Chapter: Principles of Management : Planning

Planning process

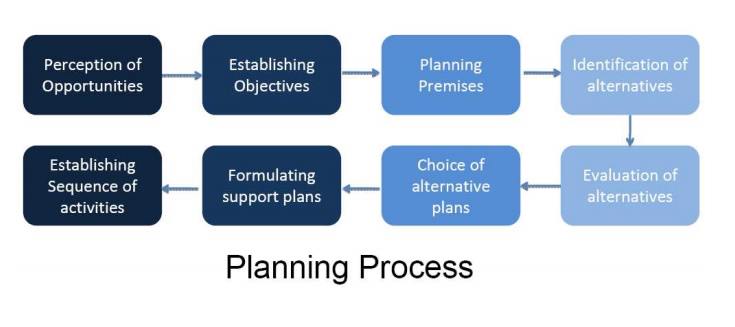

PLANNING PROCESS

The various steps involved in planning are given below

a) Perception of Opportunities:

Although preceding actual planning and therefore not strictly a part of

the planning process, awareness of an opportunity is the real starting point

for planning. It includes a preliminary look at possible future opportunities

and the ability to see them clearly and completely, knowledge of where we stand

in the light of our strengths and weaknesses, an understanding of why we wish

to solve uncertainties, and a vision of what we expect to gain. Setting

realistic objectives depends on this awareness. Planning requires realistic

diagnosis of the opportunity situation.

b) Establishing Objectives:

The first step in planning itself is to establish objectives for the

entire enterprise and then for each subordinate unit. Objectives specifying the

results expected indicate the end points of what is to be done, where the

primary emphasis is to be placed, and what is to be accomplished by the network

of strategies, policies, procedures, rules, budgets and programs.

Enterprise objectives should give direction to the nature of all major

plans which, by reflecting these objectives, define the objectives of major

departments. Major department objectives, in turn, control the objectives of

subordinate departments, and so on down the line. The objectives of lesser

departments will be better framed, however, if subdivision managers understand

the overall enterprise objectives and the implied derivative goals and if they

are given an opportunity to contribute their ideas to them and to the setting

of their own goals.

c) Considering the Planning Premises:

Another

logical step in planning is to establish, obtain agreement to utilize and

disseminate critical planning premises. These are forecast data of a factual

nature, applicable basic policies, and existing company plans. Premises, then,

are planning assumptions – in other words, the expected environment of plans in

operation. This step leads to one of the major principles of planning.

The more individuals charged with planning understand and agree to

utilize consistent planning premises, the more coordinated enterprise planning

will be.

Planning premises include far more than the usual basic forecasts of

population, prices, costs, production, markets, and similar matters.

Because the future environment of plans is so complex, it would not be

profitable or realistic to make assumptions about every detail of the future

environment of a plan.

Since agreement to utilize a given set of premises is important to

coordinate planning, it becomes a major responsibility of managers, starting

with those at the top, to make sure that subordinate managers understand the

premises upon which they are expected to plan. It is not unusual for chief

executives in well- managed companies to force top managers with differing

views, through group deliberation, to arrive at a set of major premises that

all can accept.

d) Identification of alternatives:

Once the organizational objectives have been clearly stated and the

planning premises have been developed, the manager should list as many

available alternatives as possible for reaching those objectives.

The focus of this step is to search for and examine alternative courses

of action, especially those not immediately apparent. There is seldom a plan

for which reasonable alternatives do not exist, and quite often an alternative

that is not obvious proves to be the best.

The more

common problem is not finding alternatives, but reducing the number of

alternatives so that the most promising may be analyzed. Even with mathematical

techniques and the computer, there is a limit to the number of alternatives

that may be examined. It is therefore usually necessary for the planner to

reduce by preliminary examination the number of alternatives to those promising

the most fruitful possibilities or by mathematically eliminating, through the

process of approximation, the least promising ones.

e) Evaluation of alternatives

Having sought out alternative courses and examined their strong and weak

points, the following step is to evaluate them by weighing the various factors

in the light of premises and goals. One course may appear to be the most profitable

but require a large cash outlay and a slow payback; another may be less

profitable but involve less risk; still another may better suit the company in

long–range objectives.

If the only objective were to examine profits in a certain business

immediately, if the future were not uncertain, if cash position and capital

availability were not worrisome, and if most factors could be reduced to

definite data, this evaluation should be relatively easy. But typical planning

is replete with uncertainties, problems of capital shortages, and intangible

factors, and so evaluation is usually very difficult, even with relatively

simple problems. A company may wish to enter a new product line primarily for

purposes of prestige; the forecast of expected results may show a clear

financial loss, but the question is still open as to whether the loss is worth

the gain.

f) Choice of alternative plans

An

evaluation of alternatives must include an evaluation of the premises on which

the alternatives are based. A manager usually finds that some premises are

unreasonable and can therefore be excluded from further consideration. This

elimination process helps the manager determine which alternative would best

accomplish organizational objectives.

g) Formulating of Supporting Plans

After

decisions are made and plans are set, the final step to give them meaning is to

numberize them by converting them to budgets. The overall budgets of an

enterprise represent the sum total of income and expenses with resultant profit

or surplus and budgets of major balance– sheet items such as cash and capital

expenditures. Each department or program of a business or other enterprise can

have its own budgets, usually of expenses and capital expenditures, which tie

into the overall budget.

If this process is done well, budgets become a means of adding together

the various plans and also important standards against which planning progress

can be measured.

h) Establishing sequence of activities

Once plans

that furnish the organization with both long-range and short-range direction

have been developed, they must be implemented. Obviously, the organization can

not directly benefit from planning process until this step is performed.

Related Topics