Chapter: 11th Accountancy : Chapter 9 : Rectification of Errors

Errors disclosed by the trial balance and errors not disclosed by the trial balance

Errors disclosed by the trial balance

and errors not disclosed by the trial balance

Generally, one-sided errors are revealed by trial balance. They will

cause disagreement of totals of debit balances and credit balances. Two-sided

errors are not revealed by trial balance. Thus, the errors can be classified on

the basis of their effect on the trial balance as follows:

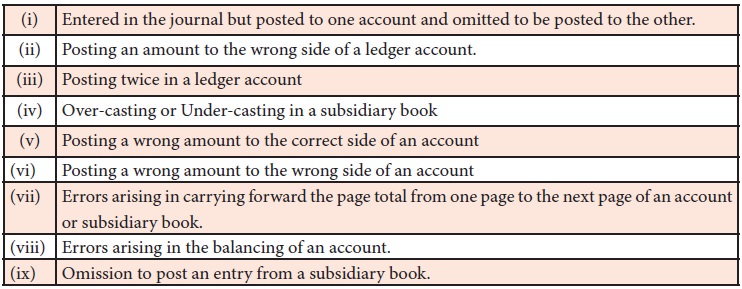

1. Errors disclosed by the trial balance

Certain errors affect the agreement of trial balance. If such errors

have occurred in the books of accounts, the total of debit and credit balances

will not be the same. The trial balance will not tally. Error of partial

omission and error of commission affect the agreement of trial balance.

Examples of such errors are follows:

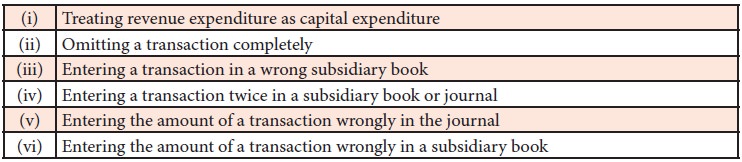

2. Errors not disclosed by the trial balance

Certain errors will not affect

the agreement of trial balance. Though such errors occur in the books of

accounts, the total of debit and credit balance will be the same. The trial

balance will tally. Errors of complete omission, error of principle,

compensating error, wrong entry in the subsidiary books are not disclosed by

the trial balance. Examples of such errors are as follows:

Related Topics