Chapter: Engineering Economics and Financial Accounting : Demand and Supply Analysis

Important Questions and Answers: Demand and Supply Analysis

DEMAND AND SUPPLY ANALYSIS

1.Define Demand.

Demand

indicates the quantities of products (goods service) which the firm is willing

and financially able to purchase at various prices, holding other factors

constant.

2. Define Determinants of Demand:

An

individual’s demand for a commodity depends on his desire and capability to

purchase it. Apart from the desire to purchase, there are many other factors

which influence the purchase of a product (demand). These are known as demand

determinants.

3. What is meant by Tastes and preferences of

Consumers:

The

change of tastes and preferences of consumers in favor of a commodity will

result in a greater demand for the commodity. The opposite also holds good i.e.

if the tastes and preferences of consumer change against the commodity, the

demand will suffer.

4. What are the two kinds of Consumers

expectations?

Consumers

have two kind of expectations one pertains to their future income and the

second is related to the future prices of the goods and its related goods.

5. Define Advertising

Advertisements

provide information about the presence of quality products in the market and

induces customer’s to buy more. It also promotes the latest preferences of the

general public to masses.

6. Define the Law of Demand:

The

relation of price to quantity demanded / sales is known as the law of demand.

Law of demand states that the higher the price is the lower the demand is and

vice versa, holding other factors as constant.

7. Define the price quantity relation.

This

price quantity relation can be expressed as demand being a function of price

D=f(p).

8. What Highlights of the law of demand:

1. The

relationship between price and quantity demanded is inverse.

2. Price is

the independent variable and demand the dependent variable.

3. Law of

demand assumes that except for price and demand, other factors remain constant.

9. What is Demand Shift: (Change in demand)

Factors shift the demand for a particular product

either on the right side of the demand curve or to the left side of the demand

curve based on the changes in price. These factors, other than the price of a

good that influence demand are known as demand shifters. The shift in the

demand either to the left or right is called the demand shift.

10.What are

the Exceptions to law of demand:

1. In share

markets on would have noticed that the rise in price of the shares increases,

the sales of the shares while decrease in the price of the shares results in

decrease of sale of the shares.

2. Some

goods which act as status symbol and have a snob appeal fall under this

category. Here when the price of the product rises then the appeal of the

product also rises and thus the demand. Some example are diamonds and antiques.

3. Finally,

ignorance on the part of the consumer may cause the consumer to buy at a higher

price, especially when the rise in price is taken to mean an improvement in

quality and a reduction in price as deterioration in quality.

11.Define Individual demand :

The quantity of a product demanded by an individual

purchaser at a given price is known as individual demand.

12.Define Market demand :

The total

quantity demanded by all the purchasers together is known as the market demand.

13.What are

the types of Demand function

1. Consumption

function

2. Product

consumption function

3. Differences

in regional incomes

4. Income

expectation and demand

14.What are

the Characteristics of demand function ?

1. The long

run relationship between consumption and income is some what stable, and

expenditure on consumption is usually about 85 to 90% of the income.

2. The

consumption function is highly unstable in short runs and the relationship

between income and consumption cannot be predicted by any mathematical formula.

3. During

the periods of economic prosperity, there is an absolute increase in the

expenditure on consumption, but decrease as a percentage of income during

periods of depression, the consumption declines absolutely but the expenditure

on the consumption increases as a percentage of income.

4. In the

periods of economic recovery, the rate of increase in consumption is higher

than the rate of the decline in consumption in times of recession.

15.Define

Product consumption function:

This function can be defined as the relationship

between the total income of the consumer and sales of particular products. It

means that when there is a change in income there is a change in the demand for

particular products.

16. Define Income expectations

and Demand:

Expectations are related to people’s estimates of

the level and durability of the future economic conditions. The demand for many

consumer durables (household appliances like TV, Washing machine, etc) is often

sensitive to general expectations regarding income level.

17.What are

the features of advertising demand relationship ?

1. Even when

there is no advertising effort done, there will be a certain amount of sales

possible for a particular product by virtue of its presence in the market.

2. There is

a direct relationship between advertising and sales. Thus when there is an

increased spending on advertisements. It will bring in more sales.

3. Increase

in advertisements will lead to more than proportionate increase in sales only

to a point. After that any increase in advertisement will have only less than

proportionate effect on sales.

18.Define

Elasticity of Demand:

Elasticity of demand is defined as ‘the percentage

change in quantity demanded caused by one percent change in the demand

determinant under consideration, while other determinants are held constant’.

19. Define demand determinant

It is the

degree of change in demand to the degree of change in any of the demand

determinants.

20.What are the Various

Elasticities ?

1. Price

elasticity of demand

2. Income

elasticity of demand

3. Cross

elasticity of demand

4. Promotional

elasticity

5. Exportations

elasticity of demand

21.Define

Price Elasticity of Demand

Price elasticity of demand can be defined as “the

degree of responsiveness of quantity demanded to a change in price”.

