Chapter: 11th Accountancy : Chapter 1 : Introduction to Accounting

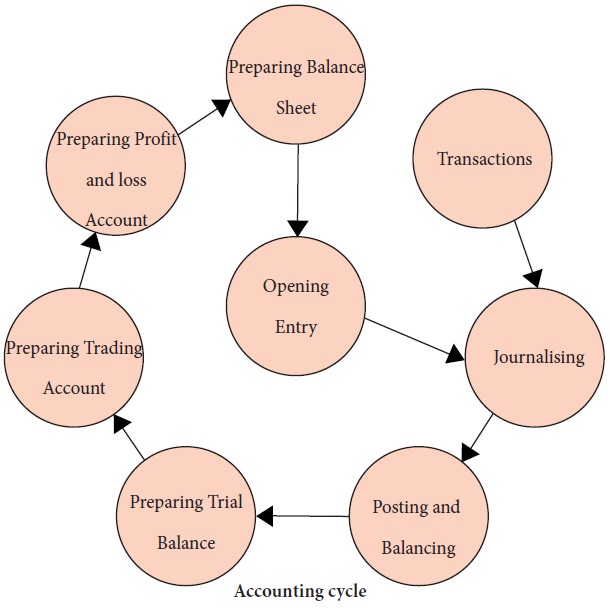

Accounting cycle

Accounting cycle

Accounting

cycle is the sequence of steps involved in the accounting process. Accounting

cycle starts with the identification and recording of financial transactions of

an organisation and ends with the preparation of final accounts for the

accounting year. The cycle continues for the next accounting year with the

opening balances of assets and liabilities which are the closing balances of

the preceding year. The steps involved are:

(i) Identifying the transactions and journalising

The first

step in the accounting process is identifying the financial transactions of a

business. All the monetary transactions are recorded in the books of original

entry called journals. Recording the transactions in the journal is called

journalising. Entries are made in the journals on the basis of source documents

in the chronological order, i.e., the order of occurrence of the transactions.

(ii) Posting and balancing

Transferring

the entries from the journal to the ledger is called posting. In the ledger,

entries are made in each account after classifying them under common heads.

Finding the differencebetween the total of the debit column and credit column

of all the ledger accounts is called balancing.

(iii) Preparation of trial balance

The list of

ledger balances namely trial balance is prepared as the next step. On the basis

of ledger balances the financial statements are prepared.

(iv) Preparation of trading account

Next step is

preparation of trading account for a particular accounting period. All the

direct revenues and direct expenses are transferred to trading account. The

balance in the trading account is the gross profit or gross loss.

(v) Preparation of profit and loss account

Profit and

loss account is prepared next for a particular accounting period. All the

indirect revenues and indirect expenses along with gross profit or gross loss

are transferred to profit and loss account. The balance in the profit and loss

account is the net profit or net loss.

(vi) Preparation of balance sheet

A statement

showing the balances of assets and liabilities namely balance sheet is prepared

as the final step in the accounting process. It is prepared on a particular

date, normally, on the last day of the accounting period.![]()

The closing

balances of an accounting year are taken as the opening balances for the next

accounting year. The transactions identified and recorded for the next year are

followed by posting and other steps.

The results

are communicated to the users of accounting information for the purpose of

analysis and decision making.

Related Topics