Chapter: Business Science : Financial Management : Working Capital Management

Inventory Management

Inventory Management

Introduction

Inventories

constitute the most significant part of current assets of the business concern.

It is also essential for smooth running of the business activities.

A proper

planning of purchasing of raw material, handling, storing and recording is to

be considered as a part of inventory management. Inventory management means,

management of raw materials and related items. Inventory management considers

what to purchase, how to purchase, how

much to purchase, from where to

purchase, where to store and when to use

for production etc.

Meaning

The dictionary meaning of the inventory is stock

of goods or a list

of goods. In accounting language, inventor y means stock

of finished goods. In a manufacturing point of view, inventory includes, raw material,

work in process, stores, etc.

1 Kinds of Inventories

Inventories

can be classified into five major

categories.

Raw

Material

It is basic and important

part of inventories. These are goods

which have not yet been committed to production in a manufacturing business concern.

Work in Progress

These include those

materials which have been committed to production

process but have not yet

been completed.

Consumables

These are the materials which are

needed to smooth running of the

manufacturing process.

Finished Goods

These are the final output of the

production process of the business concern. It is ready for consumers.

Spares

It

is also a part of inventories, which

includes small spares

and parts.

2 Objectives of Inventory Management

The major objectives of the inventory manage me nt are as follows:

To efficient and smooth

production process.

To maintain optimum inventory to

maximize the profitability.

To meet the seasonal demand of the products.

To avoid price increase in

future.

To ensure the level and site of inventories

required.

To plan when

to purchase and where to purchase

To avoid both

over stock and under stock

of inventory.

3 Techniques of Inventory Management

Inventory management

consists of effective control and ad ministration of inventories. Inventory control refers to a system which ensures supply of required quantity and quality of inventories at the required

time and at the same time prevent unnecessary investment

in inventories. It needs the following

important techniques.

Inventory

management techniques may be classified

into various types:

A.

Techniques based on the order quantity of Inventories

Order

quantity of inventories can be deter mined with the help of the following

techniques :

Stock Level

Stock

level is the level of stock which is maintained by the business concern at all

times. Therefore, the business concern must maintain optimum level of stock to

smooth running of the business process. Different level of stock can be determined

based on the volume of the stock.

Minimum Level

The

business concern must maintain minimum level of stock at all times. If the

stocks are less than the minimum level, then the work will stop due to shortage

of material.

Re-order Level

Re-ordering

level is fixed between minimum level and maximum level. Re-order level is the

level when the business concern makes fresh order at this level.

Re-order

level= maximum consumption × maximum Re-order period.

Maximum Level

It is the

maximum limit of the quantity of inventories, the business concern must maintain.

If the quantity exceeds maximum level limit then it will be overstocking.

Maximum level = Re-order level + Re-order quantity – (Minimum consumption ×

Minimum delivery period)

Danger Level

It is the

level below the minimum level. It leads to stoppage of the production process.

Lead Time

Lead time

is the time normally taken in receiving delivery after placing orders with

suppliers. The time taken in processing the order and then executing it is kno

wn as lead time.

Safety Stock

Safety

stock implies extra inventories that can be drawn down when actual lead time

and/ or usage rates are greater than expected. Safety stocks are deter mined by

opportunity cost and carrying cost of inventories. If the business concerns

maintain low level of safety stock, it will lead to larger opportunity cost and

the larger quantity of safety stock involves higher carrying costs.

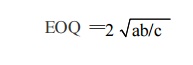

Economic Order Quantity (EOQ)

EOQ

refers to the level of inventory at which the total cost of inventory

comprising ordering cost and carrying cost. Determining an optimum level

involves two types of cost such as ordering cost and carrying cost. The EOQ is

that inventor y level that minimizes the total of ordering of carrying cost.

EOQ can

be calculated with the help of the mathematical formula:

Where,

a =

Annual usage of inventories (units)

b =

Buying cost per order

c =

Carrying cost per unit

4 Techniques Based On The Classification Of

Inventories

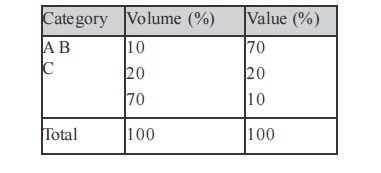

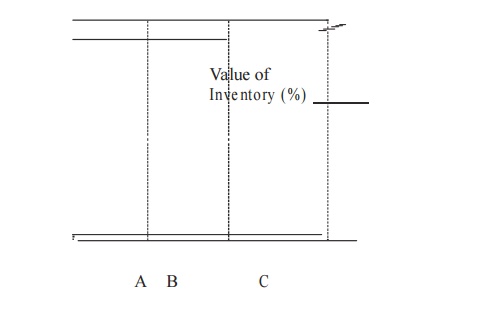

A-B-C analysis

It is the

inventory management techniques that divide inventory into three categories

based on the value and volume of the inventories; 10% of the inventory‘s item

contributs to 70% of value of consumption and this category is known as A

category. About 20% of the inventor y item contributes about 20% of value of

consumption and this category is called category B and 70% of inventor y item

contributes only 10% of value of consumption and this category is called C

category.

Inventory Breakdown Between Value and Volume

ABC analysis can be explained with the help of the following

Graphical presentation.

Inventories

Inventor

ies are classified according to the period of their holding and also this

method helps to identify the movement of the inventories. Hence, it is also

called as, FNSD analys is—

where,

F = Fast

moving inventories

N =

Normal moving inventories

S = Slow

moving inventories

D = Dead

moving inventories

VED Analysis

This

technique is ideally suited for spare parts in the inventory management like

ABC analysis. Inventories are classified into three categories on the basis of

usage of the inventories.

V = Vital item of inventories

E = Essential item of inventories

D = Desirable item of inventories

HML Analysis

Under this analysis, inventories are classified into three

categories on the basis of the value of the inventories.

H = High value of

inventories

M = Medium value of inventories

L = Low value of inventories

Techniques On The Basis Of Records

A. Inventory budget

It is a

kind of functional budget which facilitates the estimated inventory required

for the business

concern during a particular period. This budget is prepared based

on the

past experience.

B. Inventory reports

Preparation

of periodical inventory reports provides information regarding the order level,

quantity to be procured and all other information related to inventories. On the

basis of these reports, Management takes necessary decision regarding

inventory

control and Management in the business concern.

Valuation of Inventories

Inventories

are valued at different methods depending upon the situation and

nature of

manufacturing process. Some of the major methods of inventory

valuation

are mentioned as follows:

First in First Out Method (FIFO)

v Last in First Out

Method (LIFO)

v Highest in First Out Method (HIFO

v Nearest in First Out Method (NIFO)

v Average Price Method

v Base Stock Method

v Standard Price Method

v Market Price Method

Related Topics