Chapter: Civil : Construction Planning And Scheduling : Cost Control, Monitoring and Accounting

Relating Cost and Schedule Information

Relating

Cost and Schedule Information

The previous sections focused upon the

identification of the budgetary and schedule status of projects. Actual

projects involve a complex inter-relationship between time and cost. As

projects proceed, delays influence costs and budgetary problems may in turn

require adjustments to activity schedules. Trade-offs between time and costs

were discussed in Section 10.9 in the context of project planning in which

additional resources applied to a project activity might result in a shorter

duration but higher costs. Unanticipated events might result in increases in

both time and cost to complete an activity. For example, excavation problems

may easily lead to much lower than anticipated productivity on activities

requiring digging.

While project managers implicitly recognize the

inter-play between time and cost on projects, it is rare to find effective

project control systems which include both elements. Usually, project costs and

schedules are recorded and reported by separate application programs. Project

managers must then perform the tedious task of relating the two sets of

information.

The difficulty of integrating schedule and cost information

stems primarily from the level of detail required for effective integration.

Usually, a single project activity will involve numerous cost account categories.

For example, an activity for the preparation of a foundation would involve

laborers, cement workers, concrete forms, concrete, reinforcement,

transportation of materials and other resources. Even a more disaggregated

activity definition such as erection of foundation forms would involve numerous

resources such as forms, nails, carpenters, laborers, and material

transportation. Again, different cost accounts would normally be used to record

these various resources. Similarly, numerous activities might involve expenses associated

with particular cost accounts. For example, a particular material such as

standard piping might be used in numerous different schedule activities. To

integrate cost and schedule information, the disaggregated charges for specific

activities and specific cost accounts must be the basis of analysis.

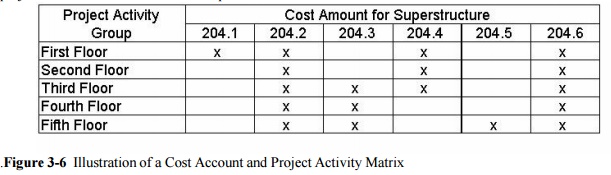

A straightforward means of relating time and cost

information is to define individual work elements representing the resources in

a particular cost category associated with a particular project activity. Work

elements would represent an element in a two-dimensional matrix of activities

and cost accounts as illustrated in Figure 3-6. A numbering or identifying

system for work elements would include both the relevant cost account and the

associated activity. In some cases, it might also be desirable to identify work

elements by the responsible organization or individual. In this case, a three

dimensional representation of work elements is required, with the third

dimension corresponding to responsible individuals. More generally, modern

computerized databases can accommodate a flexible structure of data

representation to support aggregation with respect to numerous different

perspectives; this type of system will be discussed in Chapter 5.

With this

organization of information, a number of management reports or views could be

generated. In particular, the costs associated with specific activities could

be obtained as the sum of the work elements appearing in any row in Figure 3-6.

These costs could be used to evaluate alternate technologies to accomplish

particular activities or to derive the expected project cash flow over time as

the schedule changes. From a management perspective, problems developing from

particular activities could be rapidly identified since costs would be

accumulated at such a disaggregated level. As a result, project control becomes

at once more precise and detailed

Unfortunately, the development and maintenance of

a work element database can represent a large data collection and organization

effort. As noted earlier, four hundred separate cost accounts and four hundred

activities would not be unusual for a construction project. The result would be

up to 400x400 = 160,000 separate work elements. Of course, not all activities

involve each cost account. However, even a density of two percent (so that each

activity would have eight cost accounts and each account would have eight

associated activities on the average) would involve nearly thirteen thousand

work elements. Initially preparing this database represents a considerable

burden, but it is also the case that project bookkeepers must record project

events within each of these various work elements. Implementations of the

"work element" project control systems have typically fondered on the

burden of data collection, storage and book-keeping.

Until data collection is better automated, the use

of work elements to control activities in large projects is likely to be

difficult to implement. However, certain segments of project activities can

profit tremendously from this type of organization. In particular, material

requirements can be tracked in this fashion. Materials involve only a subset of

all cost accounts and project activities, so the burden of data collection and

control is much smaller than for an entire system. Moreover, the benefits from

integration of schedule and cost information are particularly noticeable in

materials control since delivery schedules are directly affected and bulk order

discounts might be identified. Consequently, materials control systems can

reasonably encompass a "work element" accounting system.

In the absence

of a work element accounting system, costs associated with particular

activities are usually estimated by summing expenses in all cost accounts

directly related to an activity plus a proportion of expenses in cost accounts

used jointly by two or more activities. The basis of cost allocation would

typically be the level of effort or resource required by the different

activities. For example, costs associated with supervision might be allocated

to different concreting activities on the basis of the amount of work (measured

in cubic yards of concrete) in the different activities. With these

allocations, cost estimates for particular work activities can be obtained.

Related Topics