Chapter: Introduction to the Design and Analysis of Algorithms : Iterative Improvement

The Simplex Method

The Simplex Method

We have already encountered

linear programming (see Section 6.6)—the general problem of optimizing a linear

function of several variables subject to a set of linear constraints:

We mentioned there that many important practical problems can be modeled as instances of linear programming. Two researchers, L. V. Kantorovich of the former Soviet Union and the Dutch-American T. C. Koopmans, were even awarded the Nobel Prize in 1975 for their contributions to linear programming theory and its applications to economics. Apparently because there is no Nobel Prize in mathematics, the Royal Swedish Academy of Sciences failed to honor the U.S. mathematician G. B. Dantzig, who is universally recognized as the father of linear programming in its modern form and the inventor of the simplex method, the classic algorithm for solving such problems.

Geometric

Interpretation of Linear Programming

Before we introduce a general

method for solving linear programming problems, let us consider a small

example, which will help us to see the fundamental prop-erties of such

problems.

EXAMPLE

1 Consider the following linear programming problem in two

variables:

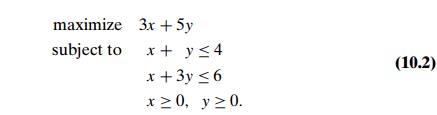

By definition, a feasible

solution to this problem is any point (x, y) that satisfies all the constraints of the

problem; the problem’s feasible region is the set of all

its feasible points. It is instructive to sketch the feasible region in the

Cartesian plane. Recall that any equation ax + by = c, where coefficients a and b are not both equal to zero, defines a straight

line. Such a line divides the plane into two half-planes: for all the points in

one of them, ax + by

< c, while for all the points in the other, ax + by

> c. (It is easy to determine which of the two half-planes is which:

take any point (x0, y0) not on the line ax + by = c and check which of the two

inequalities hold, ax0 + by0 > c or ax0 + by0 < c.) In particular, the set of points defined by

inequality x + y ≤ 4 comprises the points on and below the line x + y = 4, and the set of points defined by inequality x + 3y ≤ 6 comprises the points on and below the line x + 3y = 6. Since the points of the

feasible region must satisfy all the constraints of the problem, the feasible

region is obtained by the intersection of these two half-planes and the first

quadrant of the Cartesian plane defined by the nonnegativity constraints x ≥ 0,

y ≥ 0 (see Figure 10.1). Thus,

the feasible region for problem (10.2) is the convex polygon with the vertices (0, 0), (4, 0), (0, 2), and (3, 1). (The last point, which is the point of intersection

of the lines x + y = 4 and x + 3y = 6, is obtained by solving the system of these

two linear equations.) Our task is to find an optimal solution, a point

in the feasible region with the largest value of the objective function z = 3x + 5y.

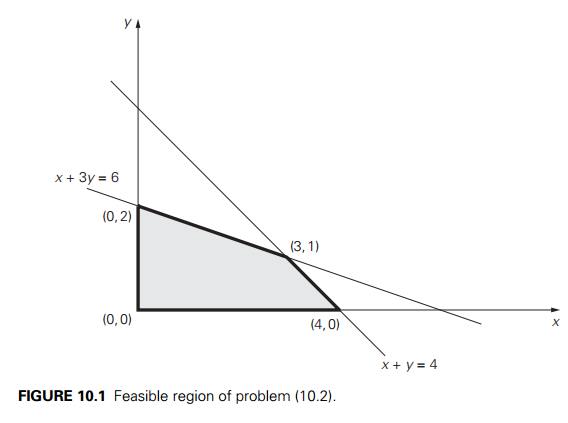

Are there feasible solutions

for which the value of the objective function equals, say, 20? The points (x, y) for which the objective function z = 3x + 5y is equal to 20 form the line

3x + 5y = 20. Since this line does not

have common points

with the feasible region—see

Figure 10.2—the answer to the posed question is no. On the other hand, there

are infinitely many feasible points for which the objective function is equal

to, say, 10: they are the intersection points of the line 3x + 5y = 10 with the feasible region. Note that the

lines 3x + 5y = 20 and 3x + 5y = 10 have the same slope, as would any line

defined by equation 3x + 5y = z where z is some constant. Such lines are called level

lines of the objective function. Thus, our problem can be restated as

finding the largest value of the parameter z for which the level line 3x + 5y = z has a common point with the

feasible region.

