Chapter: 11th 12th std standard Indian Economy Economic status Higher secondary school College

Marginal Cost

Marginal Cost

Marginal cost is defined as the addition made to the total cost by the production of one additional unit of output.

Table Computation of marginal cost

Output (units) Total cost (Rs) Marginal Cost (Rs)

0 200 -

1 300 100

2 390 90

3 470 80

4 570 100

5 690 120

6 820 130

7 955 135

8 1100 145

For example, when a firm produces 100 units of output, the marginal cost would be equal to the total cost of producing 100 units minus the total cost of producing 99 units. Suppose the total cost of producing 99 units is Rs 9000 and the total cost of producing 100 units is Rs 10,000 then the marginal cost will be Rs10, 000 - Rs 9,000 = Rs 1,000. The firm has incurred a sum of Rs 1,000 in the production of one more unit of the commodity. Symbolically

MCn = TCn - TCn-1 where

MCn = Marginal cost

TC n = Total cost of producing n units

TC n-1 = Total cost of producing n-1 units

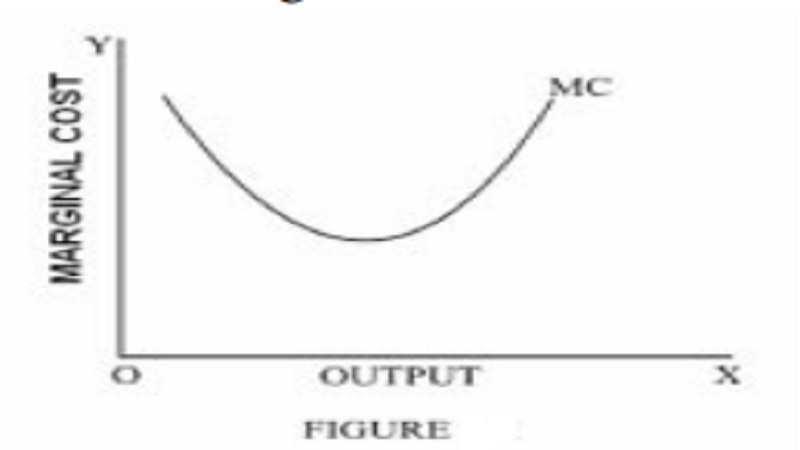

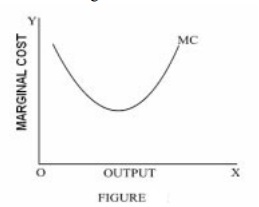

The marginal cost curve is given below

The marginal cost curve is 'U' shaped. The shape of the cost curve is determined by the law of variable proportions. If increasing returns (economies of scale)is in operation, the marginal cost curve will be declining, as the cost will be decreasing with the increase in output. When the diminishing returns (diseconomies of scale) are in operation, the MC curve will be increasing as it is the situation of increasing cost.

Relationship between short-run average and short-run marginal cost curves

The relationship between the marginal and the average cost is more a mathematical one rather than economic.

The relationship can be given as follows:

1. When marginal cost is less than average cost, average cost is falling

2. When marginal cost is greater than the average cost, average cost is rising

3. The marginal cost curve must cut the average cost curve at AC's minimum point from below. Thus at the minimum point of AC, MC is equal to AC.

Related Topics