Ratio Analysis | Accountancy - Classification of ratios | 12th Accountancy : Chapter 9 : Ratio Analysis

Chapter: 12th Accountancy : Chapter 9 : Ratio Analysis

Classification of ratios

Classification

of ratios

Ratios may be classified

in the following two ways:

i.

Traditional classification

ii.

Functional classification

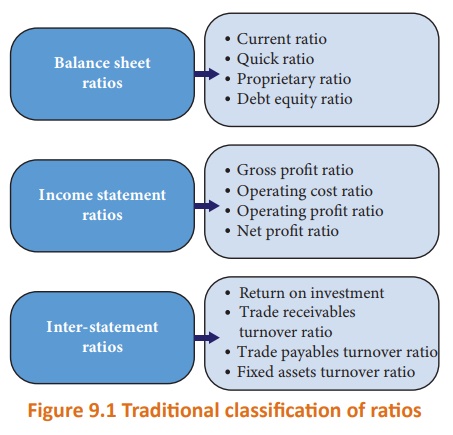

1. Traditional classification

Traditional

classification of ratios is done on the basis of the financial statements from

which the ratios are calculated. Under the traditional classification, the

ratios are classified as: (i) Balance sheet ratios, (ii) Income statement

ratios and (iii) Inter-statement ratios.

Figure 9.1 shows some of

the examples of ratios as per traditional classification:

(i) Balance sheet ratio

If both items in a ratio

are from balance sheet, it is classified as balance sheet ratio.

(ii) Income statement ratio

If the two items in a

ratio are from income statement, it is classified as income statement ratio.

(iii) Inter-statement ratio

If a ratio is computed

with one item from income statement and another item from balance sheet, it is

called inter-statement ratio.

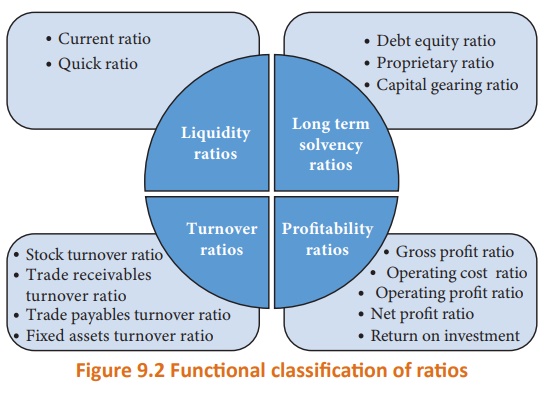

2. Functional classification

Functional

classification of ratios is based on the purpose for which ratios are computed

and it is the most commonly used classification. Under the functional

classification, the ratios are classified as follows:

(i) Liquidity ratios

(ii) Long term solvency

ratios

(iii) Turnover

ratios

(iv) Profitability

ratios

Figure 9.2 shows some of

the examples of ratios as per functional classification:

Related Topics