We can find this line either

by shifting, say, the line 3x + 5y = 20 south-west (without changing its slope!)

toward the feasible region until it hits the region for the first time or by

shifting, say, the line 3x + 5y = 10 north-east until it hits the feasible

region for the last time. Either way, it will happen at the point (3, 1) with the corresponding z value 3 . 3 + 5 . 1 = 14. This means that the optimal

solution to the linear programming problem in question is x = 3,

y = 1, with the maximal value of the objective

function equal to 14.

Note that if we had to maximize

z = 3x + 3y as the objective function in

problem (10.2), the level line 3x + 3y = z for the largest value of z would coincide with the boundary line segment

that has the same slope as the level lines (draw this line in Figure 10.2).

Consequently, all the points of the line segment between vertices (3, 1) and (4, 0), including the vertices themselves, would be

optimal solutions, yielding, of course, the same maximal value of the objective

function.

Does every linear programming

problem have an optimal solution that can be found at a vertex of its feasible

region? Without appropriate qualifications, the answer to this question is no.

To begin with, the feasible region of a linear programming problem can be

empty. For example, if the constraints include two contradictory requirements,

such as x + y ≤ 1 and x + y ≥ 2, there can be no points in the

problem’s feasible region. Linear programming problems with the empty feasible

region are called infeasible. Obviously, infeasible problems do not have optimal

solutions.

Another complication may

arise if the problem’s feasible region is unbounded, as the following example

demonstrates.

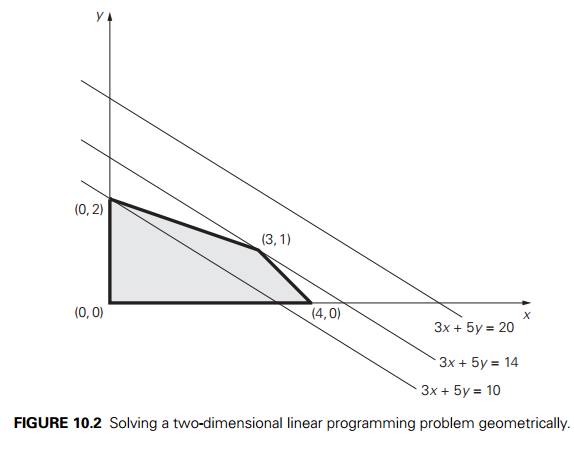

EXAMPLE

2 If we reverse the inequalities in problem (10.2) to x + y ≥ 4 and x + 3y ≥ 6, the feasible region of the

new problem will become unbounded (see Figure 10.3). If the feasible region of a

linear programming problem is unbounded, its objective function may or may not

attain a finite optimal value on it. For example, the problem of maximizing z = 3x + 5y subject to the constraints x + y ≥ 4, x + 3y ≥ 6,

x ≥ 0, y ≥ 0 has no optimal solution, because there are

points in the feasible region making 3x + 5y as large as we wish. Such

problems are called unbounded. On the other hand, the problem of minimizing z = 3x + 5y subject to the

same constraints has an optimal solution (which?).

Fortunately, the most

important features of the examples we considered above hold for problems with

more than two variables. In particular, a feasible region of a typical linear

programming problem is in many ways similar to convex polygons in the two-dimensional

Cartesian plane. Specifically, it always has a finite number of vertices, which

mathematicians prefer to call extreme points (see Section 3.3).

Furthermore, an optimal solution to a linear programming problem can be found

at one of the extreme points of its feasible region. We reiterate these

properties in the following theorem.