22.What are

the Types of price elasticity:

1. Perfectly

elastic demand

2. Absolutely

inclastic demand or perfectly inelastic demand

3. Unit

elasticity of demand

4. Relatively

elastic demand

5. Relatively

inelastic demand

23.Define Absolutely inelastic demand or perfectly

inelastic demand (ep=):

Absolutely

inelastic demand is where a change in price howsoever large, causes no change

in the quantity demanded of a product. Here, the shape of the demand curve is

vertical.

24.Define Relatively elastic demand (ep>1):

It is

where a reduction in price leads to more than proportionate change in demand.

Here the shape of the demand curve in flat.

25.What are theFactors determining price elasticity

of Demand ?

The

elasticity of demand depends on the following factors namely

1. Nature of

the product

2. Extent of

usage

3. Availability

of substitutes

4. Income

level of people

5. Proportion

of the income spent of the product

6. Urgency

of demand and

7. Durability

of a product.

Part B

1.

i. Define

law of demand &explain the types of demand.

According

to Marshall, The amount demanded increases with a fall in price and diminishes

with a rice in price, other remaining constant.

Types of Demand

ü Individual

& Market demand

ü Firm and

Industry product

ü Autonomous

& Derived demand

ü Demand

for durable and non durable demand

ü Short

term and long term demand

ü Joint

demand and composite demand

ü Direct

demand and Indirect demand

ü Total

market and Market segment demand

ü Negative

demand

ii.Why does demand curve sloping Downwards ?

Ø substitution effect

Ø income

effect

Ø new

consumer creating demand

Ø price

effect

Ø different

uses

2. Write a note on elasticity of supply & it’s

types

It is a

measure of degree of responsiveness of supply to the change in price

E(s) =

Proportional change in supply / Proportional change in price

Types of Elasticity of supply

1.Completely

(Perfectly) Inelastic supply: In this case the quantity

supplied does not react to the changes in the price. The increase or decrease

in the price does not change the quantity supplied.

2.Completely

(Perfectly) Elastic supply: When a minuscule change in

price results in infinite change in the quantity supplied then it is a case

of completely elastic supply. For instance when there is marginal rise in the

price, then the quantity supplied rises infinitely.

Unitary

Elastic supply: When the proportionate change in quantity supplied

is equal to the proportionate change in the price of the

commodity then we call it as unitary or unit elasticity of supply.

4.Relatively

Inelastic supply: When the percentage change in quantity supplied

is less than the proportionate change in price than it is a case

of relatively inelastic supply.

3. .Briefly

explain about various factors determining the demand.

ü Price of

the commodity

ü Taste

& Preference

ü Advertisements

& Sales Propaganda

ü Growth of

Population

ü Tax rate

ü Pattern

of saving Income of the consumer

ü Price of

related goods

ü Consumer’s

Expectations

ü Weather

conditions

ü Availability

of credit

ü Circulation

of money

4.

Describe

concept of demand elasticity .

It

denotes a measure of the rate at which demand changes in response to the change

in prices

1. Price

Elasticity of demand

2. Income

Elasticity of demand

3. Cross

elasticity of demand

4. Promotional

elasticity of demand 1.Price Elasticity of demand

Perfectly

Elastic demand ( E=∞)Demand change but price does not change

Perfectly

Inelastic demand ( E=0)

If the

demand for a commodity does not change in spite of an increase or decrease in

its price

Unitary

Elastic demand ( E=1)

Change in

demand is exactly proportionate to the change in price

2.Income

Elasticity of Demand

It is defined as the percentage change in the

quantity demanded of a good divided by the percentage change in the income of

the consumer,

3.Cross

elasticity of demand

A change

in demand for one good in response to a change in the price of another good .

It is a

measure of the responsiveness of demand for a commodity to the change in outlay

on advertisements and other promotional efforts

5. Discuss in detail about the Measurement of

Price Elasticity of Demand

1. Percentage Method

It

measures the percentage change in the quantity of a commodity demanded

resulting from a given percentage change in its price

2. Point Method or Geometric Method

It

measures the elasticity of demand on different points of a demand curve. It is

a variant proportionate method.

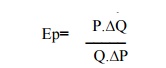

3. Arc Method

segment

of a demand curve between two points is called Arc.

