Production Analysis | Economics - Producer's Equilibrium | 11th Economics : Chapter 3 : Production Analysis

Chapter: 11th Economics : Chapter 3 : Production Analysis

Producer's Equilibrium

Producer’s

Equilibrium

Producer

equilibrium implies the situation where producer maximizes his output. It is

also known as optimum combination of the

factors of production. In short, the producer manufactures a given amount

of output with ‘least cost combination of

factors’, with his given budget.

Optimum Combination of Factors implies either

·

there is output maximisation for given inputs or

·

there is cost minimisation for the given output.

Conditions for Producer Equilibrium

The two

conditions that are to be fulfilled for the attainment of producer equilibrium

are:

·

The iso-cost line must be tangent to iso-quant

curve.

·

At point of tangency, the iso-quant curve must be

convex to the origin or MRTSLk must be declining.

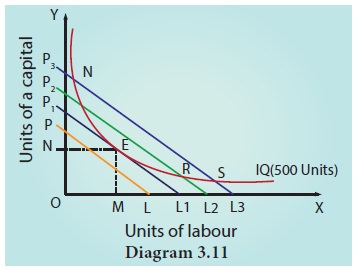

When the

outlay and prices of two factors, namely, labour and capital are given,

producers attain equilibrium (or least cost combination of factors is attained

by the firm) where the iso-cost line is tangent to an iso-product curve. It is

illustrated in the following Diagram 3.11.

In the

above figure, profit of the firm (or the producer) is maximised at the point of

equilibrium E.

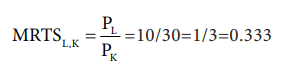

At the

point of equilibrium, the slope of the iso cost line is equal to the slope of

iso product curve (or the MRTS of labour for capital is equal to the price

ratio of the two factors)

Hence, it

can be stated as follows.

At point

E, the firm employs OM units of labour and ON units of capital. In other words,

it obtains least cost combination or optimum combination of the two factors to

produce the level of output denoted by the iso-quant IQ.

The other

points such as H, K, R and S lie on higher iso cost lines indicating that a

larger outlay is required, which exceeds the financial resources of the firm.

Related Topics