THEOREM

(Extreme Point Theorem) Any linear programming

problem with a nonempty bounded feasible region has an

optimal solution; moreover, an op-timal solution can always be found at an

extreme point of the problem’s feasible region.2

This theorem implies that to

solve a linear programming problem, at least in the case of a bounded feasible

region, we can ignore all but a finite number of points in its feasible region.

In principle, we can solve such a problem by computing the value of the

objective function at each extreme point and selecting the one with the best

value. There are two major obstacles to implementing this plan, however. The

first lies in the need for a mechanism for generating the extreme points of the

feasible region. As we are going to see below, a rather straightforward

algebraic procedure for this task has been discovered. The second obstacle lies

in the number of extreme points a typical feasible region has. Here, the news

is bad: the number of extreme points is known to grow exponentially with the

size of the problem. This makes the exhaustive inspection of extreme points

unrealistic for most linear programming problems of nontrivial sizes.

Fortunately, it turns out

that there exists an algorithm that typically inspects only a small fraction of

the extreme points of the feasible region before reaching an optimal one. This

famous algorithm is called the simplex method. The idea of this

algorithm can be described in geometric terms as follows. Start by identifying

an extreme point of the feasible region. Then check whether one can get an

improved value of the objective function by going to an adjacent extreme point.

If it is not the case, the current point is optimal—stop; if it is the case,

proceed to an adjacent extreme point with an improved value of the objective

function. After a finite number of steps, the algorithm will either reach an

extreme point where an optimal solution occurs or determine that no optimal

solution exists.

An

Outline of the Simplex Method

Our task now is to

“translate” the geometric description of the simplex method into the more

algorithmically precise language of algebra. To begin with, before we can apply

the simplex method to a linear programming problem, it has to be represented in

a special form called the standard form. The standard form has

the following requirements:

It must be a maximization

problem.

All the constraints (except

the nonnegativity constraints) must be in the form of linear equations with

nonnegative right-hand sides.

All the variables must be

required to be nonnegative.

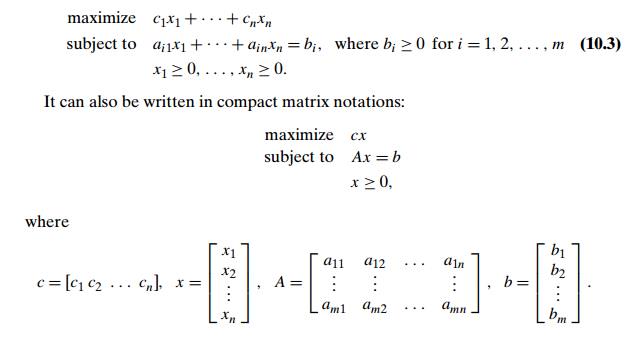

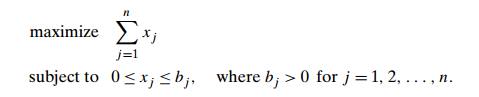

Thus, the general linear

programming problem in standard form with m constraints and n unknowns (n ≥ m) is

Any linear programming

problem can be transformed into an equivalent problem in standard form. If an

objective function needs to be minimized, it can be replaced by the equivalent

problem of maximizing the same objective function with all its coefficients cj replaced by −cj , j = 1, 2, . . . , n (see Section 6.6 for a more

general discussion of such transformations). If a constraint is given as an

inequality, it can be replaced by an equivalent equation by adding a slack

variable representing the difference between the two sides of the

original inequality. For example, the two inequalities of problem (10.2) can be

transformed, respectively, into the following equations:

x + y + u = 4 where u ≥ 0 and x + 3y + v = 6 where v ≥ 0.

Finally, in most linear

programming problems, the variables are required to be nonnegative to begin

with because they represent some physical quantities. If this is not the case

in an initial statement of a problem, an unconstrained variable

xj can be replaced by the difference between two

new nonnegative variables: xj = x'j − x''j , x'j ≥ 0,

x''j ≥ 0.

