Economics - Perfect Competition | 11th Economics : Chapter 5 : Market Structure and Pricing

Chapter: 11th Economics : Chapter 5 : Market Structure and Pricing

Perfect Competition

Perfect

Competition:

It is an

ideal but imaginary market. 100% perfect completion cannot be seen. Perfect

Competition market is that type of market in which the number of buyers and

sellers is very large, all are engaged in buying and selling a homogenous

product at uniform price without any artificial restrictions and possessing

perfect knowledge of the market at a time.

According

to Joan Robinson, “Perfect competition

prevails when the demand for the output

of each producer is perfectly elastic”.

1. Features of the Perfect Combination:

a. Large Number of Buyers and Sellers

‘A large

number of buyers’ implies that each individual buyer buys a very, very small

quantum of a product as compared to that found in the market. This means that

he (he includes she also) has no power to fix the price of the product. He is only a price-taker and not a price-maker.

The term,

‘large number of sellers’ implies that share of each individual seller is a

very, very small quantum of a product. This means that he has no power to fix

the price of the product. Like the buyer, the seller also is only a price-taker and not a price-maker.

b. Homogeneous Product and Uniform Price

The

product sold and bought is homogeneous in nature, in the sense that the units

of the product are perfectly substitutable. All the units of the product are

identical (ie) of the same size, shape, colour, quality etc. Therefore, a uniform price prevails in the market.

c. Free Entry and Exit

In the

short run, it is possible for the very efficient producer, producing the

product at a very low cost, to earn super

normal profits. Attracted by such a profit, new firms enter into the

industry. When large number of firms enter, the supply (in comparison to

demand) would increase, resulting in lower price.

An

inefficient producer, who is unable to bring down the cost incurs loss.

Disturbed by the loss, the existing loss-incurring firms quit the market. If it

happens, supply will then decrease, price will go up. Existing firms could earn

more profit.

d. Absence Of Transport Cost

The

prevalence of the uniform price is also due to the absence of the transport

cost.

e. Perfect Mobility of Factors of Production

The

prevalence of the uniform price is also due to the perfect mobility of the

factors of production. As they enjoy perfect freedom to move from one place to

another and from one occupation to another, the price gets adjusted.

f. Perfect Knowledge of the Market

All

buyers and sellers have a thorough knowledge of the quality of the product,

prevailing price etc.

g. No

Government Intervention

There is

no government regulation on supply of raw materials, and in the determination

of price etc.

2. Perfect Competition: Firm’s Equilibrium in the Short Run

In the

short run, at least a few factors of production are fixed. The firms under

Perfect Competition take the price (10) from the industry and start adjusting

their quantities produced. For example Qd= 100 – 5P and Qs=5P. At equilibrium

Qd=Qs. Therefore 100-5P=5P

100 =

10P; 100/10 = P

Qd

= demand

P = 10

P = Price

Qd =

100-5(10)

Qs

= Supply

100-50 =

50

Qs =

5(10)=50

Therefore

50 = 50

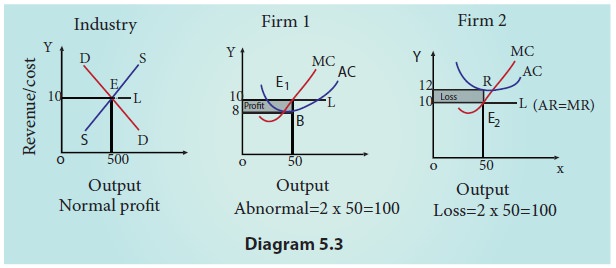

This

diagram consists of three panels. The equilibrium of an industry is explained

in the first panel. The demand and supply forces of all the firms interact and

the price is fixed as Rs.10. The equilibrium of an industry is obtained at 50

units of output.

In the

second part of the diagram, AC curve is lower than the price line. The

equilibrium condition is achieved where MC=MR. Its equilibrium quantity sold is

50. With the prevailing price, Rs.10 it experiences super normal profit. AC =

Rs.8, AR = Rs.10.