Where

∆Q=

change in quantity demanded

∆P=

Change in price of the commodity

P1=

Original price

P2=New

Price

Q1=Original

quantity

Q2=New

quantity

4. Total outlay Method

It is

measured on the basis of change in total outlay or total expenditure in

response to change in the price of the commodity

Types:

Unitary Elasticity: Small

changes in price unaffected the total outlay

Elastic demand: Small changes in price increases

the total outlay

Inelastic demand: Small

changes in price decreases the total outlay

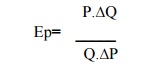

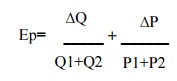

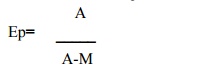

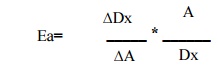

5. Revenue Method

It refers

to the sale proceeds of a firm

Where,

Ep=Stands for elasticity of demand

A=Stands for average revenue

M=Stands for Marginal

revenue

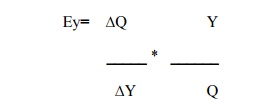

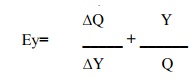

2.Income Elasticity of Demand

It is

defined as the percentage change in the quantity demanded of a good divided by

the percentage change in the income of the consumer,

Where,

Ey=

stands for income elasticity

Q=stands

for quantity demanded

Y=stands

for income

∆Q= Gives change in quantity demanded

∆Y = Gives change in income

Types of Income Elasticity of

demand

1.High Income elasticity : If Income

increases in high and quantity demand also good increases

2. Unitary Income elasticity: Changes

in income and quantity demanded are same

3. Low Income elasticity: If Income

increases in low and quantity demand also good increases

4. 4.Zero Income elasticity: No change

in quantity demanded by the changes in income

5. 5.Negative Income elasticity: Increase

in income results in decreases in quantity demanded

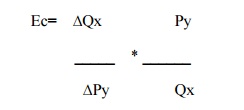

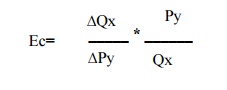

3. Cross elasticity of demand

A change

in demand for one good in response to a change in the price of another good .

Where,

Ec=stands

for cross elaticity

∆Qx=

changes in quantity demanded

Py=original

price of good y

∆Py=small changes in price of y

Qx=changes in

quantity demanded

Applications of cross elasticity

in management

a. In Production

b. Demand forecasting and pricing

c. In international trade and balance of payments

4. Advertising and promotional elasticity of demand

It is a

measure of the responsiveness of demand for a commodity to the change in outlay

on advertisements and

other

promotional efforts

Factors determining advertising

elasticity of demand

ü Type of

commodity

ü Market

share

ü Rival’s

reactions

ü State of

economy

ü Effect of advertising in terms of time

6.Tools of Forecasting Techniques

1. Qualitative model

a. Delphi

Technique

A

systematic forecasting method that involves structured interaction among a

group of experts on a subject.

The

Delphi Technique typically includes at least two rounds of experts answering

questions and giving justification for their answers, providing the opportunity

between rounds for changes and revisions.

b. Nominal group technique

The

nominal group technique (NGT) is a group process involving problem

identification, solution generation, and decision making.

c. Marketing research method

The

process or set of processes that links the consumers, customers, and end users

to the marketer through information — information used to identify and define

marketing opportunities and problems and improve understanding of marketing as

a process.

d. Sales force composite method

A

technique used by production managers to project the future demand for a good

or service based on the total amount that each salesperson anticipates being

able to sell in their region.

2. Quanitative model

I.Time Series Models

a. Last period Method

Uses last

period’s actual value as a forecast

Ft= At –

1

Ft =

Forecast demand for period t

At-1=

Actual demand in previous period

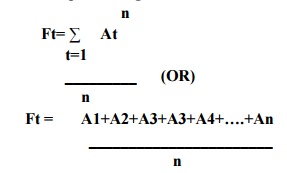

b. Simple Average Method

Ft

=Forecasted demand for period t

At=

Actual demand for period t

n= Total

no of periods

c. Moving average method

Uses an

average of a specified number of the most recent observations, with each observation

receiving a different emphasis (weight)

Where

Ft- Forecasted demand for period t

At- Actual demand for period t

n- Total no of periods

d. Exponential smoothing method

A

weighted average procedure with weights declining exponentially as data become

older.

Ft = Ft-1 + a(At-1 –

Ft-1)

Where

Ft – Forecasted demand for period t

Ft-1 –forecasted demand for previous method a- Smoothening constant

At-1- Actual demand for previous demand

e. Trend Project( Past data/ Predicting the future)

This

method is a version of the linear regression technique.

Y = a +

bX

Where

X

represents the values on the horizontal axis (time)

Y

represents the values on the vertical axis (demand).

2. Cause and Effect Model

a. Correlation and Regression method

Linear regression is a

mathematical technique that relates one variable, called an independent variable, to

another, the dependent variable,

Y = a +

bX

Y-

independent variable X- Dependent variable a- the intercept

B- slope

of the line

b. Econometric Method

It

includes endogenous –determined within the model ( controlled variables) and

exogenous variable-determined outside the model(uncontrolled variables)

eg.,

Money

C. Input and output method

It helps

to determine Or forecast the demand of a particular product or services.

d. End use method

It has

theoretical and practical method or value. It is influenced by the

technological , structural and other changes.

Related Topics