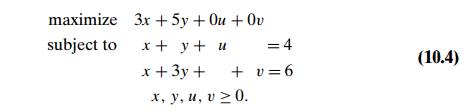

Thus, problem (10.2) in

standard form is the following linear programming problem in four variables:

It is easy to see that if we

find an optimal solution (x∗, y∗, u∗, v∗) to problem (10.4), we can obtain an optimal

solution to problem (10.2) by simply ignoring its last two coordinates.

The principal advantage of

the standard form lies in the simple mechanism it provides for identifying

extreme points of the feasible region. To do this for problem (10.4), for

example, we need to set two of the four variables in the con-straint equations

to zero to get a system of two linear equations in two unknowns and solve this

system. For the general case of a problem with m equations in n unknowns (n ≥ m), n − m variables need to be set to

zero to get a system of m equations in m unknowns. If the system obtained has a unique

solution—as any nondegenerate system of linear equations with the number of

equations equal to the number of unknowns does—we have a basic solution; its

coordinates set to zero before solving the system are called nonbasic,

and its coordinates obtained by solving the system are called basic.

(This terminology comes from linear algebra.

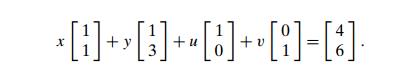

Specifically, we can rewrite

the system of constraint equations of (10.4) as

A basis in the

two-dimensional vector space is composed of any two vectors that are not

proportional to each other; once a basis is chosen, any vector can be uniquely

expressed as a sum of multiples of the basis vectors. Basic and nonba-sic

variables indicate which of the given vectors are, respectively, included and

excluded in a particular basis choice.)

If all the coordinates of a

basic solution are nonnegative, the basic solution is called a basic

feasible solution. For example, if we set to zero variables x and y and solve the resulting system for u and v, we obtain the basic feasible solution (0, 0, 4, 6); if we set to zero variables x and u

and solve the resulting system for y and v, we obtain the basic solution

(0, 4, 0, −6), which is not feasible. The

impor-tance of basic feasible solutions lies in the one-to-one correspondence

between them and the extreme points of the feasible region. For example, (0, 0, 4, 6) is an extreme point of the feasible region of

problem (10.4) (with the point (0, 0) in Fig-ure 10.1 being its

projection on the x,

y plane). Incidentally, (0, 0, 4, 6) is a natural starting point

for the simplex method’s application to this problem.

As mentioned above, the

simplex method progresses through a series of adjacent extreme points (basic

feasible solutions) with increasing values of the objective function. Each such

point can be represented by a simplex tableau, a table storing the

information about the basic feasible solution corresponding to the extreme

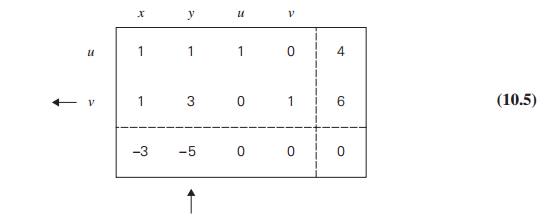

point. For example, the simplex tableau for (0, 0, 4, 6) of problem (10.4) is presented below:

In general, a simplex tableau

for a linear programming problem in standard form with n unknowns and m linear equality constraints (n ≥ m) has m + 1 rows and n + 1 columns. Each of the first m rows of the table contains the coefficients of a corresponding constraint equation, with the

last column’s entry containing the equation’s right-hand side. The columns,

except the last one, are labeled by the names of the variables. The rows are

labeled by the basic variables of the basic feasible solution the tableau represents;

the values of the basic variables of this solution are in the last column. Also

note that the columns labeled by the basic variables form the m × m identity matrix.