Price & Output Determination-Perfect Competition during Short Run

Its total

revenue is 50X10=500. Its total cost is 50X8=400. Therefore, its total profit

is 500-400=100.

In the

third part of the diagram, firm’s cost curve is above the price line. The

equilibrium condition is achieved at point where MR=MC. Its quantity sold is

50. With the prevailing price, it experiences loss. (AC>AR)

Its total

revenue is 50X10=500. Its total cost is 50X12=600. Therefore, its total loss is

600-500=100.

As profit prevails in the market, new firms

will enter the industry, thus increasing the supply of the product. This means

a decline in the price of the product and increase the cost of production.

Thus, the abnormal profit will be wiped out; loss will be incurved.

When loss prevails in the market, the

existing loss making firms will exit the industry, thus decreasing the supply

of the product. This means a rise in the price of the product and reduction in

the cost of production. So the loss will vanish; Profit will emerge. Consequent

upon the entry and exit of new firms into the industry, firms always earn

‘normal profit’ in the long run as shown in diagram.

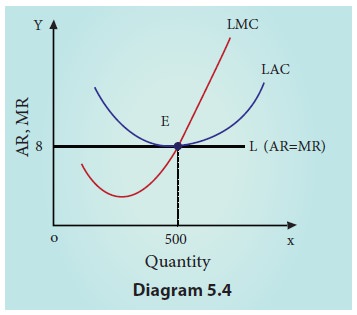

3. Perfect Competition: Firm’s Equilibrium in the Long Run (Normal Profit)

In the

long run, all the factors are variable.

The LAC curve is an envelope curve as it contains a few average cost curves. It is a flatter U shaped one. It is also known as planning curve. First, the firms will earn only normal profit.

Secondly, all the firms in the market are in equilibrium. This means that there should neither be a tendency for the new firms to enter into the industry nor for any of the existing firms to exit from the industry.

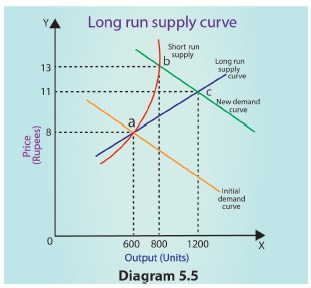

Long run

supply curve is explained to determine the long run price after an increase in

demand. The effect of the increase in demand in the short run is explained by

the movement from point ‘a’ to point ‘b’. The price increases from Rs.8 to Rs.13, and the quantity increases from 600 to

800 units. Economic profit of a firm is positive. Therefore, new firms enter

the market. In the long run new firms entry will continue until the price drops

to Rs.11 and the quantity is 1,200

units. The new long run equilibrium is shown by point ‘c’, where the new demand

curve intersects supply curve. At this price level ( Rs.11) and quantity (1,200

units). Due to diminishing returns, it is very difficult to increase output in

the short tun, as a result the price will increase to cover these higher cost

of production. New firms will enter into the market. The price

gradually drops to the point ( Rs.11) at which each firm makes zero economic

profit.

A firm

under perfect competition even in the long run is a price – taker, not a price

– maker. It takes the price of the product from the industry. And it

superimposes its cost curves on the revenue curves.

Long run

equilibrium of the firm is illustrated in the diagram. Under perfect

competition, long run equilibrium is only at minimum point of LAC. At point E,

LMC = MR = AR = LAC.

In the

above diagram (5.4), average cost is equal to average revenue. The equilibrium

of the firm finally rests at point E where price is 8 and output is 500.

(Numbers are hypothetical) At this point, the profit of the firm is only

normal. Thus condition for long run equilibrium of the firm is:

Price = AR=MR = Minimum AC

At the equilibrium

point, the SAC>LAC. Hence, long run equilibrium price is lower than short

run equilibrium price; long run equilibrium quantity is larger than short run

equilibrium quantity.

Related Topics