Meaning, Features, Basic Concepts - Income Tax | 11th Commerce : Chapter 32 : Direct Taxes

Chapter: 11th Commerce : Chapter 32 : Direct Taxes

Income Tax

Income Tax

Income tax is a direct tax under which

tax is calculated on the income, gains or profits earned by a person such as

individuals and other artificial entities (a partnership firm, company, etc.)

Features of Income Tax in India

i. Levied as Per the Constitution

Income tax is levied in India by virtue of entry No. 82 of list I (Union List) of Seventh Schedule to the Article 246 of the Constitution of India.

ii. Levied by Central Government

Income tax is charged by the Central Government on all incomes other than agricultural income. However, the power to charge income tax on agricultural income has been vested with the State Government as per entry 46 of list II, i.e., State List.

iii. Direct Tax

Income tax is direct tax. It is because the liability to deposit and ultimate burden are on same person. The person earning income is liable to pay income tax out of his own pocket and cannot pass on the burden of tax to another person.

iv. Annual Tax

Income tax is an annual tax because it is the income of a particular year which is chargeable to tax.

v. Tax on Person

It is a tax on income earned by a person. The term ‘person’ has been defined under the Income tax Act. It includes individual, Hindu Undivided Family, Firm, Company, local authority, Association of person or body of Individual or any other artificial juridical persons. The persons who are covered under Income tax Act are called ‘assessees’.

vi. Tax on Income

It is a tax on income. The Income tax Act has defined the term income and it includes salary income, house property income, business/profession income, capital gains and other sources income. However, there are certain incomes which are specifically exempt from income tax.

vii. Income of ‘Previous Year’ is Assessable in ‘Assessment Year’

Income earned during a particular financial year is assessed to tax in the immediately following financial year. The year of earning income is called ‘Previous Year’ and the year in which assessment of income is done is called ‘Assessment Year’. The income tax return of previous year’s income is filed in the relevant assessment year.

viii. Charged at Prescribed Rate(s)

Income tax is charged at prescribed rate(s). The rates of income tax differ for different income and for different persons. While tax rates for normal incomes are prescribed by the annual Finance Act, tax rates for certain special incomes have been prescribed under Income Tax Act itself. For instance, the following tax rates have been prescribed under Income Tax Act.

a. Tax on long term capital gain @ 20% (Section 112).

b. Tax on short term capital gain on shares covered under STT @15% (Section 111A).

c. Tax on lottery income @ 30% (Section 115BB)

ix. Administered by the Central Government

Income tax is administered by the Central Government (Ministry of Finance) with the help of ‘Income tax department’ with branches throughout the country. The Central Government has constituted the ‘Central Board of Direct Taxes’ (CBDT) which exercises overall control over the Income tax department by issuing guidelines for related matters.

x. Applicability

Income Tax is applicable throughout India including the State of Jammu and Kashmir.

Basic Concepts of Income Tax

1. Assessee[(Sec. 2(7)]

Assessee means a person by whom any tax

or any other sum of money is payable under this Act. It includes every person

in respect of whom any proceeding has been taken for the assessment of his

income or assessment of fringe benefits.

2. Person[Sec.2 (31)]

The term ‘person’ includes the following

·

an individual,

·

a Hindu Undivided Family (HUF),

·

a company,

·

a firm,

·

an Association Of Persons or a Body Of

Individual, whether incorporated or not,

·

a local authority, and

·

every artificial juridical person e.g.,

an idol or deity.

3. Assessment Year (A.Y)[Sec.2 (9)]

The term has been defined under section

2(9). The year in which tax is paid is called the assessment year. It normally

consisting of a period of 12 months commencing on 1st April every year and

ending on 31st March of the following year.

4. Previous Year (P.Y)[Sec.(3)]

The year in which income is earned is

called previous year. It is also normally consisting of a period of 12 months

commencing on 1st April every year and ending on 31st March of the following

year. It is also called as financial year immediately following the assessment

year.

5. Income [Sec.2 (24)]

Income includes the followings;

·

Profits and gains of business or

profession.

·

Dividend

·

Voluntary contribution received by a

charitable / religious trust or university/ education institution or hospital/

electoral trust[ w.e.f.01.04.2010]

·

Value of perquisite or profit

in lieu of salary taxable u/s 17

and social allowance or benefit specifically granted either to meet personal

expenses or for performance of duties of an office or an employment of profit.

·

Export incentives, like duty drawback,

cash compensatory support, sale of licenses, etc.,

·

Interest, salary, bonus, commission or

remuneration earned by a partner of a firm from such firm.

·

Capital gain chargeable u/s 45.

·

Profits and gains from the business of

banking carried on by a co- operative society with its members.

·

Winning from lotteries, crossword

puzzles, races including horse races, card games and other games of any sort or

from gambling or betting of any form or nature whatsoever.

·

Deemed income u/s 41 or 59.

·

Sums received by an assessee from his employees towards welfare fund

contribution such as provident fund, superannuation fund, etc.

·

Amount received under key man insurance

policy including bonus thereon.

·

Amount received under agreement for-

·

not carrying out activity in relation to

any business, or (b) not sharing any know – how, patent, copyright etc.

·

Benefit or perquisite

received from a company, by a director or a person holding

substantial interest or a relative of the director or such person.

·

Gift as defined u/s 56 (2)(vi), and

others.

6. Agricultural Income (Section 2(1A)

Any rent or revenue derived from land

which is situated in India and is used for agriculture purposes. Agricultural

income is fully exempted from tax u/s 10(1) and as such does not form part of

total income.

Heads of Income [Sec. 14]

Section 14 of Income Tax Act 1961

provides for the computation of total income of an assessee which is divided

under five heads of income. Each head of income has its own method of

computation.

These five heads are;

1.

Income from ‘Salaries’ [Sections 15-

17];

2.

Income from ‘House Property’ [Sections

22-27];

3.

Income from ‘Profits and Gains of

Business or Profession’ [Sections 28- 44];

4.

Income from ‘Capital Gains’ [Sections

45-55]; and

5.

Income from ‘Other Sources’ [Sections

56-59].

Gross Total Income (GTI) [Section 80B (5)]

Income from all the above five heads of

income shall be computed separately according to the provisions given in the

Act. Income computed under these heads shall be aggregated after adjusting past

and present losses and the total so arrived at is known as ‘Gross Total

Income’.

1.

Income from ‘Salaries’ *****

2.

Income from ‘House Property’ *****

3.

Income from ‘Business or

Profession’ *****

4.

Income from ‘Capital Gains’ *****

5.

Income from ‘Other Sources’ *****

Gross Total Income (GTI) *****

Total Income (T.I.) [Sections 2 (45)]

Out of Gross Total Income, Income tax

Act 1961 allows certain deductions under section 80. After allowing

these deductions the figure which we arrive at is called ‘Total Income’ and on

this figure tax liability is computed at the prescribed rates.

Gross Total Income ****

Less: Deductions (Sec.80C to 80U) ****

Total Income (T.I.) ****

80C

Deductions; Contribution to Provident Fund, life

Insurance Premium, Children’s Tuition Fees, Health Insurance Premium,

Investment in National Savings Certificate, interest paid for home loans, etc.

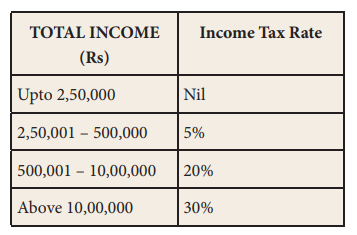

Income Tax Slab Rate for Individual - Illustration

As

per the Assessment Year 2018-19

Related Topics