Meaning, definition, Characteristics, Types, Conclusion - Factoring | 11th Commerce : Chapter 16 : Emerging Service Business in India

Chapter: 11th Commerce : Chapter 16 : Emerging Service Business in India

Factoring

FACTORING

Introduction

Firms sell goods on cash and credit

basis. When goods are sold on credit basis, bills are drawn on the buyer by the

seller. In case of small and medium business, a considerable part of their

working capital is tied down in bills

receivables. The liquidity position of the firm is affected and this hinders

the smooth functioning of the business. In order to overcome this hurdle,

Factoring as a service has emerged.

Meaning and Definition

Factoring is derived from a Latin term

“facere” which means ‘to make or do’. Factoring is an arrangement wherein the

trade debts of a company are sold to a financial institution at a discount. The

factor is an agent who buys the accounts receivables (Debtors and Bills

Receivables) of a firm and provides finance to a firm to meet its working

capital requirements.The main advantage of factoring is that the small or big

business firm receives short term finance (working capital) to meet day-to- day

payments.

In a report submitted to the Reserve

Bank of India, Mr.C.S.Kalyanasundaram defines factoring as “a continuing arrangement under which a

financing institution assumes the credit and collection functions for its

clients, purchases receivables as they arise (with or without recourse for

credit losses, i.e., the customer’s financial inability to pay), maintains the

sales ledgers, attends to other book-keeping duties relating to such accounts,

and performs other auxiliary duties”.

The Factoring Regulation Act 2011 governs the registration of factors and regulating the assignment of receivables and the associated obligations.

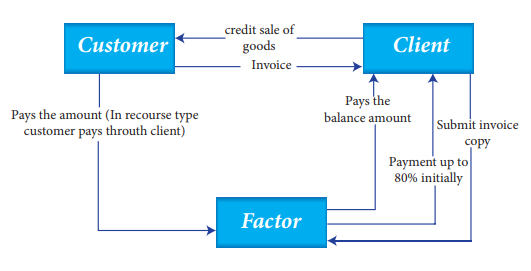

Factoring Process

a.

The firm enters into a factoring

arrangement with a factor, which is generally a financial institution, for

invoice purchasing

b.

Whenever goods are sold on credit basis,

an invoice is raised and a copy of the same is sent to the factor.

c.

The

debt amount due

to the firm

is transferred to the factor through assignment and the same is

intimated to the customer.

d.

On the due date, the amount is collected

by the factor from the customer.

e. After retaining the service fees, the remaining amount is sent to the firm by the factor

Maintenance of book-debts

a.

Maintenance of book-debts

A factor takes the responsibility of

maintaining the accounts of debtors of a business institution.

b.

Credit coverage

The factor accepts the risk burden of

loss of bad debts leaving the seller to concentrate on his core business.

c.

Cash advances

Around eighty percent of the total

amount of accounts receivables is paid as advance cash to the client.

d.

Collection service

Issuing reminders, receiving part

payments, collection of cheques form part of the factoring service.

e.

Advice to clients

From the past history of debtors, the factor is able to provide advices regarding the credit worthiness of customers, perception of customers about the products of the client, etc.

Types of factoring

a. Full service factoring or Without recourse factoring:

When a factor agrees to provide complete

set of services which includes financing, maintenance of sales ledger, debt

collection at his own risk, and providing consultancy services as and when

necessary, it is called as full servicing factoring.

b. With recourse factoring

When the factor does not undertake

credit risk, it is known as with recourse factoring. In case the debtor fails

to make the payment on due date, it is assigned back to the firm by the factor.

Here the responsibility of collecting the amount lies with the selling firm.

c. Maturity factoring

In this type, the factor agrees to

finance the firm only after collecting the amount on maturity from debtors.

d. International factoring

When the claims of an exporter are

assigned to a financial institution and the finance is advanced on the basis of

export invoice it is called as international factoring.

The factoring process involving the

client firm, factor and the customer is given below.

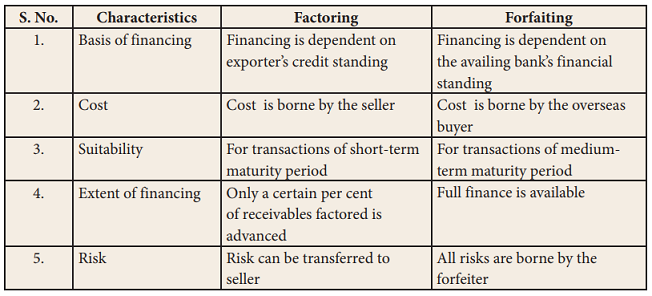

Factoring vs Forfaiting

Forfaiting is defined as “the

non-recourse purchase by a bank or any other financial institution of

receivables arising from an export of goods and services”.

Conclusion

Factoring helps smooth running of

business by getting short term credits from financial institutions against

accounts receivables. Forfaiting is a variation of factoring with focus on

international exports.

Related Topics