The last row of a simplex

tableau is called the objective row. It is initialized by

the coefficients of the objective function with their signs reversed (in the

first n columns) and the value of the

objective function at the initial point (in the last column). On subsequent iterations, the

objective row is transformed the same way as all the other rows. The objective

row is used by the simplex method to check whether the current tableau

represents an optimal solution: it does if all the entries in the objective

row—except, possibly, the one in the last column—are nonnegative. If this is

not the case, any of the negative entries indicates a nonbasic variable that

can become basic in the next tableau.

For example, according to

this criterion, the basic feasible solution (0, 0, 4, 6) represented by tableau (10.5) is not optimal.

The negative value in the x-column signals the fact that

we can increase the value of the objective function z = 3x + 5y + 0u + 0v by increasing the value of

the x-coordinate in the current

basic feasible solution (0, 0, 4, 6). Indeed, since the

coefficient for x in the objective function is

positive, the larger the x value, the larger the value

of this function. Of course, we will need to “compensate” an increase in x by adjusting the values of the basic variables

u and v so that the new point is still feasible. For

this to be the case, both conditions

x + u = 4 where u ≥ 0 x

+ v = 6 where v ≥ 0

must be satisfied, which

means that

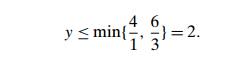

x ≤ min{4, 6} = 4.

Note that if we increase the

value of x from 0 to 4, the largest

amount possible, we will find ourselves at the point (4, 0, 0, 2), an adjacent to (0, 0, 4, 6) extreme point of the feasible region, with z = 12.

Similarly, the negative value

in the y-column of the objective row

signals the fact that we can also increase the value of the objective function

by increasing the value of the y-coordinate in the initial

basic feasible solution (0, 0, 4, 6). This requires

y + u = 4 where u ≥ 0 3y + v = 6 where v ≥ 0,

which means that

If we increase the value of y from 0 to 2, the largest amount possible, we

will find ourselves at the point (0, 2, 2, 0), another adjacent to (0, 0, 4, 6) extreme point, with z = 10.

If there are several negative

entries in the objective row, a commonly used rule is to select the most

negative one, i.e., the negative number with the largest absolute value. This

rule is motivated by the observation that such a choice yields the largest

increase in the objective function’s value per unit of change in a vari-able’s

value. (In our example, an increase in the x-value from 0 to 1 at (0, 0, 4, 6) changes the value of z = 3x + 5y + 0u + 0v from 0 to 3, while an

increase in the y-value from 0 to 1 at (0, 0, 4, 6) changes z from 0 to 5.) Note, however, that the feasibility constraints impose different limits

on how much each of the variables may increase. In our example, in particular,

the choice of the y-variable over the x-variable leads to a smaller increase in the

value of the objective function. Still, we will employ this commonly used rule and

select variable y as we continue with our

example. A new basic variable is called the entering variable, while

its column is referred to as the pivot column; we mark the pivot

column by ↑ .

Now we will explain how to

choose a departing variable, i.e., a basic variable to become nonbasic

in the next tableau. (The total number of basic variables in any basic solution

must be equal to m, the number of the equality

constraints.) As we saw above, to get to an adjacent extreme point with a

larger value of the objective function, we need to increase the entering

variable by the largest amount possible to make one of the old basic variables

zero while preserving the nonnegativity of all the others. We can translate

this observation into the following rule for choosing a departing variable in a

simplex tableau: for each positive

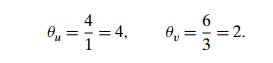

entry in the pivot column, compute the θ -ratio by dividing the row’s last

entry by the entry in the pivot column. For the example of tableau (10.5),

these θ -ratios are

The row with the smallest θ -ratio determines the departing variable,

i.e., the variable to become nonbasic. Ties may be broken arbitrarily. For our

example, it is variable v. We mark the row of the

departing variable, called the pivot row, by ←

and denote it row. Note that

if there are no positive entries in the pivot column, no θ -ratio can be computed, which indicates that

the problem is unbounded and the algorithm stops.

