Chapter: Mechanical : Engineering Economics & Cost Analysis : Introduction to Economics

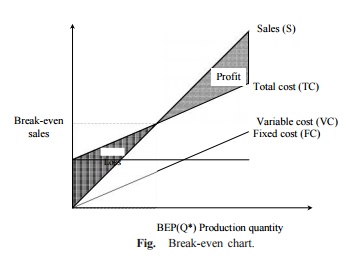

Break-Even Analysis

Break-Even Analysis

The main objective of break-even analysis is to find the cut-off production volume from where a firm will make profit.

Let

s = selling price per unit v = variable cost per unit FC = fixed cost per period Q = volume of production

The total sales revenue (S) of the firm is given by the following formula:

S = s Q

The total cost of the firm for a given production volume is given as

TC = Total variable cost + Fixed cost

= v Q + FC

· The linear plots of the above two equations are shown in Fig. .

· The intersection point of the total sales revenue line and the total cost line is called the break-even point.

· The corresponding volume of production on the X-axis is known as the break-even sales quantity.

· At the intersection point, the total cost is equal to the total revenue. This point is also called the no-loss or no-gain situation.

· For any production quantity which is less than the break-even quantity, the total cost is more than the total revenue.

· Hence, the firm will be making loss.

For any production quantity which is more than the break-even quantity, the total revenue will be more than the total cost. Hence, the firm will be making profit.

Profit = Sales – (Fixed cost + Variable costs)

= s Q – (FC + v Q)

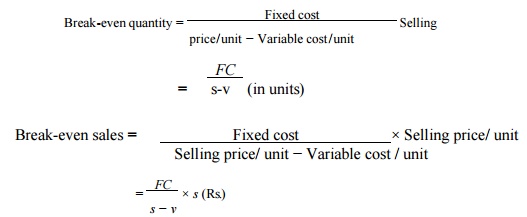

The formulae to find the break-even quantity and break-even sales quantity

Break-even quantity = [ Fixed cost ] / [ price/unit − Variable cost/unit ] Selling

= FC/ s-v (in units)

Break-even sales = [ Fixed cost × Selling price/ unit − Variable cost / unit ] x Selling price/ unit

= [ FC / s − v ] × s (Rs.)

The contribution is the difference between the sales and the variable costs. The margin of safety (M.S.) is the sales over and above the break-even sales. The formulae to compute these values are

Contribution = Sales – Variable costs

Contribution/unit = Selling price/unit – Variable cost/unit

M.S. = Actual sales – Break-even sales

= [ Profit / Contribution ] x sales

M.S. as a per cent of sales = (M.S./Sales) 100

P/V ratio is a valid ratio which is useful for further analysis.

The different formulae for the P/V ratio are as follows:

P/V ratio = Contribution / Sales = Sales − Variable costs / Sales

The relationship between BEP and P/V ratio is as follows:

BEP = Fixed cost / P/V ratio

Related Topics