Economics - Monopolistic Competition | 11th Economics : Chapter 5 : Market Structure and Pricing

Chapter: 11th Economics : Chapter 5 : Market Structure and Pricing

Monopolistic Competition

Monopolistic

Competition

Monopolistic

competition refers to a market situation where there are many firms selling a

differentiated product. There is competition which is keen,

No firm can have

any perceptible influence on the price-output policies of the other sellers nor

can it be influenced much by their actions. Thus monopolistic competition

refers to competition among a large number of sellers producing close but not

perfect substitutes for each other.

1. Features of monopolistic competition

The

important features of monopolistic competition are :

i.

There are large number of buyers and many sellers.

ii.

Firms under monopolistic competition are price

makers. They set their own prices.

iii.

Firms produce differentiated products. It is the

key element of monopolistic competition.

iv.

There is a free entry and exit of firms.

v.

Firms compete with each other by incurring selling

cost or expenditure on sales promotion of their products.

vi.

Non – price competition is an essential part of

monopolistic competition.

vii.

A firm can follow an independent price policy.

2. Price and Output Determination under Monopolistic Competition

The firm

under monopolistic competition achieves its equilibrium when it’s MC = MR, and

when its MC curve cuts its MR curve from below. If MC is less than MR, the

sellers will find it profitable to expand their output.

Under

monopolistic competition

1.

The demand curve is downwards sloping.

2.

There are close substitutes.

3.

The demand curve (the average revenue curve) is

fairly elastic.

Under

monopolistic competition, different firms produce different varieties of the

product and sell them at different prices. Each firm under monopolistic

competition seeks to achieve equilibrium as regards

1. Price

and output, 2. Product adjustment and 3. selling cost adjustment.

Short-run equilibrium:

How does

a monopolistically competitive firm achieve price-output level equilibrium? The

profit maximisation is achieved when MC=MR.

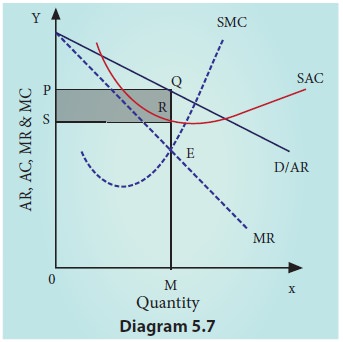

‘OM’ is

the equilibrium output. ‘OP’ is the equilibrium price. The total revenue is

‘OMQP’. And the total cost is ‘OMRS’. Therefore, total profit is ‘PQRS’. This

is super normal profit under short-run.

But under

differing revenue and cost conditions, the monopolistically competitive firms

many incur loss.

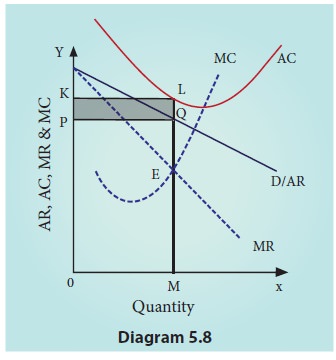

As shown

in the diagram, the AR and MR curves are fairly elastic. The equilibrium

situation occurs at point ‘E’, where MC = MR and MC cuts MR from below.

The

equilibrium output is OM and the equilibrium price is OP.

The total

revenue of the firm is ‘OMQP’ and the total cost of the firm is ‘OMLK’ and thus

the total loss is ‘PQLK’. This firm incurs loss in the short run.

Long-Run Equilibrium of the Firm and the Group Equilibrium

In the

short run a firm under monopolistic competition may earn super

But in the long run, the entry of the new firms in the

industry will wipe out the super normal profit earned by the existing firms.

The entry of new firms and exit of loss making firms will result in normal

profit for the firms in the industry.

In the

long run AR curve is more elastic or flatter, because plenty of substitutes are

available. Hence, the firms will earn only normal profit.

The only one condition for equilibrium in the short

run : MC = MR.

The two conditions for equilibrium in the long run

: MC = MR and AC = AR.

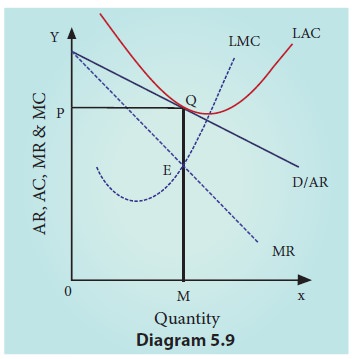

In the

diagram equilibrium is achieved at point ‘E’. The equilibrium output is ‘OM’

and the equilibrium price is ‘OP’. The average revenue at the equilibrium

output is ‘MQ’ and the average cost is also ‘MQ’. Thus, in the long run under

monopolistic competition, there is equilibrium when AR=AC and MC=MR. It means

that a firm earns normal profit. AR is tangent to the Long Run Average Cost

(LAC) curve at point ‘Q’.

3. Wastes of Monopolistic Competition

Generally

there are five kinds of wastages under monopolistic competition.

1. Idle Capacity: Unutilized

capacity is the difference between the optimum output that can be produced and the actual output produced by the firm. In the

long run, a monopolistic firm produces delibourately output which is less than

the optimum output that is the output corresponding to the minimum average

cost. This is done so mainly to create artificial and raise price. This leads

to excess capacity which is actually a waste in monopolistic competition. In

diagram 5.8., MF quantity of output refers to unused capacity. If OF is

produced, the society will get larger quantity with lower price.

2. Unemployment: Under monopolistic competition,

the firms produce less than optimum output.

As a result, the productive capacity is not used to the fullest extent. This

will lead to unemployment of human resources also.

3. Advertisement: There is

a lot of waste in competitive advertisements under monopolistic competition. The wasteful and competitive

advertisements lead to high cost to consumers. It is also claimed that

advertisements cheat the consumers by giving false. information about the

product.

4. Too Many Varieties of Goods: Introducing

too many varieties of a good is another waste

of monopolistic competition. The goods differ in size, shape, style and colour.

A reasonable number of varieties would be sufficient. Cost per unit can also be

reduced, if only a few varieties are produced in larger quantity Instead of

larger varieties with small quantity.

5. Inefficient Firms: Under

monopolistic competition, inefficient firms charge prices higher than their marginal cost. Such type of

inefficient firms should be kept out of the industry. But, the buyers’

preference for such products mostly due to emotions. enables the inefficient

firms to continue to exist. Efficient firms cannot drive out the inefficient

firms because sometimes the Efficient firms may not be able to Spend money on

attractive advertisement to lure the buyers. In reality, the consumers are

mostly emotional rather than rational, as stated by Richard Theiler, the Nobel

prize winner for the year 2017.Rational decision are made by mind; emotional

decisions are made by heart.

Monopsony

Monopsony

is a market structure in which there is only one buyer of a good or service. If

there is only one customer for a certain good, that customer has monopsony

power in the market for that good. Monopsony is analogous to monopoly, but

monopsony has market power on the demand side rather than on the supply side.

Bilateral Monopoly:

Bilateral monopoly refers to a market situation in

which a single producer (monopolist) of a product faces a single buyer

(monopsonist) of that product.

Related Topics