Finally, the following steps

need to be taken to transform a current tableau into the next one. (This

transformation, called pivoting, is similar to the

princi-pal step of the Gauss-Jordan elimination algorithm for solving systems

of linear equations—see Problem 8 in Exercises 6.2.) First, divide all the

entries of the pivot

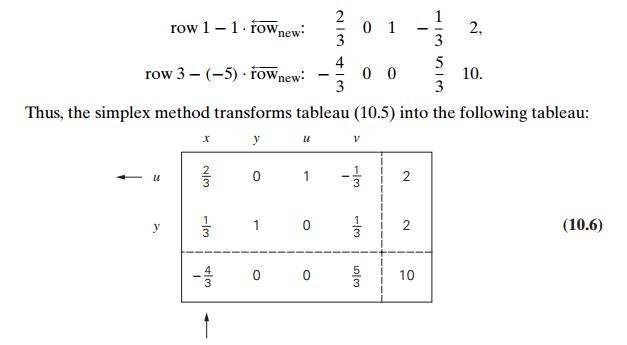

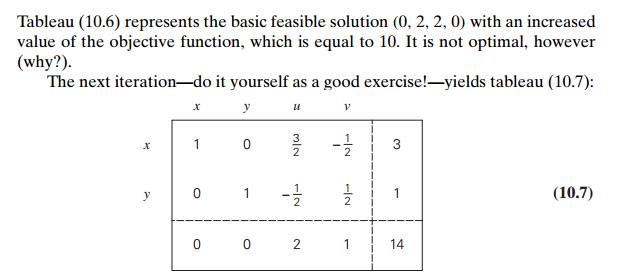

Tableau (10.6) represents the

basic feasible solution (0, 2, 2, 0) with an increased value of

the objective function, which is equal to 10. It is not optimal, however

(why?).

The next iteration—do it

yourself as a good exercise!—yields tableau (10.7):

This tableau represents the

basic feasible solution (3, 1, 0, 0). It is optimal because all

the entries in the objective row of tableau (10.7) are nonnegative. The maximal

value of the objective function is equal to 14, the last entry in the objective

row.

Let us summarize the steps of

the simplex method.

Summary

of the simplex method

Step 0 Initialization Present a given linear programming problem in stan-dard form and

set up an initial tableau with nonnegative entries in the rightmost column and m other columns composing the m × m identity matrix. (Entries in

the objective row are to be disregarded in verifying these requirements.) These

m columns define the basic

variables of the initial basic feasible solution, used as the labels of the

tableau’s rows.

Step 1 Optimality test If all the entries in the objective row (except, possibly, the one in the rightmost column, which

represents the value of the objective function) are nonnegative—stop: the

tableau represents an optimal solution whose basic variables’ values are in the

rightmost column and the remaining, nonbasic variables’ values are zeros.

Step 2 Finding the entering variable Select a negative entry from among the first n elements of the objective

row. (A commonly used rule is to select the negative entry with the largest

absolute value, with ties broken arbitrarily.) Mark its column to indicate the

entering variable and the pivot column.

Step 3 Finding the departing

variable For each positive entry in

the pivot column, calculate the θ -ratio by dividing that row’s entry in the

right-most column by its entry in the pivot column. (If all the entries in the

pivot column are negative or zero, the problem is unbounded—stop.) Find the row

with the smallest θ -ratio (ties may be broken

arbitrarily), and mark this row to indicate the departing variable and the

pivot row.

Step 4 Forming the next tableau Divide all the entries in the pivot row by its entry in the pivot column. Subtract from each of the other

rows, including the objective row, the new pivot row multiplied by the entry in

the pivot column of the row in question. (This will make all the entries in the

pivot column 0’s except for 1 in the pivot row.) Replace the label of the pivot

row by the variable’s name of the pivot column and go back to Step 1.

