 125

18 Purchased a printer by cheque 7,600

23 Received cash from Rajasekar 14,320

Discount allowed to him Rs. 180

Solution for illustration 7

Related Topics