Chapter: Mechanical : Engineering Economics & Cost Analysis : Introduction to Economics

Laws of supply and demand

Laws of supply and demand

i.Laws of supply - states that the quantity of a commodity supplied varies directly with the price, other determinants of supply remaining constant.

ü If the cost of inputs increases, then naturally, the cost of the product will go up. In such a situation, at the prevailing price of the product the profit margin per unit will be less.

ü The producers will then reduce the production quantity, which in turn will affect the supply of the product.

ü For instance, if the prices of fertilizers and cost of labour are increased significantly, in agriculture, the profit margin per bag of paddy will be reduced.

ü So, the farmers will reduce the area of cultivation, and hence the quantity of supply of paddy will be reduced at the prevailing prices of the paddy.

ü If there is an advancement in technology used in the manufacture of the product in the long run, there will be a reduction in the production cost per unit.

ü This will enable the manufacturer to have a greater profit margin per unit at the prevailing price of the product. Hence, the producer will be tempted to supply more quantity to the market.

ü Weather also has a direct bearing on the supply of products. For example, demand for woollen products will increase during winter. This means the prices of woollen goods will be incresed in winter.

ü So, naturally, manufacturers will supply more volume of woollen goods during winter.

Factors influencing supply

The shape of the supply curve is affected by the following factors:

ü Cost of the inputs

ü Technology

ü Weather

ü Prices of related goods

ii.Law of demand states that other things being equal demand when price falls and contracts when price rises.

· Market demand is the total quantity demanded by all the purchasers together.

· Elasticity of Demand - Elasticity of demand may be defined as the degree of responsiveness of quantity demanded to a Change in price.

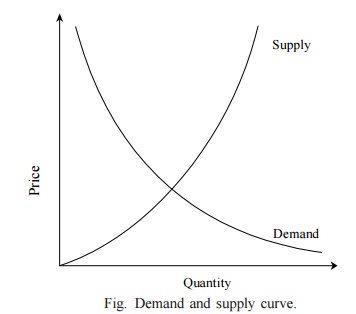

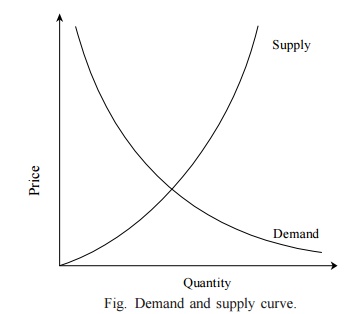

ü An interesting aspect of the economy is that the demand and supply of a product are interdependent and they are sensitive with respect to the price of that product. .

ü From Fig. it is clear that when there is a decrease in the price of a product, the demand for the product increases and its supply decreases.

ü Also, the product is more in demand and hence the demand of the product increases.

ü At the same time, lowering of the price of the product makes the producers restrain from releasing more quantities of the product in the market.

ü Hence, the supply of the product is decreased. The point of intersection of the supply curve and the demand curve is known as the equilibrium point.

ü At the price corresponding to this point, the quantity of supply is equal to the quantity of demand. Hence, this point is called the equilibrium point.

Fig. Demand and supply curve.

Factors influencing demand

The shape of the demand curve is influenced by the following factors:

ü Income of the people

ü Prices of related goods

ü Tastes of consumers

Related Topics