Further

Notes on the Simplex Method

Formal proofs of validity of

the simplex method steps can be found in books devoted to a detailed discussion

of linear programming (e.g., [Dan63]). A few important remarks about the method

still need to be made, however. Generally speaking, an iteration of the simplex

method leads to an extreme point of the prob-lem’s feasible region with a

greater value of the objective function. In degenerate cases, which arise when

one or more basic variables are equal to zero, the simplex method can only

guarantee that the value of the objective function at the new extreme point is

greater than or equal to its value at the previous point. In turn, this opens

the door to the possibility not only that the objective function’s values

“stall” for several iterations in a row but that the algorithm might cycle back

to a previously considered point and hence never terminate. The latter

phenomenon is called cycling. Although it rarely if ever

happens in practice, specific examples of problems where cycling does occur

have been constructed. A simple modifica-tion of Steps 2 and 3 of the simplex

method, called Bland’s rule, eliminates even the theoretical possibility of

cycling. Assuming that the variables are denoted by a subscripted letter (e.g.,

x1, x2, . . . , xn), this rule can be stated as follows:

Step 2 modified Among the columns with a negative entry in the

objective row, select the column

with the smallest subscript.

Step 3 modified Resolve a tie among the smallest θ -ratios by selecting the row labeled by the basic variable with

the smallest subscript.

Another caveat deals with the

assumptions made in Step 0. They are automat-ically satisfied if a problem is

given in the form where all the constraints imposed on nonnegative variables

are inequalities ai1x1 + . . . + ainxn ≤ bi with bi ≥ 0 for i = 1, 2, . . . , m. Indeed, by adding a

nonnegative slack variable xn+i into the ith constraint, we obtain the

equality ai1x1 + . . . + ainxn + xn+i = bi, and all the re-quirements imposed on an

initial tableau of the simplex method are satisfied for

the

obvious basic feasible solution x1 = . . . = xn = 0, xn+1 = . . . = xn+m = 1. But if

a problem is not given in such a form, finding an initial basic feasible

solution

may present a nontrivial

obstacle. Moreover, for problems with an empty feasible region, no initial

basic feasible solution exists, and we need an algorithmic way to identify such

problems. One of the ways to address these issues is to use an exten-sion to the

classic simplex method called the two-phase simplex method (see, e.g.,

[Kol95]). In a nutshell, this method adds a set of artificial variables to the

equality constraints of a given problem so that the new problem has an obvious

basic fea-sible solution. It then solves the linear programming problem of

minimizing the sum of the artificial variables by the simplex method. The

optimal solution to this problem either yields an initial tableau for the

original problem or indicates that the feasible region of the original problem

is empty.

How efficient is the simplex

method? Since the algorithm progresses through a sequence of adjacent points of

a feasible region, one should probably expect bad news because the number of

extreme points is known to grow exponentially with the problem size. Indeed,

the worst-case efficiency of the simplex method has been shown to be

exponential as well. Fortunately, more than half a century of practical

experience with the algorithm has shown that the number of iterations in a

typical application ranges between m and 3m, with the number of operations per iteration

proportional to mn, where m and n are the numbers of equality constraints and

variables, respectively.

Since its discovery in 1947,

the simplex method has been a subject of intensive study by many researchers.

Some of them have worked on improvements to the original algorithm and details

of its efficient implementation. As a result of these efforts, programs

implementing the simplex method have been polished to the point that very large

problems with hundreds of thousands of constraints and variables can be solved

in a routine manner. In fact, such programs have evolved into sophisticated

software packages. These packages enable the user to enter a problem’s

constraints and obtain a solution in a user-friendly form. They also provide

tools for investigating important properties of the solution, such as its

sensitivity to changes in the input data. Such investigations are very

important for many applications, including those in economics. At the other end

of the spectrum, linear programming problems of a moderate size can nowadays be

solved on a desktop using a standard spreadsheet facility or by taking

advantage of specialized software available on the Internet.

Researchers have also tried

to find algorithms for solving linear programming problems with polynomial-time

efficiency in the worst case. An important mile-stone in the history of such

algorithms was the proof by L. G. Khachian [Kha79] showing that the ellipsoid

method can solve any linear programming problem in polynomial time.

