Accountancy - Grouping and codification of accounts | 11th Accountancy : Chapter 14 : Computerised Accounting

Chapter: 11th Accountancy : Chapter 14 : Computerised Accounting

Grouping and codification of accounts

Grouping and codification of accounts

When the volume and size of the business increase, the number of

transaction increases.![]() Therefore, it becomes necessary to have proper classification of data.

Therefore, it becomes necessary to have proper classification of data.

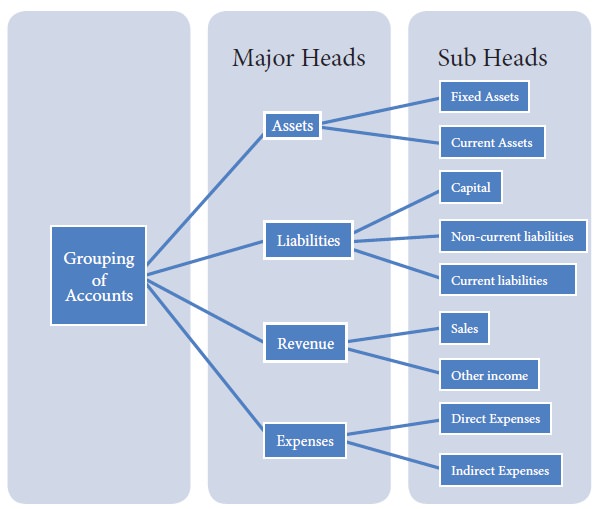

Grouping of accounts

In any organisation, the main unit of classification is the major head

which is further divided into minor heads. Each minor head may have number of

sub-heads. After classification of accounts into various groups namely, major,

minor and sub-heads and allotting codes to each account these are programmed

into the computer system.

A proper codification requires a systematic grouping of accounts. The

major groups or heads could be Assets, Liabilities, Revenues and Expenses. The

sub- groups or minor heads could be capital, non-current liabilities, current

assets, sales and so on.

In general, the basic classifications of different accounts embodied in

a transaction are resorted through accounting equation.

Assets = Liabilities + Capital +

(Revenues – Expenses)

Each component of the above equation can be divided into groups of

accounts as follows:

A. Liabilities and capital

Capital

·

Capital

·

Reserves

and surplus

Non-Current Liabilities

·

Long-term

borrowings

·

Other

long-term liabilities

Current liabilities

·

Short

term borrowings

·

Trade

payables

·

Other

current liabilities

B. Assets

Fixed tangible assets

·

Land and

building

·

Plant and

machinery

·

Furniture

and fixtures

Intangible assets

·

Goodwill

·

Copyright

·

Patents

Current Assets

·

Short

term investments

·

Inventories

·

Trade

receivables

·

Cash and

cash equivalents

·

Short

term loans and advances

·

Other

current assets

C. Revenues

·

Sales

·

Other

income

D. Expenses

·

Material

consumed

·

Wages

·

Manufacturing

expenses

·

Depreciation

·

Administrative

expenses

·

Interest

·

Selling

and distribution expenses, etc.

Codification of accounts

Code is an identification mark. Generally, computerised accounting

involves codification of accounts. Codification of accounts is needed where

there are numerous accounts heads in an organisation. There is a hierarchical

relationship between the groups and its components. In order to maintain the

hierarchical relationships between a group and its sub-groups, proper

codification is required.

The coding scheme of account heads should be such that it leads to

grouping of accounts at various levels so as to generate various reports. For

example, the codes for various accounts may be allotted as follows:

i.

Liabilities

and Capital

ii.

Assets

iii.

Revenues

iv.

Expenses

Under Liabilities and Capital

i.

Capital

ii.

Non-current

liabilities

iii.

Current

liabilities

Under Assets

i.

Non-current

assets

ii.

Current

assets

The above codification scheme utilises the hierarchy present in grouping

of accounts. Major advantage of such coding is that if the account codes are

listed in ascending order, these will be automatically listed as per the

desired hierarchy.

Methods of codification

Following are the three methods of codification.

a. Sequential codes

In sequential code, numbers

and/or letters are assigned in consecutive order. These codes are applied

primarily to source documents such as cheques, invoices, etc. A sequential code

can facilitate document search. For example:

Code Accounts

CL001 ABC LTD

CL002 XYZ LTD

CL003 SCERT

b. Block codes

In a block code, a range of numbers is partitioned into a desired number

of sub-ranges and each sub-range is allotted to a specific group. In most of

the cases of block codes, numbers within a sub-range follow sequential coding

scheme, i.e., the numbers increase consecutively. For example:

Code Dealer type

100 – 199 Small pumps

200 – 299 Medium pumps

300 – 399 Pipes

400 – 499 Motors

c. Mnemonic codes

A mnemonic code consists of

alphabets or abbreviations as symbols to codify a piece of information. For

example:

Code Information

SJ Sales Journals

HQ Head Quarters

Related Topics