Although the ellipsoid method was much slower than the simplex method in

practice, its better worst-case efficiency encouraged a search for

alterna-tives to the simplex method. In 1984, Narendra Karmarkar published an

algorithm that not only had a polynomial worst-case efficiency but also was

competitive with the simplex method in empirical tests as well. Although we are

not going to discuss Karmarkar’s algorithm [Kar84] here,

it is worth pointing out that it is also based on the

iterative-improvement idea. However, Karmarkar’s algorithm generates a sequence

of feasible solutions that lie within the feasible region rather than going

through a sequence of adjacent extreme points as the simplex method does. Such

algorithms are called interior-point methods (see, e.g.,

[Arb93]).

Exercises 10.1

Consider the following version of the post office location problem

(Problem 3 in Exercises 3.3): Given n integers x1, x2, . . . , xn representing coordinates of n villages located along a straight road, find a

location for a post office that minimizes the average distance between the

villages. The post office may be, but is not required to be, located at one of

the villages. Devise an iterative-improvement algorithm for this problem. Is this

an efficient way to solve this problem?

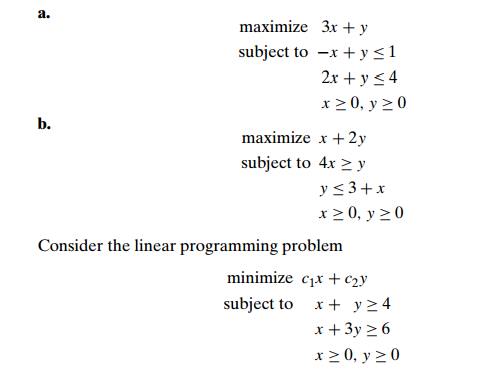

Solve the following linear

programming problems geometrically.

where c1 and c2 are some real numbers not both equal to zero.

Give an example of the

coefficient values c1 and c2 for which the problem has a unique optimal

solution.

Give an example of the coefficient values c1 and c2 for which the problem has infinitely many

optimal solutions.

Give an example of the coefficient values c1 and c2 for which the problem does not have an optimal

solution.

Would the solution to problem (10.2) be different if its inequality

constraints were strict, i.e., x + y

< 4 and x + 3y

< 6, respectively?

Trace the simplex method on

the problem of Exercise 2a.

the problem of Exercise 2b.

Trace the simplex method on the problem of Example 1 in Section 6.6

by hand.

by using one of the implementations available on the Internet.

Determine how many iterations the simplex method needs to solve the

problem

Can we apply the simplex method to solve the knapsack problem (see

Exam-ple 2 in Section 6.6)? If you answer yes, indicate whether it is a good

algorithm for the problem in question; if you answer no, explain why not.

Prove that no linear programming problem can have exactly k ≥ 1 optimal solutions unless k = 1.

If a linear programming problem

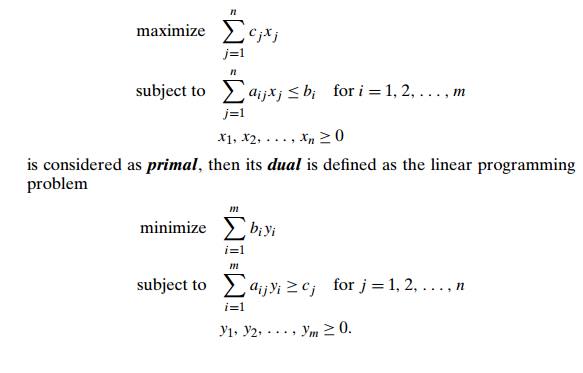

Express the primal and dual problems in matrix notations.

Find the dual of the linear programming problem

maximize x1 + 4x2 − x3 subject to x1 + x2 + x3 ≤ 6

x1 − x2 − 2x3 ≤ 2 x1, x2, x3 ≥ 0.

Solve the primal and dual problems and compare the optimal values

of their objective functions.

Related Topics